Pesanan dari Pak Habib: Pak Habib mahu mengucapkan ribuan terima kasih kepada semua individu yang sudi infak Ramadan tempohari. Sumbangan anda telah diagihkan ke beberapa sekolah tahfiz dan anak yatim di Palestin, Thailand dan sekitar Kedah dan Perlis, katanya ribuan orang mendapat manafaat dari sumbangan anda dan mereka mendoakan anda... mudah-mudahan sumbangan anda itu memberi lebih berkat kepada energi rezeki anda.

baca di link ini:

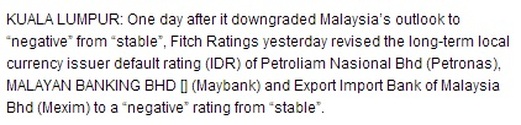

http://www.theedgemalaysia.com/business-news/248438-fitch-downgrades-petronas-maybank-and-mexims-idr-.html

Petronas, Maybank dan MEXIM kini dalam NEGATIF!!! Kita perlu hadapi Tsunami Ekonomi seperti yang dijangka 2014 adalah tahun masalah kewangan.

Mungkin anda rasa tak peduli sebab itu bukan kompeni bapak aku.. tapi apabila Petronas dan Maybank dalam negatif, bayangkan situasi macam ni.... pelabur mungkin keluarkan duit mereka dan masalah berlaku hingga ke stesen minyak petronas (tiada minyak - ini pun diesel asyik kurang je) dan Maybank bermasalah dan ianya boleh beranak sampailah ke semua industri.... bayangkan! Satu cara... naikkan harga minyak, kurangkan subsidi... walau macam mana pun ianya beri kesan jua kepada semua.... kita dah terperangkap.

Apakah anda masih terkulat-kulat malaslah nak berdoa dan berusaha kaya... alah duit zakat ada (tapi anda tak layak tau)... alah mak bapak aku kaya boleh bagi duit (tapi kami ni dah tak ada mak ayah)... alah duit 1Malaysia kan ada... alah aku ada 6 biji restoran hari-hari untung apa peduli... tak kisah apa alasan anda persoalannya apakah persediaan anda?

http://www.theedgemalaysia.com/business-news/248438-fitch-downgrades-petronas-maybank-and-mexims-idr-.html

Petronas, Maybank dan MEXIM kini dalam NEGATIF!!! Kita perlu hadapi Tsunami Ekonomi seperti yang dijangka 2014 adalah tahun masalah kewangan.

Mungkin anda rasa tak peduli sebab itu bukan kompeni bapak aku.. tapi apabila Petronas dan Maybank dalam negatif, bayangkan situasi macam ni.... pelabur mungkin keluarkan duit mereka dan masalah berlaku hingga ke stesen minyak petronas (tiada minyak - ini pun diesel asyik kurang je) dan Maybank bermasalah dan ianya boleh beranak sampailah ke semua industri.... bayangkan! Satu cara... naikkan harga minyak, kurangkan subsidi... walau macam mana pun ianya beri kesan jua kepada semua.... kita dah terperangkap.

Apakah anda masih terkulat-kulat malaslah nak berdoa dan berusaha kaya... alah duit zakat ada (tapi anda tak layak tau)... alah mak bapak aku kaya boleh bagi duit (tapi kami ni dah tak ada mak ayah)... alah duit 1Malaysia kan ada... alah aku ada 6 biji restoran hari-hari untung apa peduli... tak kisah apa alasan anda persoalannya apakah persediaan anda?

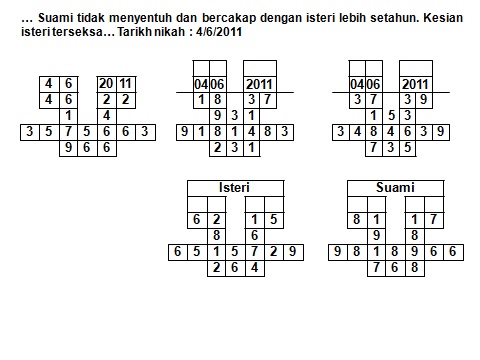

Apakah tarikh nikah anda mengandungi pola-pola konflik Bagaimana cara atasinya?

Tarikh nikah cikgu Ady dan isteri (seorang saja dari dulu hingga kini). masa tu umur 21 tahun mana ada kira tarikh ni.. Dari situ ada pola rumah masalah air bertakung hingga kini (rumah kami yang sebelum ini no 7 selalu banjir bila hujan walaupun barisan rumah teres tengah), banyak kali berpindah dan rumah sentiasa penuh dengan barang.. semenjak kami tidur di arah Selatan dalam bilik, rezeki adalah baik.

Tarikh nikah juga memberi klu tentang prestasi hidup anda... ada beberapa kes indvidu bermasalah perniagaan tetapi ok semula setelah buat teknik "terima nikah semula"... memang unik kes tersebut tetapi tarikh nikah memainkan peranan penting kerana ianya satu daripada tarikh penting kita.

Bagaimana memilih tarikh nikah yang baik? Apa kriteria tarikh baik dan tarikh tak baik? Bagaimana jika tarikh yang telah dipilih keluarga mengandungi pola konflik?

Tarikh nikah juga memberi klu tentang prestasi hidup anda... ada beberapa kes indvidu bermasalah perniagaan tetapi ok semula setelah buat teknik "terima nikah semula"... memang unik kes tersebut tetapi tarikh nikah memainkan peranan penting kerana ianya satu daripada tarikh penting kita.

Bagaimana memilih tarikh nikah yang baik? Apa kriteria tarikh baik dan tarikh tak baik? Bagaimana jika tarikh yang telah dipilih keluarga mengandungi pola konflik?

Karikatur karton di muka depan majalah The Economist dengan tajuk The Great Deceleration"... katanya pertumbuhan ekonomi dunia makin perlahan dan akan masuk fasa perubahan.

10 Reasons You’re Not Rich Yet

By Jocelyn Black Hodes | DailyWorth

Being “rich” can mean different things to different people, but I believe it means having the financial freedom to achieve your goals and live the life you want.

Regardless of our upbringing, education, profession or lifestyle, most of us are not where we want to be financially and our reasons are probably more similar than different. The good news is that it is never too late to become rich if you, like me, are ready to own up to the reasons you’re not and do something about it.

Want to know why you aren’t rich yet? Keep reading.

#1: You spend money like you’re already rich.

Sure, it feels good to buy expensive things, whether it’s a luxury car, designer clothes, a big house in the burbs, or a tropical vacation. Even if you don’t necessarily buy pricey items, if you consistently buy stuff you really don’t need, it still adds up fast ($300 trip to Target for toothpaste? AHEM). But the shopping high only lasts until the guilt and regret set in or the credit card bill arrives. Most of us are guilty of living beyond our means and using credit cards more than we should. The problem is that as long as we continue to spend more than we have, we can’t start building wealth. Chronic overspending and high-interest, revolving credit card debt are your worst enemies when it comes to financial success. Spend like you’re poor and you are much more likely to become rich.

#2: You don’t have a plan.

Without clearly defined short, mid and long-term goals, becoming rich will just seem like an unattainable fantasy. And that turns into your go-to excuse for why you shouldn’t bother saving or stop overspending. As we say in the financial industry: those who fail to plan, plan to fail. Creating a financial plan may seem overwhelming or intimidating, but it doesn’t have to be. Whether you do-it-yourself or decide to work with a financial professional, the process simply starts with prioritizing your goals and writing them down. Put that list where you can see it on a regular basis. Visual reminders go a long way in helping us stay on track.

#3: You don’t have an emergency fund.

I know, you’ve heard it a hundred times: you need to have at least six months of income saved in an emergency fund. And yes, it’s much easier said than done. However, I’ve seen too many people (including myself) get hit with a major unplanned expense, whether it’s a car or home repair or a medical bill, or an unexpected job loss, accident or illness that’s led to a drastic reduction in income. When these things happen--and they do, more often than you might think--not having a financial safety cushion can make the situation much, much worse. If you’re forced to rely on credit cards, you’ll end up sinking deeper into debt instead of, yes, saving to become rich.

#4: You started late.

With every year or month that goes by without saving, your chances of becoming rich decrease. Time and compounding interest are your two best friends when it comes to growing money, so wasting them really hurts. Just like exercising, the hardest part of saving is starting. Even if you’re in debt, making little money or have a lot of expenses, you can still always save something -- even if it is a small amount. The sooner you get yourself into the habit of saving -- regardless of how much -- the easier it will be for you to continue and eventually increase those savings. I like to think of saving as a muscle you have to work out and build with practice. Even if you start saving late, you can still become rich if you’re committed enough. But you need to start. Now.

#5: You’d rather complain than commit.

“Life is too expensive.” “I’ll never get out of debt.” “I don’t make enough money.” “Investing is too risky.” I’ve probably heard every excuse for why someone isn’t saving, investing or planning in general, and I’ll admit I’ve used a few of them myself from time to time. It’s easier to be lazy and let bad habits fester than to commit to --and follow through on -- changing them. It’s no wonder obesity and debt are epidemics in our country, and that millions of Americans have had to push off retirement. As long as the complaining, excuses and finger-pointing persist, so too will not becoming rich. Instead, take responsibility for your bad habits and focus on what you can do to change them. Then do it.

#6: You live for today in spite of tomorrow.

I get it. It is really hard to think about retirement and other distant fantasies when we have needs and plenty of wants now. The bills have to get paid, the family must be fed, momma needs a vacation -- and a new wardrobe to go along with it. The problem is that impulsive and overly-indulgent behavior commonly lead to credit card debt, spending money you might have otherwise saved and, yes, not becoming rich. Do yourself a favor: Ditch the “buy now, worry later” mindset and instead, adopt a “save now, get rich later” mindset.

#7: You’re a one-trick investor.

You might be lucky enough to become rich by betting all your money on one type of investment. Just like you might be lucky enough to win the lottery. But that’s not a strategy for getting rich (at least, not one I’d ever recommend).

One of the worst financial mistakes you can make is putting all your money eggs in one basket. Doing so puts you at too much risk, whether it is being too conservative or too aggressive. Sure, the stock market is on a run and real estate is on an upswing again, but are you prepared for when the tides turn? Because they will. And if you are invested in all fixed-income securities like CDs, bonds and annuities and think you’re safe, inflation should make you think again. Your investment portfolio needs to include a good mix of investments with varied levels of risk and return potential and liquidity (so you can get your money when you need it).

#8: You don’t automate.

Here’s the secret to saving: Automation. Saving is seamless when it’s automatic. Unfortunately, we are not born to be savers. We are impulsive and greedy by nature. Being responsible requires much more discipline. However, automation forces us to be responsible without too much effort. And all it requires is setting up regular transfers from a paycheck or bank account to a savings or investment account. Without it, we are much more likely to spend money we could be saving. Even if it is a seemingly small amount that you automate, those steady investments can make a big difference over time. Automate whatever you can whenever you can; just be careful to avoid overdrafting your account and try to increase your savings amount periodically.

#9: You have no sense of urgency.

You might think you don’t need to worry about getting out of debt or saving because someone, or something else will save you. Maybe it’s a pay raise, a new job, an inheritance, a rich spouse, or the lottery you’re counting on. Whatever “it” is, you use it as an excuse to put off taking steps on your own to become rich. The problem is that very little in life is certain. Who knows what will actually happen, or not happen, so why not focus on what you can control now? Save now and save yourself -- just in case something, or someone, else won’t.

#10: You’re easily influenced.

Maybe you live with a chronic overspender or a typical day out with your girlfriends involves shopping. Or maybe it’s your inner “Real Housewife” that you sometimes can’t control. We all have negative influences in our lives that threaten our chances of becoming rich. The superficial, materialistic, sensational culture in which we live is probably the biggest one. The suffocating swirl of media that goes along with it makes it ten times worse. The trick is not giving in to temptation. How? Some of it is making conscious choices to avoid putting yourself in vulnerable positions. But most of it is having the willpower to keep the goal of becoming rich in the front of your mind, especially when you are tempted to sabotage yourself.

By Jocelyn Black Hodes | DailyWorth

Being “rich” can mean different things to different people, but I believe it means having the financial freedom to achieve your goals and live the life you want.

Regardless of our upbringing, education, profession or lifestyle, most of us are not where we want to be financially and our reasons are probably more similar than different. The good news is that it is never too late to become rich if you, like me, are ready to own up to the reasons you’re not and do something about it.

Want to know why you aren’t rich yet? Keep reading.

#1: You spend money like you’re already rich.

Sure, it feels good to buy expensive things, whether it’s a luxury car, designer clothes, a big house in the burbs, or a tropical vacation. Even if you don’t necessarily buy pricey items, if you consistently buy stuff you really don’t need, it still adds up fast ($300 trip to Target for toothpaste? AHEM). But the shopping high only lasts until the guilt and regret set in or the credit card bill arrives. Most of us are guilty of living beyond our means and using credit cards more than we should. The problem is that as long as we continue to spend more than we have, we can’t start building wealth. Chronic overspending and high-interest, revolving credit card debt are your worst enemies when it comes to financial success. Spend like you’re poor and you are much more likely to become rich.

#2: You don’t have a plan.

Without clearly defined short, mid and long-term goals, becoming rich will just seem like an unattainable fantasy. And that turns into your go-to excuse for why you shouldn’t bother saving or stop overspending. As we say in the financial industry: those who fail to plan, plan to fail. Creating a financial plan may seem overwhelming or intimidating, but it doesn’t have to be. Whether you do-it-yourself or decide to work with a financial professional, the process simply starts with prioritizing your goals and writing them down. Put that list where you can see it on a regular basis. Visual reminders go a long way in helping us stay on track.

#3: You don’t have an emergency fund.

I know, you’ve heard it a hundred times: you need to have at least six months of income saved in an emergency fund. And yes, it’s much easier said than done. However, I’ve seen too many people (including myself) get hit with a major unplanned expense, whether it’s a car or home repair or a medical bill, or an unexpected job loss, accident or illness that’s led to a drastic reduction in income. When these things happen--and they do, more often than you might think--not having a financial safety cushion can make the situation much, much worse. If you’re forced to rely on credit cards, you’ll end up sinking deeper into debt instead of, yes, saving to become rich.

#4: You started late.

With every year or month that goes by without saving, your chances of becoming rich decrease. Time and compounding interest are your two best friends when it comes to growing money, so wasting them really hurts. Just like exercising, the hardest part of saving is starting. Even if you’re in debt, making little money or have a lot of expenses, you can still always save something -- even if it is a small amount. The sooner you get yourself into the habit of saving -- regardless of how much -- the easier it will be for you to continue and eventually increase those savings. I like to think of saving as a muscle you have to work out and build with practice. Even if you start saving late, you can still become rich if you’re committed enough. But you need to start. Now.

#5: You’d rather complain than commit.

“Life is too expensive.” “I’ll never get out of debt.” “I don’t make enough money.” “Investing is too risky.” I’ve probably heard every excuse for why someone isn’t saving, investing or planning in general, and I’ll admit I’ve used a few of them myself from time to time. It’s easier to be lazy and let bad habits fester than to commit to --and follow through on -- changing them. It’s no wonder obesity and debt are epidemics in our country, and that millions of Americans have had to push off retirement. As long as the complaining, excuses and finger-pointing persist, so too will not becoming rich. Instead, take responsibility for your bad habits and focus on what you can do to change them. Then do it.

#6: You live for today in spite of tomorrow.

I get it. It is really hard to think about retirement and other distant fantasies when we have needs and plenty of wants now. The bills have to get paid, the family must be fed, momma needs a vacation -- and a new wardrobe to go along with it. The problem is that impulsive and overly-indulgent behavior commonly lead to credit card debt, spending money you might have otherwise saved and, yes, not becoming rich. Do yourself a favor: Ditch the “buy now, worry later” mindset and instead, adopt a “save now, get rich later” mindset.

#7: You’re a one-trick investor.

You might be lucky enough to become rich by betting all your money on one type of investment. Just like you might be lucky enough to win the lottery. But that’s not a strategy for getting rich (at least, not one I’d ever recommend).

One of the worst financial mistakes you can make is putting all your money eggs in one basket. Doing so puts you at too much risk, whether it is being too conservative or too aggressive. Sure, the stock market is on a run and real estate is on an upswing again, but are you prepared for when the tides turn? Because they will. And if you are invested in all fixed-income securities like CDs, bonds and annuities and think you’re safe, inflation should make you think again. Your investment portfolio needs to include a good mix of investments with varied levels of risk and return potential and liquidity (so you can get your money when you need it).

#8: You don’t automate.

Here’s the secret to saving: Automation. Saving is seamless when it’s automatic. Unfortunately, we are not born to be savers. We are impulsive and greedy by nature. Being responsible requires much more discipline. However, automation forces us to be responsible without too much effort. And all it requires is setting up regular transfers from a paycheck or bank account to a savings or investment account. Without it, we are much more likely to spend money we could be saving. Even if it is a seemingly small amount that you automate, those steady investments can make a big difference over time. Automate whatever you can whenever you can; just be careful to avoid overdrafting your account and try to increase your savings amount periodically.

#9: You have no sense of urgency.

You might think you don’t need to worry about getting out of debt or saving because someone, or something else will save you. Maybe it’s a pay raise, a new job, an inheritance, a rich spouse, or the lottery you’re counting on. Whatever “it” is, you use it as an excuse to put off taking steps on your own to become rich. The problem is that very little in life is certain. Who knows what will actually happen, or not happen, so why not focus on what you can control now? Save now and save yourself -- just in case something, or someone, else won’t.

#10: You’re easily influenced.

Maybe you live with a chronic overspender or a typical day out with your girlfriends involves shopping. Or maybe it’s your inner “Real Housewife” that you sometimes can’t control. We all have negative influences in our lives that threaten our chances of becoming rich. The superficial, materialistic, sensational culture in which we live is probably the biggest one. The suffocating swirl of media that goes along with it makes it ten times worse. The trick is not giving in to temptation. How? Some of it is making conscious choices to avoid putting yourself in vulnerable positions. But most of it is having the willpower to keep the goal of becoming rich in the front of your mind, especially when you are tempted to sabotage yourself.

Concern over debt, spending

PETALING JAYA: Fitch Ratings, after cutting Malaysia’s credit rating outlook to “negative”, sending the stock market and the ringgit reeling, has said it is more likely to downgrade the country’s rating within the next two years on doubts over the Government’s ability to rein in its debt and spending.

Standard & Poor’s had last week, however, reaffirmed its credit rating on Malaysia and said it might raise sovereign credit ratings if stronger growth and the Government’s effort to reduce spending resulted in lower-than-expected deficits.

“With lower deficits, a significant reduction in Government debt is possible,” it said. It might lower its rating for Malaysia if the Government fails to deliver reform measures to reduce its fiscal deficits and increase the country’s growth prospects.

“These reforms may include implementing the Goods and Services Tax or GST, reducing subsidies, boosting private investments and diversifying the economy,” said S&P.

The downgrade in Malaysia’s rating outlook by Fitch on Tuesday took a toll on the capital markets, and sent the ringgit to a three-year low against the US dollar.

CIMB Research, in a note by its head of research Terence Wong and economics research head Lee Heng Guie, said Fitch’s revised outlook on the country was “bad news” for the stock market.

“While we believe there will be a knee-jerk selldown, the average lifespan for a rating outlook is about 18 to 24 months before a downgrade is enforced, giving Malaysia time to prevent that,” the report said.

They said the Fitch downgrade was a warning to Malaysia to improve its macroeconomic management, and was of the opinion that the Government had time to get its house in order.

Meanwhile, Areca Capital chief executive officer Danny Wong told StarBiz that foreign investors might use the downgrade as a reason to exit from Bursa Malaysia.

------------------------------------------

Memang sukar jadi Menteri Kewangan Malaysia... pada masa yang sama perjuangkan kebajikan rakyat tapi pada masa yang sama rating agency paksa negara kurangkan subsidi, laksanakan cukai barangan GST dsbnya... jika tidak. rating kewangan negara jadi lebih negatif dan pelabur asing keluar dari Bursa dan negara... Bila kerajaan nak laksanakan semua tu tentu saja rakyat protes tapi macam mana nak lindungi kepentingan pelabur asing pula... kalau begitu, buat tak tahu je demi rakyat tapi pelabur asing mungkin keluar sebab rating dah negatif ni dan akan terus negatif... tu yang tahun 2014 jadi tahun masalah kewangan...

katakanlah kerajaan terpaksa juga laksanakan tuntutan itu, maka apakah anda telah bersedia? Selama ni kita hidup dengan subsidi minyak dan gula dsbnya, tiada cukai barang (kecuali makan di restoran makanan segera kena cukai dsbnya tapi pergilah makan kedai biasa)... jadi kita ini agak mewah berbanding rakyat negara lain yang kena cukai barang tiap kali beli barang dan tiada subsidi... sebab itulah kita perlu tingkatkan keupayaan kewangan kita... mencipta strategi kekayaan dan membina kewangan yang kukuh jadi bilamana masalah kewangan tahun 2014 berlaku, kita telah bersedia...

Sayangnya negara kita masih berbalah pasal undi, pasal kantin sekolah, pasal itu ini... terlupa yang potensi masalah kewangan negara dah pun bermula dengan rating negatif sebegini... kita dah terlewat, sememangnya terlewat untuk hadapi tahun 2014 ni... mereka yang berbalah tu tak pelah dah kaya... anda yang sekarang dah ada masalah kewangan nak pergi minta tolong dengan YB yang mana? Melainkan kita sendiri betulkan dan tingkatkan energi kekayaan kita...

Kursus berkaitan:

- Strategi Hadapi Tahun 2014

- Pola 6 Potensi Kewangan dan Kekayaan.

PETALING JAYA: Fitch Ratings, after cutting Malaysia’s credit rating outlook to “negative”, sending the stock market and the ringgit reeling, has said it is more likely to downgrade the country’s rating within the next two years on doubts over the Government’s ability to rein in its debt and spending.

Standard & Poor’s had last week, however, reaffirmed its credit rating on Malaysia and said it might raise sovereign credit ratings if stronger growth and the Government’s effort to reduce spending resulted in lower-than-expected deficits.

“With lower deficits, a significant reduction in Government debt is possible,” it said. It might lower its rating for Malaysia if the Government fails to deliver reform measures to reduce its fiscal deficits and increase the country’s growth prospects.

“These reforms may include implementing the Goods and Services Tax or GST, reducing subsidies, boosting private investments and diversifying the economy,” said S&P.

The downgrade in Malaysia’s rating outlook by Fitch on Tuesday took a toll on the capital markets, and sent the ringgit to a three-year low against the US dollar.

CIMB Research, in a note by its head of research Terence Wong and economics research head Lee Heng Guie, said Fitch’s revised outlook on the country was “bad news” for the stock market.

“While we believe there will be a knee-jerk selldown, the average lifespan for a rating outlook is about 18 to 24 months before a downgrade is enforced, giving Malaysia time to prevent that,” the report said.

They said the Fitch downgrade was a warning to Malaysia to improve its macroeconomic management, and was of the opinion that the Government had time to get its house in order.

Meanwhile, Areca Capital chief executive officer Danny Wong told StarBiz that foreign investors might use the downgrade as a reason to exit from Bursa Malaysia.

------------------------------------------

Memang sukar jadi Menteri Kewangan Malaysia... pada masa yang sama perjuangkan kebajikan rakyat tapi pada masa yang sama rating agency paksa negara kurangkan subsidi, laksanakan cukai barangan GST dsbnya... jika tidak. rating kewangan negara jadi lebih negatif dan pelabur asing keluar dari Bursa dan negara... Bila kerajaan nak laksanakan semua tu tentu saja rakyat protes tapi macam mana nak lindungi kepentingan pelabur asing pula... kalau begitu, buat tak tahu je demi rakyat tapi pelabur asing mungkin keluar sebab rating dah negatif ni dan akan terus negatif... tu yang tahun 2014 jadi tahun masalah kewangan...

katakanlah kerajaan terpaksa juga laksanakan tuntutan itu, maka apakah anda telah bersedia? Selama ni kita hidup dengan subsidi minyak dan gula dsbnya, tiada cukai barang (kecuali makan di restoran makanan segera kena cukai dsbnya tapi pergilah makan kedai biasa)... jadi kita ini agak mewah berbanding rakyat negara lain yang kena cukai barang tiap kali beli barang dan tiada subsidi... sebab itulah kita perlu tingkatkan keupayaan kewangan kita... mencipta strategi kekayaan dan membina kewangan yang kukuh jadi bilamana masalah kewangan tahun 2014 berlaku, kita telah bersedia...

Sayangnya negara kita masih berbalah pasal undi, pasal kantin sekolah, pasal itu ini... terlupa yang potensi masalah kewangan negara dah pun bermula dengan rating negatif sebegini... kita dah terlewat, sememangnya terlewat untuk hadapi tahun 2014 ni... mereka yang berbalah tu tak pelah dah kaya... anda yang sekarang dah ada masalah kewangan nak pergi minta tolong dengan YB yang mana? Melainkan kita sendiri betulkan dan tingkatkan energi kekayaan kita...

Kursus berkaitan:

- Strategi Hadapi Tahun 2014

- Pola 6 Potensi Kewangan dan Kekayaan.

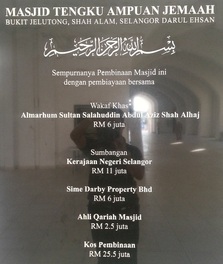

Dengan kekayaan dapatlah kita buat sesuatu kebajikan di dunia ini untuk bekalan akhirat... ada pasangan selebriti yang menyumbang jutaan ringgit untuk bina masjid di Kedah.. bilamana kita ada kekayaan, dapatlah kita buat sumbangan... seperti kos pembinaan masjid di Bukit Jelutong, Shah Alam ini.

Ini salah satu kaedah "Buffer" kewangan yang diamalkan cikgu Ady... apabila berada di kedai untuk membeli sesuatu barang, pecahkan duit RM50... jika ada baki maka;

1) wang RM1 lama masuk ke tabung duit sekolah anak.

2) wang RM1 yang baru masuk ke tabung duit raya

3) duit syiling masuk ke tabung syiling

4) duit not kertas - jika siri cantik masuk album . Jika siri tak cantik diguna esoknya.

Bila dah setahun, maka album duit cantik dah penuh dan ditukar beli Sijil Premium dan duit syiling dah banyak bolehlah buat infak/ sedekah ke masjid manakala ada terkumpul duit raya... kan mudah menyimpan cara "buffer" sebegini! Dah tak payah susah nak guna duit yang ada sekarang untuk cari duit raya dan ada duit nak menderma... contohnya, jika di bulan Ramadan ini anda ada RM1,500... jika tidak buat buffer, maka anda terpaksa tukar RM500 untuk duit raya tinggal RM1,000 ... dengan buffer, anda sudah menyimpan duit raya lebih awal dan tidak perlu guna RM500 itu semata-mata untuk buat duit raya.

Amalkan juga untuk perniagaan anda pula.

1) wang RM1 lama masuk ke tabung duit sekolah anak.

2) wang RM1 yang baru masuk ke tabung duit raya

3) duit syiling masuk ke tabung syiling

4) duit not kertas - jika siri cantik masuk album . Jika siri tak cantik diguna esoknya.

Bila dah setahun, maka album duit cantik dah penuh dan ditukar beli Sijil Premium dan duit syiling dah banyak bolehlah buat infak/ sedekah ke masjid manakala ada terkumpul duit raya... kan mudah menyimpan cara "buffer" sebegini! Dah tak payah susah nak guna duit yang ada sekarang untuk cari duit raya dan ada duit nak menderma... contohnya, jika di bulan Ramadan ini anda ada RM1,500... jika tidak buat buffer, maka anda terpaksa tukar RM500 untuk duit raya tinggal RM1,000 ... dengan buffer, anda sudah menyimpan duit raya lebih awal dan tidak perlu guna RM500 itu semata-mata untuk buat duit raya.

Amalkan juga untuk perniagaan anda pula.

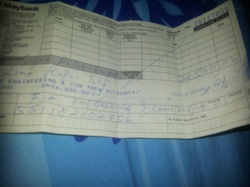

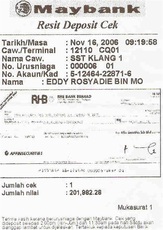

Slip deposit RM74K milik seorang peserta Elit38 dan sempat daftar syarikat pada 2 Julai lalu... tak sampai sebulan rezeki besar.. katanya ada lagi payment 16K dan 84K... Juga, beberapa sesi berdoa jarak jauh termasuk 20 julai lalu... semasa kursus Elit38 juga ada sesi berdoa bisnes berjaya kaya...

Energi tinggi hasilnya tinggi... berdoa adalah "booster" kepada hasil usaha dari ilmu dan strategi kita supaya lebih cepat berjaya.

Energi tinggi hasilnya tinggi... berdoa adalah "booster" kepada hasil usaha dari ilmu dan strategi kita supaya lebih cepat berjaya.

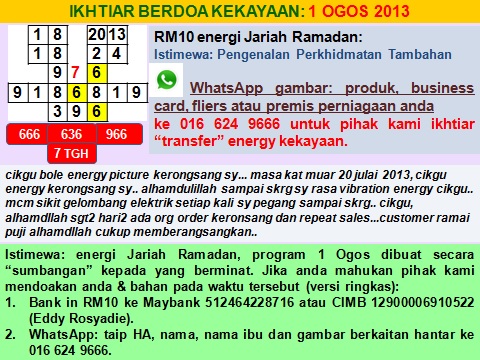

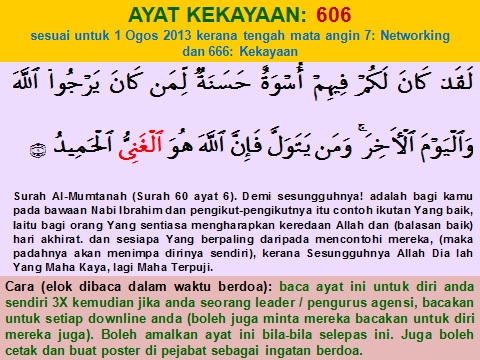

Esok 1 Ogos 2013, waktu berdoa kekayaan dberi percuma iaitu jam 9.30 malam - 11.30 malam maka anda buatlah berdoa sendiri ye... boleh juga panggil kawan-kawan atau ahli keluarga, elok sangat lah sebab khamis malam Jumaat lepas tarawih pulak tu... memang energi hebat... untuk non-muslim juga buatlah juga ikut cara anda sendiri... tapi jika anda mahu team kami doakan anda, bolehlah sumbangan jariah RM10 dan kalau nak lebih lagi boleh WhatsApp gambar produk atau kedai... juga ada sesi berdoa Premium Ekslusif RM138.... terpulang kepada anda.

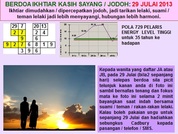

BERDOA KEKAYAAN 29 JULAI 2013:

Salam cikgu... 9.30 pg 29.7 sya wat solat dhuha.. then sy zikir slwat fatih tnpa hnti... pukul 10.30... partner sms bgtau dah ambl cek brnilai 82K++.. mlm tu wak2 trawih sya ngantuk sgt2... x prnh rsa ngntuk sblm ni... sya trtdo awal... mlm tu sya brmimpi mlht bntg yg byk d langit... sya dah terjaga dlm kol 1 pg lbh.... mlm tu ialh mlm 21... sya mngntuk yg amt sgt... mak kata mlm tu sunyi sepi... mcm lailatul qdr.

Salam cikgu... 9.30 pg 29.7 sya wat solat dhuha.. then sy zikir slwat fatih tnpa hnti... pukul 10.30... partner sms bgtau dah ambl cek brnilai 82K++.. mlm tu wak2 trawih sya ngantuk sgt2... x prnh rsa ngntuk sblm ni... sya trtdo awal... mlm tu sya brmimpi mlht bntg yg byk d langit... sya dah terjaga dlm kol 1 pg lbh.... mlm tu ialh mlm 21... sya mngntuk yg amt sgt... mak kata mlm tu sunyi sepi... mcm lailatul qdr.

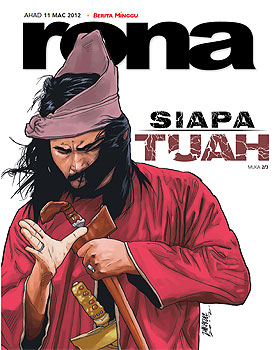

Nama Sebenar Hang Tuah adalah Daeng Merupawah atau Daeng Mempawah, iaitu anak kepada Raja yang pernah memerintah Daerah Bajung (ejaan sebenarnya adalah Daerah Bajeng, Gowa, Makassar). Hikayat Sulatus Al Salitin bertulisan jawi dengan ejaan ‘Ba Alif Jim Nga’ menyebabkan sebutannya menjadi Bajung.... Hang Tuah telah dilahirkan pada tahun 1388 Masehi.

Foto tahun 1994 bulan puasa di Syracuse University, New York USA.. Pelajar Malaysia situ berkumpul untuk ambil foto beramai-ramai.

Syracuse University rasanya satu-satunya universiti di USA ketika itu yang memberi cuti Hari Raya Aidilfitri, namun disebabkan tarikh telah kekal dalam kalendar universiti tetapi raya jatuh hari lain, maka terpaksa jugalah kami ke kelas pada hari raya...

Sempat dua kali raya di sana... kali pertama bujang je dan kali kedua dah ada isteri! Syok beraya dengan isteri di bawah salji tau! Kenangan kami 20 tahun berkahwin... Selamat Hari Raya Aidilfitri Sayang!

Syracuse University rasanya satu-satunya universiti di USA ketika itu yang memberi cuti Hari Raya Aidilfitri, namun disebabkan tarikh telah kekal dalam kalendar universiti tetapi raya jatuh hari lain, maka terpaksa jugalah kami ke kelas pada hari raya...

Sempat dua kali raya di sana... kali pertama bujang je dan kali kedua dah ada isteri! Syok beraya dengan isteri di bawah salji tau! Kenangan kami 20 tahun berkahwin... Selamat Hari Raya Aidilfitri Sayang!

Semasa di Syracuse, sempat bekerja sementara sebagai sukarelawan selama 3 bulan di Crouse-Irving Memorial Hospital... memang dah pola perubatan! Antara tugasan - bahagian logistik untuk transport pesakit dan menghantar bahan makmal.

Berdekatan Syracuse University ada satu Pusat Islam siap ada imam tetap untuk solat biasa dan Solat Jumaat dll serta beli ayam halal. Di dalam kampus SU, surau terletak di ruang bawah basement Hendrik Chapel, sebuah gereja yang terletak di tengah kampus... surau selalu berkunci kalau nak solat di surau kena ambil kunci surau dengan paderi yang jaga bangunan tu,

Among the individuals who have attended or graduated from Syracuse University include ... legendary venture capitalist and cofounder of Intel; Donna Shalala ... Joe Biden, Vice President of the United States; Robert Jarvik, inventor of the first artificial heart implanted into human beings; Eileen Collins, first female commander of a Space Shuttle; Prince Sultan bin Salman, first Arab, first Muslim and the youngest person to travel to space; Robert Menschel, legendary partner/director at Goldman Sachs; musician Lou Reed; and Prince Al-Waleed bin Talal, a prominent investor and member of the Saudi royal family.

Program "transfer energy" secara online ini adalah satu-satunya dan pertama di dunia oleh kami... adalah satu ikhtiar sesuai dengan teknologi zaman kini. Beberapa ujikaji cikgu Ady sebelum ini mendapati ianya boleh diusahakan cara sebegini. Anda boleh menghantar gambar diri anda, produk, premis perniagaan, business card, fliers dsbnya untuk tujuan dienergikan.

Untuk gambar diri, sila ambil gambar penuh (berdiri atau duduk jangan baring atau posing2) atau sekurangnya separuh badan macam gambar pasport... elakkan dari gambar muka semata-mata. Ini disebabkan pihak kami "menyentuh" gambar tidak sesuai tenyeh pada gambar muka.. untuk yang wanita mohon gambar yang sopan lengkap berpakaian lah sebab kami tidak boleh sentuh aurat anda walaupun dalam gambar (kemungkinan kami akan sentuh bahagian bahu anda dalam gambar tersebut).Buat masa ini pihak berdoa adalah kaum lelaki, kami cuba cari pihak wanita bagi tujuan sentuhan lain kali.. jika anda tidak selesa dengan "sentuhan" lelaki kami, maka hantar gambar produk atau business card sahaja.

Untuk gambar diri, sila ambil gambar penuh (berdiri atau duduk jangan baring atau posing2) atau sekurangnya separuh badan macam gambar pasport... elakkan dari gambar muka semata-mata. Ini disebabkan pihak kami "menyentuh" gambar tidak sesuai tenyeh pada gambar muka.. untuk yang wanita mohon gambar yang sopan lengkap berpakaian lah sebab kami tidak boleh sentuh aurat anda walaupun dalam gambar (kemungkinan kami akan sentuh bahagian bahu anda dalam gambar tersebut).Buat masa ini pihak berdoa adalah kaum lelaki, kami cuba cari pihak wanita bagi tujuan sentuhan lain kali.. jika anda tidak selesa dengan "sentuhan" lelaki kami, maka hantar gambar produk atau business card sahaja.

Seorang peserta kursus Pola 38 pada 1 Julai lalu mengerang kesakitan semasa sesi Upload Energy "SUN" sebelah petang (link dengan sdra Noredie di Kaabah pada waktu yang sama). Seolah nampak menyerang jantung tetapi apabila ditanya sebenarnya bukan di jantung tetapi badan keseluruhan tapi emosinya tertangkap di jantung. Energy SUN memang tinggi..

kursus Upload Energy Pola 38 yang akan datang, kami akan adjust cara Upload yang lebih sesuai.

kursus Upload Energy Pola 38 yang akan datang, kami akan adjust cara Upload yang lebih sesuai.

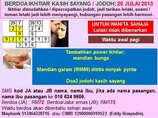

Program Berdoa Kasih Sayang 29 Jul 2013:

cikgu Ady, suami hantar sms petang semalam kata "sayang hingga hujung nyawa..." suami sudah boleh bercakap/ bercerita semalam, dah 3 bulan sy tak dengar dia bercerita sampaikan hasratnya yg sangat2 ingin bersama2 dengan anak2 dan sy... alhamdulillah cikgu.

cikgu Ady, suami hantar sms petang semalam kata "sayang hingga hujung nyawa..." suami sudah boleh bercakap/ bercerita semalam, dah 3 bulan sy tak dengar dia bercerita sampaikan hasratnya yg sangat2 ingin bersama2 dengan anak2 dan sy... alhamdulillah cikgu.

Alhamdulilah sessi pembelajaran taknik nombor bersama tuan... membuka minda mengapa masalah yg sama berulang dlm kehidupan saya,suami dan anak- anak.terima kasih cikgu

5 Reasons You're Earning More Money and You're Still Miserable

By Mandi Woodruff | Business Insider

Whether you're a millionaire or a middle-class father of two, we all make the same mistakes when it comes to money – we think the more we earn, the happier we'll be.

If you really want to buy yourself a more fulfilling life, it's not how much money you earn that matters, but figuring out the right way to spend it.

That's the idea explored in a fascinating new book, "Happy Money: The Science of Smarter Spending," written by a pair of renown behavioral scientists, Dr. Elizabeth Dunn and Dr. Michael Norton.

"When it comes to increasing the amount of money they have, most people recognize that relying on their own intuition is insufficient, spawning an entire industry of financial advisors," they write. "But when it comes to spending that money, people are often content to rely on their hunches about what will make them happy."

That all ends with this book. We've combed through and highlighted five ways to change the way you think about money that will make you happier in the long-run.

1. You're buying too many things and not enough experiences.

In a world where anything and everything can be yours with a credit card and access to the Internet, it's easy to get swept up by material things.

But if you recognized the fact that you could get more satisfaction out of a $50 dinner with friends than that big screen TV or new iPhone, it might change the way you shop.

"Research shows experiences provide more happiness than material goods in part because experiences are more likely to make us feel connected to others," Dunn and Norton write. "Understanding why experiences provide more happiness than material goods can also help us to choose the most satisfying kinds of experiences."

To help, here are four questions they suggest asking before you spend money on an experience that may not be as happiness-inducing as others:

1. Does this bring me together with other people?

2. Will this make a memorable story that I will tell for years to come?

3. Is this experience in line with who I am or who I'd like to become?

4. Is this a unique opportunity and something I can't compare to things I've done before?

2. You're more focused on getting more money than buying more time.

We get too caught up in either working hard to save a buck or working hard to earn a buck to realize what really matters – our time.

"Research suggests that people with more money do not spend their time in more enjoyable ways on a day-to-day basis," the authors write."Wealthier individuals tend to spend more of their time on activities associated with relatively high levels of tension and stress, such as shopping, working, and commuting."

On the flip side, penny-pinchers sometimes take saving too far. When you trade your time for some kind of monetary payoff (saving $20 on a flight by staying up all night on Kayak.com or using your vacation to earn over-time pay), you could be sacrificing your overall happiness in the process.

Now, if you get a high from saving five cents on a gallon of gas by driving 10 miles out of your way, then fine. But most people would be happier spending a little extra money to get home 20 minutes earlier for dinner.

3. You think a McMansion will make you happy.

What could possibly be more satisfying than ditching that old starter home you and your spouse moved into during your broke newlywed years?

Two studies cited in "Happy Money" prove otherwise.

When researchers followed groups of German homeowners five years after they moved into new homes, they all wound up saying they were happier with their newer house. But there was one problem: They weren't any happier with their lives. The same was true in a study of Ohio homeowners in which it turned out they weren't any happier with their lives than renters.

"Even in the heart of middle America, housing seems to play a surprisingly small role in the successful pursuit of happiness," Dunn and Norton write. "If the largest material purchase most of us will ever make provides no detectable benefit for our overall happiness, then it may be time to rethink our fundamental assumptions about how we use money."

4. You're letting yourself have too much of a good thing.

When you've got unlimited financial resources, it may seem stupid to deny yourself simple pleasures that you've come to enjoy, like new jewelry or an expensive bottle of wine with dinner every evening.

But when you reach that point of material over-saturation, you could be killing the potential to make yourself any happier.

"This is the sad reality of the human experience: The more we're exposed to something, the more its impact diminishes," Dunn and Norton write. "Knowing we have access to wonderful things undermines our happiness by reducing our tendency to appreciate life's small joys."

You think if the McRib were always on the menu, people would line up to get a taste every day? Probably not. Instead, try to make things you really enjoy a special treat you only allow yourself once in a while. It will pack a much happier punch.

5. You're investing too much in yourself and not enough in other people.

Like love, it stands to reason that the happier you are with yourself, the more likely it is that you'll bring happiness to others. But Dunn and Norton suggest flipping that idea on its head.

Make others happier first and you'll bring yourself happiness in the process. It sound obvious, but you'd be surprised how many of us forget it.

"In [a study] of more than 600 Americans, personal spending accounted for the lion's share of most people's budgets," they write. "But the amount of money individuals devoted to themselves was unrelated to their overall happiness. What did predict happiness? The amount of money they gave away. The more they invested in others, the happier they were."

That being said, you may wonder why you don't really feel all that much happier after donating a bag of clothing to Goodwill or cutting a check to the Red Cross. The real happiness comes from seeing your money at work.

By Mandi Woodruff | Business Insider

Whether you're a millionaire or a middle-class father of two, we all make the same mistakes when it comes to money – we think the more we earn, the happier we'll be.

If you really want to buy yourself a more fulfilling life, it's not how much money you earn that matters, but figuring out the right way to spend it.

That's the idea explored in a fascinating new book, "Happy Money: The Science of Smarter Spending," written by a pair of renown behavioral scientists, Dr. Elizabeth Dunn and Dr. Michael Norton.

"When it comes to increasing the amount of money they have, most people recognize that relying on their own intuition is insufficient, spawning an entire industry of financial advisors," they write. "But when it comes to spending that money, people are often content to rely on their hunches about what will make them happy."

That all ends with this book. We've combed through and highlighted five ways to change the way you think about money that will make you happier in the long-run.

1. You're buying too many things and not enough experiences.

In a world where anything and everything can be yours with a credit card and access to the Internet, it's easy to get swept up by material things.

But if you recognized the fact that you could get more satisfaction out of a $50 dinner with friends than that big screen TV or new iPhone, it might change the way you shop.

"Research shows experiences provide more happiness than material goods in part because experiences are more likely to make us feel connected to others," Dunn and Norton write. "Understanding why experiences provide more happiness than material goods can also help us to choose the most satisfying kinds of experiences."

To help, here are four questions they suggest asking before you spend money on an experience that may not be as happiness-inducing as others:

1. Does this bring me together with other people?

2. Will this make a memorable story that I will tell for years to come?

3. Is this experience in line with who I am or who I'd like to become?

4. Is this a unique opportunity and something I can't compare to things I've done before?

2. You're more focused on getting more money than buying more time.

We get too caught up in either working hard to save a buck or working hard to earn a buck to realize what really matters – our time.

"Research suggests that people with more money do not spend their time in more enjoyable ways on a day-to-day basis," the authors write."Wealthier individuals tend to spend more of their time on activities associated with relatively high levels of tension and stress, such as shopping, working, and commuting."

On the flip side, penny-pinchers sometimes take saving too far. When you trade your time for some kind of monetary payoff (saving $20 on a flight by staying up all night on Kayak.com or using your vacation to earn over-time pay), you could be sacrificing your overall happiness in the process.

Now, if you get a high from saving five cents on a gallon of gas by driving 10 miles out of your way, then fine. But most people would be happier spending a little extra money to get home 20 minutes earlier for dinner.

3. You think a McMansion will make you happy.

What could possibly be more satisfying than ditching that old starter home you and your spouse moved into during your broke newlywed years?

Two studies cited in "Happy Money" prove otherwise.

When researchers followed groups of German homeowners five years after they moved into new homes, they all wound up saying they were happier with their newer house. But there was one problem: They weren't any happier with their lives. The same was true in a study of Ohio homeowners in which it turned out they weren't any happier with their lives than renters.

"Even in the heart of middle America, housing seems to play a surprisingly small role in the successful pursuit of happiness," Dunn and Norton write. "If the largest material purchase most of us will ever make provides no detectable benefit for our overall happiness, then it may be time to rethink our fundamental assumptions about how we use money."

4. You're letting yourself have too much of a good thing.

When you've got unlimited financial resources, it may seem stupid to deny yourself simple pleasures that you've come to enjoy, like new jewelry or an expensive bottle of wine with dinner every evening.

But when you reach that point of material over-saturation, you could be killing the potential to make yourself any happier.

"This is the sad reality of the human experience: The more we're exposed to something, the more its impact diminishes," Dunn and Norton write. "Knowing we have access to wonderful things undermines our happiness by reducing our tendency to appreciate life's small joys."

You think if the McRib were always on the menu, people would line up to get a taste every day? Probably not. Instead, try to make things you really enjoy a special treat you only allow yourself once in a while. It will pack a much happier punch.

5. You're investing too much in yourself and not enough in other people.

Like love, it stands to reason that the happier you are with yourself, the more likely it is that you'll bring happiness to others. But Dunn and Norton suggest flipping that idea on its head.

Make others happier first and you'll bring yourself happiness in the process. It sound obvious, but you'd be surprised how many of us forget it.

"In [a study] of more than 600 Americans, personal spending accounted for the lion's share of most people's budgets," they write. "But the amount of money individuals devoted to themselves was unrelated to their overall happiness. What did predict happiness? The amount of money they gave away. The more they invested in others, the happier they were."

That being said, you may wonder why you don't really feel all that much happier after donating a bag of clothing to Goodwill or cutting a check to the Red Cross. The real happiness comes from seeing your money at work.

Study Finds Only 28 Percent of Millionaires Think They're Rich

If you had investments worth a million dollars, would you consider yourself rich? How about $5 million? Well, hold on to your wallet because a new study has found that the majority of millionaires don't consider themselves rich.

According to a study from investment bank UBS, entitled "What is Wealthy?," 40 percent of those with $5 million in investable assets said they didn't feel they were rich. And only 28 percent of investors who had between $1 and $5 million in investable assets viewed themselves as rich.

"To us, the surprise was that that many people with $1 million or more did not consider themselves wealthy," said Emily Pachuta, head of investor insights at UBS Wealth Management Americas. "We think it shows a very interesting mindset shift. People have certainly experienced a shock from the volatility of the market, and they are very aware that it takes a significant amount of money to have that dual feeling of having enough money and no financial constraints."

According to the opt-in, online survey of 4,450 Americans ages 25 plus with a minimum of at least $250,000 in investable assets (half with at least $1 million in investable assets), 50 percent of investors define wealth as "having no financial constraints on what they do." However, although the $5 million-plus investors are twice as likely to feel wealthy as investors with $1 million to $5 million in assets, only 64 percent of the former and 62 percent of the latter felt confident that they would achieve their goals.

"It's shocking to those of us who are not personally in that range, but it's not surprising when you take into the account the costs and expenses that are associated with people at that level of wealth," said Cliff Goldstein, a personal finance associate at Nerd Wallet, a cost comparison website.

Indeed, of those who have adult children, 80 percent said they are providing financial support for adult children, grandchildren or aging parents. "Unemployment, the economy and aging parents cause concern about the financial situation," he said.

For starters, research has shown that many rich people are afraid they will lose it all. Secondly, wealth is relative, especially in a world that is trying to keep up with the Jones's (whoever they are).

"In New York City, being wealthy enough to own upright a property worth $5 million doesn't make you feel rich, because you're surrounded by people who can buy and sell you in a two hours income," he told ABC News. "There are always some people around you who have more. Also, having $5 million in Keokuk, Iowa, is a lot different than having $5 million in New York or Silicon Valley or Seattle."

What's more, he says, most people don't understand money. "Handling assets and understanding what they are is a skill very few people have," he said. "To most people money is a stream and not a pool of assets."

One thing that does make investors feel confident is holding a significant amount of cash. According to UBS, despite significant market gains over the past year, investors keep an average of around 20 percent of their assets in cash, as they have for the past three years. Sixty-four percent feel they have the right amount of cash, and 56 percent expect to keep the same level of cash for the next 12 months.

Wealthy investors' two top personal finance concerns are long-term care and the finances of their children and grandchildren. While most feel highly prepared in their retirement planning (62 percent), 36 percent said they were not prepared at all.

"These people have a lot of money," said Goldstein. "But the reason they don't feel wealthy is because they don't feel like they have a comprehensive financial plan in place to take care of all of these longer-term costs."

If you had investments worth a million dollars, would you consider yourself rich? How about $5 million? Well, hold on to your wallet because a new study has found that the majority of millionaires don't consider themselves rich.

According to a study from investment bank UBS, entitled "What is Wealthy?," 40 percent of those with $5 million in investable assets said they didn't feel they were rich. And only 28 percent of investors who had between $1 and $5 million in investable assets viewed themselves as rich.

"To us, the surprise was that that many people with $1 million or more did not consider themselves wealthy," said Emily Pachuta, head of investor insights at UBS Wealth Management Americas. "We think it shows a very interesting mindset shift. People have certainly experienced a shock from the volatility of the market, and they are very aware that it takes a significant amount of money to have that dual feeling of having enough money and no financial constraints."

According to the opt-in, online survey of 4,450 Americans ages 25 plus with a minimum of at least $250,000 in investable assets (half with at least $1 million in investable assets), 50 percent of investors define wealth as "having no financial constraints on what they do." However, although the $5 million-plus investors are twice as likely to feel wealthy as investors with $1 million to $5 million in assets, only 64 percent of the former and 62 percent of the latter felt confident that they would achieve their goals.

"It's shocking to those of us who are not personally in that range, but it's not surprising when you take into the account the costs and expenses that are associated with people at that level of wealth," said Cliff Goldstein, a personal finance associate at Nerd Wallet, a cost comparison website.

Indeed, of those who have adult children, 80 percent said they are providing financial support for adult children, grandchildren or aging parents. "Unemployment, the economy and aging parents cause concern about the financial situation," he said.

For starters, research has shown that many rich people are afraid they will lose it all. Secondly, wealth is relative, especially in a world that is trying to keep up with the Jones's (whoever they are).

"In New York City, being wealthy enough to own upright a property worth $5 million doesn't make you feel rich, because you're surrounded by people who can buy and sell you in a two hours income," he told ABC News. "There are always some people around you who have more. Also, having $5 million in Keokuk, Iowa, is a lot different than having $5 million in New York or Silicon Valley or Seattle."

What's more, he says, most people don't understand money. "Handling assets and understanding what they are is a skill very few people have," he said. "To most people money is a stream and not a pool of assets."

One thing that does make investors feel confident is holding a significant amount of cash. According to UBS, despite significant market gains over the past year, investors keep an average of around 20 percent of their assets in cash, as they have for the past three years. Sixty-four percent feel they have the right amount of cash, and 56 percent expect to keep the same level of cash for the next 12 months.

Wealthy investors' two top personal finance concerns are long-term care and the finances of their children and grandchildren. While most feel highly prepared in their retirement planning (62 percent), 36 percent said they were not prepared at all.

"These people have a lot of money," said Goldstein. "But the reason they don't feel wealthy is because they don't feel like they have a comprehensive financial plan in place to take care of all of these longer-term costs."

Dapatkan majalah Fardu Ain Edisi 19

Menariknya edisi bernombor 19 bertema "Elak Cerai"... seperti yang cikgu Ady beritahu bahawa pola angka 11 dan 19 atau 91 berkaitan dengan "berjauhan" yang boleh menyebabkan perceraian... tak sangka pula kebetulan Edisi 19 ini cerita tentang perihal perceraian... memang betul-betul kebetulan!

Baca... sangat sesuai untuk ilmu tambahan untuk para isteri atau wanita bakal isteri juga suami dan lelaki bakal suami.

Kata seorang penulis (muka surat 29): apabila suami dapat menyimpan kuasa talak dan pada masa yang sama isteri dapat menggunakan kuasa menggoda tentu tidak akan berlaku perceraian...

Menariknya edisi bernombor 19 bertema "Elak Cerai"... seperti yang cikgu Ady beritahu bahawa pola angka 11 dan 19 atau 91 berkaitan dengan "berjauhan" yang boleh menyebabkan perceraian... tak sangka pula kebetulan Edisi 19 ini cerita tentang perihal perceraian... memang betul-betul kebetulan!

Baca... sangat sesuai untuk ilmu tambahan untuk para isteri atau wanita bakal isteri juga suami dan lelaki bakal suami.

Kata seorang penulis (muka surat 29): apabila suami dapat menyimpan kuasa talak dan pada masa yang sama isteri dapat menggunakan kuasa menggoda tentu tidak akan berlaku perceraian...

Memilih keserasian... memilih tarikh nikah (dan waktu nikah) yang sesuai.. .juga jika dah ternikah dan salah pula tarikh nikah nak buat macam mana ada caranya ikhtiar pembetulan...

Kursus/ bahan berkaitan:

- Potensi Jodoh dan Perkahwinan.

- Sesi konsultansi keluarga.

- Laporan Keserasian Pasangan.

Kursus/ bahan berkaitan:

- Potensi Jodoh dan Perkahwinan.

- Sesi konsultansi keluarga.

- Laporan Keserasian Pasangan.

PERHATIAN: Cikgu Ady amat-amat tidak bersetuju dengan perkataan yang selalu digunakan oleh orang ramai iaitu "kalau Tuhan dah tentukan itu bukan jodoh kita (bercerai)" atau "dah takdir nak buat macam mana (bercerai)".... Kaedah pernomboran versi cikgu Ady adalah untuk membuat pemilihan keserasian dan membuat peningkatan keserasian, jadi tidak timbul isu ayat-ayat tersebut jika kita (kedua-dua pihak suami dan isteri) sudah ada ilmu dan strategi SEBELUM mahupun SEMASA dalam tempoh perkahwinan.. cuba lihat contoh di atas jelas menunjukkan ada potensi masalah, jadi bagaimana cara menguruskannya dengan berkesan? Tidak perlukan ayat-ayat itu jika sudah tahu cara menguruskannya.

Assalam ckgu ady... td masa lps doa ksh syg sya tekan telunjuk jari di photo lps tu mcm ada cahaya kat blkg mula2 kecil pastu jd besar... alhamdulillah...

Td sy dftr SSM dpt no 0662299.. .sy dftr guna nama yg ckgu cadangkan.. balik dp SSM sy gi JPN utk tukar almt ic.. dpt no giliran di JPN tadi 0060...

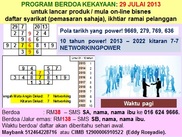

Program Berdoa Kekayaan (Networking Power)

29 Julai 2013

..dpt no pendaftaran: SA0267967... dan satu lagi SA0267965.. sendiri pun terkejut... alhamdulillah sbb Allah kabul hajat nak buat networking ni sungguh-sungguh dan berkat doa dari cikgu ady dan team juga.

Menakjubkan.. dapat nombor pendaftaran 769 pada hari networking power 29 Julai tu 769, 966, 366!

Program berdoa jarak jauh sebenarnya dah bermula pada 28 Julai lagi apabila cikgu Ady singgah di Masjid Jamek Muar selepas berbuka puasa di Muar untuk solat hajat dan berdoa untuk peserta berdaftar... kemudian pada 29 Jul jam 9.30 pagi dibuat di Masjid As-Syarif, Meru, Klang untuk peserta yang berdaftar dan pada masa yang sama Team Admin Johor bersama Delegasi SSM berada di SSM Johor. Sementara menunggu mereka siap daftar, cikgu Ady ke Bank Simpanan Nasional untuk beli Simpanan Premium (no giliran 1066 dan nombor sijil bermula dari 01006261169). Dalam jam 11.30 pagi, kami "on-line" video call untuk sesi berdoa jarak jauh. Jadi, cikgu Ady pilih berdoa di depan Maybank Setia Alam duduk dalam kereta (tentunya plet 7699) dan hari ni memang penuh orang parking depan Maybank. Semasa berdoa, sebuah kereta datang dan parking depan... plet 7779 dan selepas berdoa hujan pun turun... hujan rahmat... mudah-mudahan ikhtiar berdoa berhasil kejayaan,

29 Julai 2013

..dpt no pendaftaran: SA0267967... dan satu lagi SA0267965.. sendiri pun terkejut... alhamdulillah sbb Allah kabul hajat nak buat networking ni sungguh-sungguh dan berkat doa dari cikgu ady dan team juga.

Menakjubkan.. dapat nombor pendaftaran 769 pada hari networking power 29 Julai tu 769, 966, 366!

Program berdoa jarak jauh sebenarnya dah bermula pada 28 Julai lagi apabila cikgu Ady singgah di Masjid Jamek Muar selepas berbuka puasa di Muar untuk solat hajat dan berdoa untuk peserta berdaftar... kemudian pada 29 Jul jam 9.30 pagi dibuat di Masjid As-Syarif, Meru, Klang untuk peserta yang berdaftar dan pada masa yang sama Team Admin Johor bersama Delegasi SSM berada di SSM Johor. Sementara menunggu mereka siap daftar, cikgu Ady ke Bank Simpanan Nasional untuk beli Simpanan Premium (no giliran 1066 dan nombor sijil bermula dari 01006261169). Dalam jam 11.30 pagi, kami "on-line" video call untuk sesi berdoa jarak jauh. Jadi, cikgu Ady pilih berdoa di depan Maybank Setia Alam duduk dalam kereta (tentunya plet 7699) dan hari ni memang penuh orang parking depan Maybank. Semasa berdoa, sebuah kereta datang dan parking depan... plet 7779 dan selepas berdoa hujan pun turun... hujan rahmat... mudah-mudahan ikhtiar berdoa berhasil kejayaan,

cikgu bole energy picture kerongsang sy... masa kat muar 20 julai 2013, cikgu energy kerongsang sy.. alhamdulillah sampai skrg sy rasa vibration energy cikgu.. mcm sikit gelombang elektrik setiap kali sy pegang sampai skrg.. cikgu, alhamdllah sgt2 hari2 ada org order keronsang dan repeat sales...customer ramai puji alhamdllah cukup memberangsangkan..

(tempahan kerongsang: Alin Kuantan 012 929 9927)

(tempahan kerongsang: Alin Kuantan 012 929 9927)

Biar perut langsing asalkan dompet buncit!

Foto projek "Delegasi SSM" pada 2 Julai lalu... ada individu yang daftar 10 buah syarikat sekali! Projek SSM yang tak pernah dibuat orang tapi kami satu-satunya yang menawarkannya di sini ada pelbagai pakej Daftar SSM.

Sesi konsultansi yang dijalankan di Kulai, Johor di Hotel Novelle pada 28 Julai lalu untuk sebuah keluarga (10 orang). Senang cerita sekali harung bawa anak-anak sekali bertanya dan bertanya pelbagai perihal potensi bisnes, kerjaya dll. Kami siapkan sekali set binding semua graf dan laporan berkaitan.

Untuk tempahan pakej (Johor): En Nizam 012 769 3807

Untuk tempahan pakej (Johor): En Nizam 012 769 3807

Minyak Pyrite 83 (Edisi Khas) disimpan dalam sebuah kotak warna emas (dibeli di Mekah) dileta bersama 2 botol minyak pyrite yang telah didoakan dan disentuh lantai Kaabah pada 20 Mac lalu, juga dibelakangnya diletakkan kad emas yang mana emas itu juga didoakan di depan Kaabah, kesemua ini berada di atas meja pemain mp3 ayat Al-Quran... pemindahan frekuensi energy yang tinggi.. oleh itu simpan botol minyak di tempat yang bersih dan suci supaya frekuensinya dapat dikekalkan... untuk "recharge" ada beberapa cara.. satu cara mudah pasang mp3 ayat Al-Quran disebelahnya.

Tempahan minyak pyrite:

Edisi Biasa 38 - RM38 - hubungi Pak Lah 017 5049786

Edisi Khas 83 - RM83 - bank in RM83 (+ kos pos RM10 Semenanjung / RM20 Sabah Sarawak) dan SMS nama, nama ibu, alamat pos ke 016 624 9666.

Tempahan minyak pyrite:

Edisi Biasa 38 - RM38 - hubungi Pak Lah 017 5049786

Edisi Khas 83 - RM83 - bank in RM83 (+ kos pos RM10 Semenanjung / RM20 Sabah Sarawak) dan SMS nama, nama ibu, alamat pos ke 016 624 9666.

RSS Feed

RSS Feed