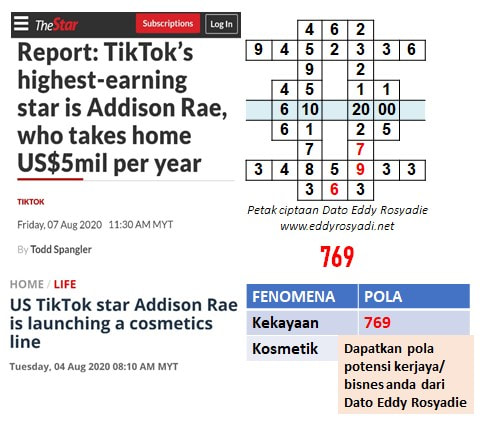

| Tahun 2021 ada pola 786 biasanya dikaitkan dengan "kepimpinan" seperti seorang Penyelia, Pengurus, Pengarah, CEO, Boss, dsbnya.

** ada bonus kepada mereka yang hadir KDT786 untuk hadir ke Seminar Hadapi 2021/2022 di Larkin, Johor Bahru pada 10 Oktober 2020. |  |

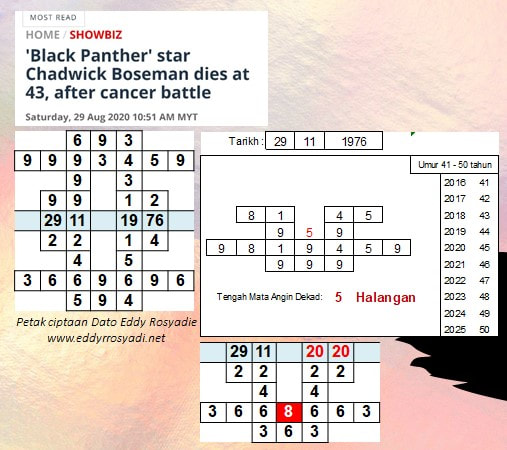

Beliau ini dikenali sebagai "King of Wakanda" dalam filem Black Panther. Beliau didapati hadapi kanser pada tahun 2016 kebetulan ketika usia dekad halangan bermula. Dan pada tahun 2020 tahun tekanan beliau meninggal dunia.

Bagaimana pula dengan usia dekad anda? Bilakah usia dekad tekanan? Bilakah usia dekad kekayaan?

Bagaimana pula dengan usia dekad anda? Bilakah usia dekad tekanan? Bilakah usia dekad kekayaan?

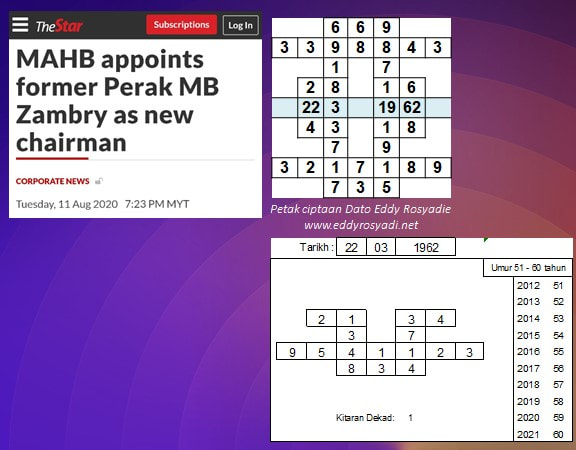

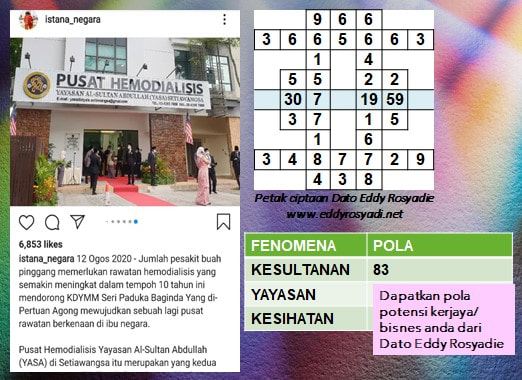

Beliau ini dilahirkan tanpa pola 38 atau 83 tentang kesultanan dalam petak tarikh lahir statik. Bagaimana pula beliau boleh berlakon utama sebagai "King of Wakanda"? (king = kesultanan = pola 38). Rupanya petak tarikh lahir dinamik pada tahun 2016 semasa filem Captain America: The Civil War, watak Black Panther beliau ini diperkenalkan iaitu anak kepada Raja Wakanda, beliau tahun 2016 itu ada pola 38 (kesultanan) dalam petak tarikh lahir dinamik. Juga kebetulan pada tahun 2016 juga, beliau adalah pelakon utama dalam filem "Message from the King" (king = kesultanan = pola 38).

Kebetulan? Fenomena 38 ini pun boleh terjadi dalam perfileman? Inilah dinamakan fenomena kehidupan. Malah pelakon Afdlin Aman Ramlie juga dilahirkan tanpa pola 38 atau 83 kesultanan dalam petak tarikh lahir statik tetapi pada tahun 2004, beliau berlakon sebagai Sultan Melaka dalam filem Puteri Gunung Ledang sebab pada tahun 2004 itu petak tarikh lahir dinamik beliau ada pola 38 kesultanan.

Kebetulan? Fenomena 38 ini pun boleh terjadi dalam perfileman? Inilah dinamakan fenomena kehidupan. Malah pelakon Afdlin Aman Ramlie juga dilahirkan tanpa pola 38 atau 83 kesultanan dalam petak tarikh lahir statik tetapi pada tahun 2004, beliau berlakon sebagai Sultan Melaka dalam filem Puteri Gunung Ledang sebab pada tahun 2004 itu petak tarikh lahir dinamik beliau ada pola 38 kesultanan.

| Musibah Covid19 ada hikmah dan ujiannya. Hikmahnya dapat kita kenali perangai pasangan yang sebenar apabila dalam situasi tertekan sebegini. Masa bercinta dan mula berkahwin bukan main manis lagi, tetapi bila diuji dengan tekanan kewangan sebegini, mau ditumbuk dipukul. Tapi sang isteri tak berdaya nak mengadu kepada pihak berkuasa. Kata kahwin kerana cinta tapi kenapa masalah kewangan menjadi punca pasangan jadi agresif? Apakah kahwin itu kerana duit? kerana wang? Itu sebenarnya yang menjadi isu dan risiko untuk berkahwin. Maka, betulkan energi rezeki di dalam perkahwinan anda.

Berkahwin dengan individu kaya tidak menjamin anda akan kekal kaya selama2nya. Ada banyak kes muflis /bankrup /masalah kewangan setelah berkahwin walaupun asalnya kaya raya. |  |

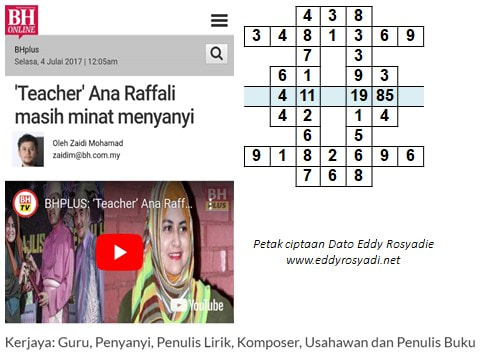

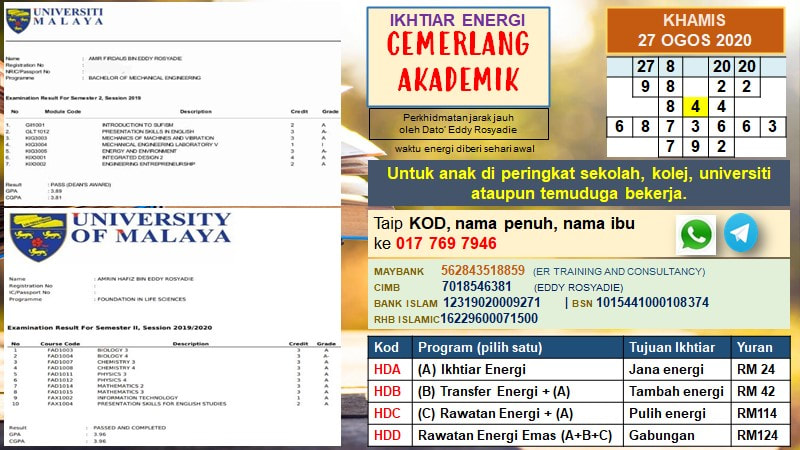

Sudah kena dengan pola2 dan elemen2 di dalam petak tarikh lahir. Begitulah kajian yang dijalankan oleh Dato Eddy Rosyadie menggunakan pernomboran tarikh lahir orang sebenar kisah sebenar yang digunakan sebagai panduan untuk orang lain yang tercari2 perniagaan/ kerjaya yang sesuai untuk mereka.

Kenali Potensi Diri dan Pantau Prestasi anda bersama Dato Eddy Rosyadie

017 769 7946

016 624 9666

Kenali Potensi Diri dan Pantau Prestasi anda bersama Dato Eddy Rosyadie

017 769 7946

016 624 9666

|  |

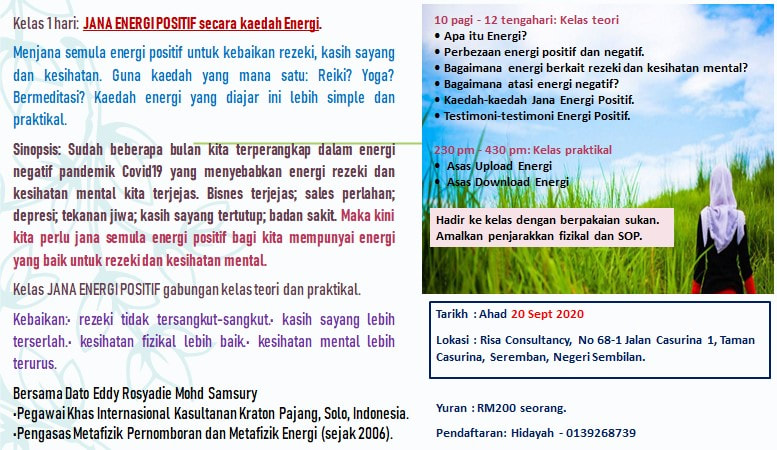

Bagaimana untuk menjana / menghasilkan energi yang positif yang dapat membawa kepada kebaikan2 kepada diri kita? Menjana energi bagi aura rezeki, aura kasih sayang, aura kesihatan mental dan fizikal yang baik. Jom, hadiri kelas JANA ENERGI POSITIF.

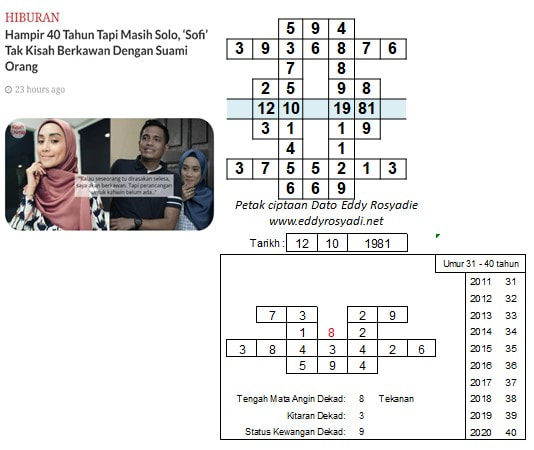

| Kisah seorang pendekar terkenal dengan kesaktiannya di Indonesia yang dikenali Jaka Tingkir mengasaskan Kasultanan Pajang, Solo setelah mengambilalih Kerajaan Demak. Kasultanan Pajang cuma 30 tahun selepas itu diganti dengan kerajaan Mataram yang pada mulanya dihadiahkan satu wilayah kepada kerajaan Mataram dan akhirnya mengambil alih kasultanan Pajang. Pada tahun 2010, Kasultanan Pajang dihidupkan kembali bertujuan untuk mengekalkan warisan dan sejarah budaya. Dato Eddy Rosyadie adalah Pegawai Khas Internasional Kasultanan Keraton Pajang. |  |

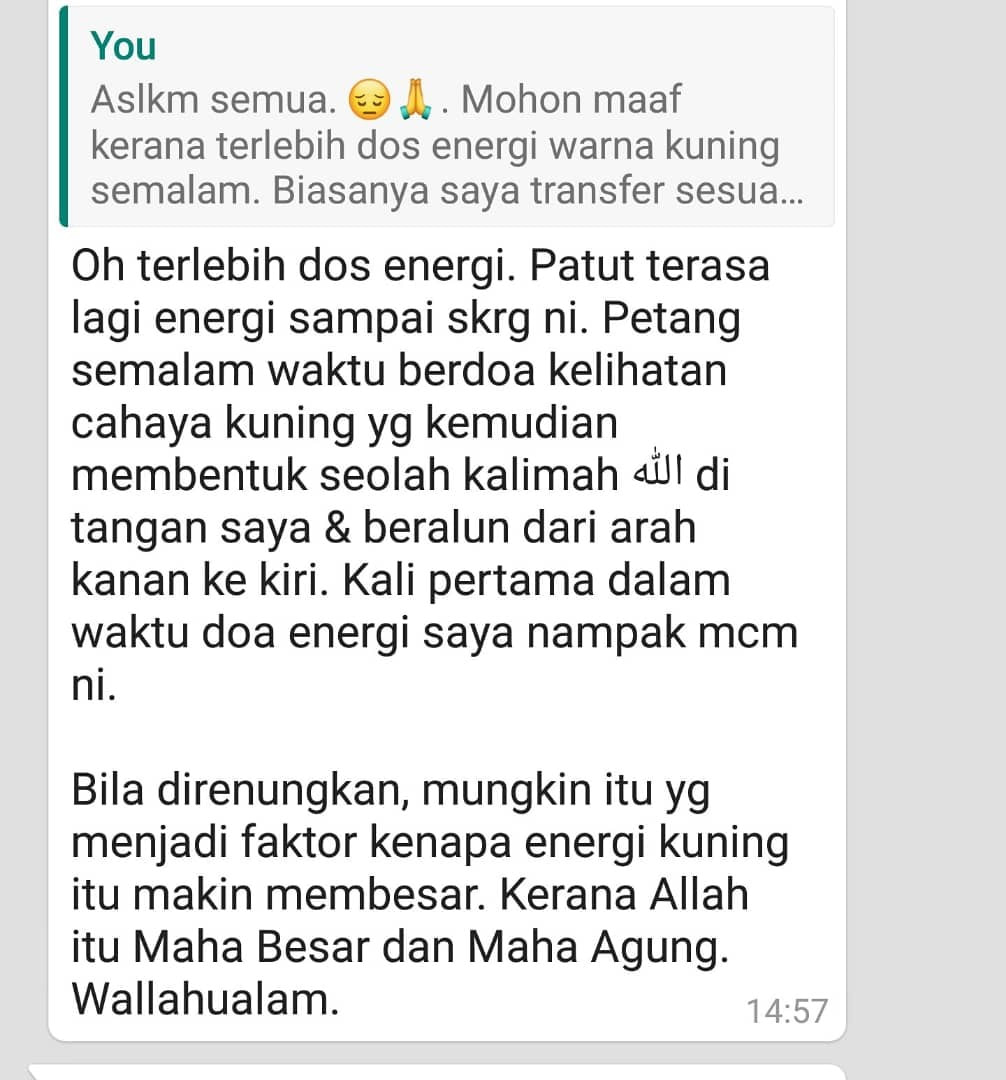

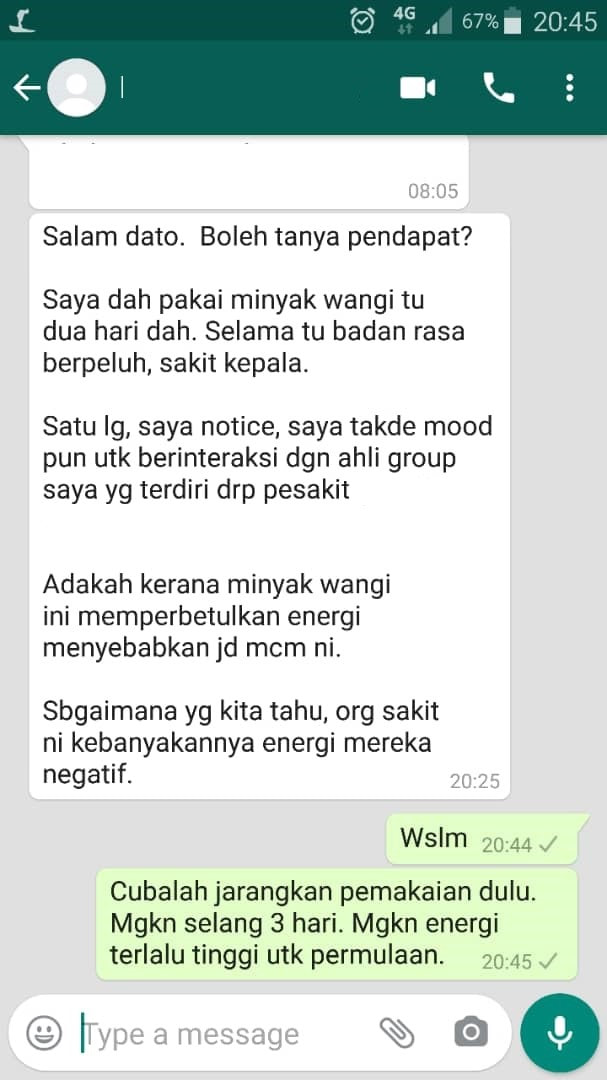

| Maklumbalas pengguna minyak wangi ENERGI PUTIH yang diadun oleh Dato Eddy Rosyadie. Maklumbalas sebegini selalu dikemukakan. Biasalah permulaan pemakaian mendatangkan kesan jadi dijarakkan selang 3 hari kemudian selang 2 hari dan akhirnya selang 1 hari bagi menjadikan energi itu serasi dengan badan. |  |

| Bagi yang bekerja makan gaji pasti akan bersara namun persoalannya tentang kecukupan simpanan. Majoriti kita memang punyai pendapatan MASUK tetapi kurang dapat menguruskan perbelanjaan KELUAR yang menyebabkan simpanan selalu berkurangan. Banyak seminar2 kewangan yang menyajikan kaedah2 untuk pendapatan MASUK yang banyak tetapi kurang memberi penekanan tentang perbelanjaan KELUAR. Terdapat strategi metafizik pernomboran dan juga ikthiar metafizik energi bagi membetulkan isu wang KELUAR dan isu membuat simpanan. |  |

|   |

| Ada individu yang TIDAK PERNAH JATUH CINTA. Psikologi mengaitkan fenomena ini sebagai "Victim of Counter Dependency". Ada strategi secara psikologi tentang perihal ini. Daripada persepektif metafizik pula, ada individu yang punyai masalah jodoh kerana; 1. Usia Dekad 20an- 50an tiada pola jodoh. 2. Setiap Graf Hayat ada potensi Married Star tetapi ada individu yang punyai Married Star BESERTA Widowed Star sekali. Ini menyebabkan mereka sentiasa ragu2 tentang perasaan cinta yang berputik. 3. Dan pelbagai faktor lagi termasuk TERSALAH ARAH. |

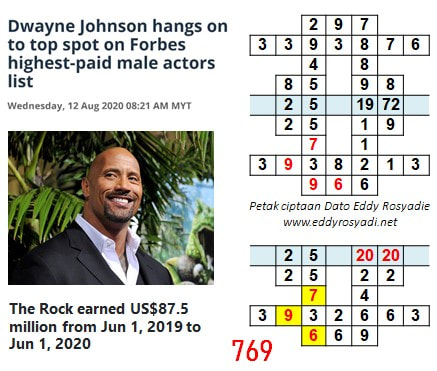

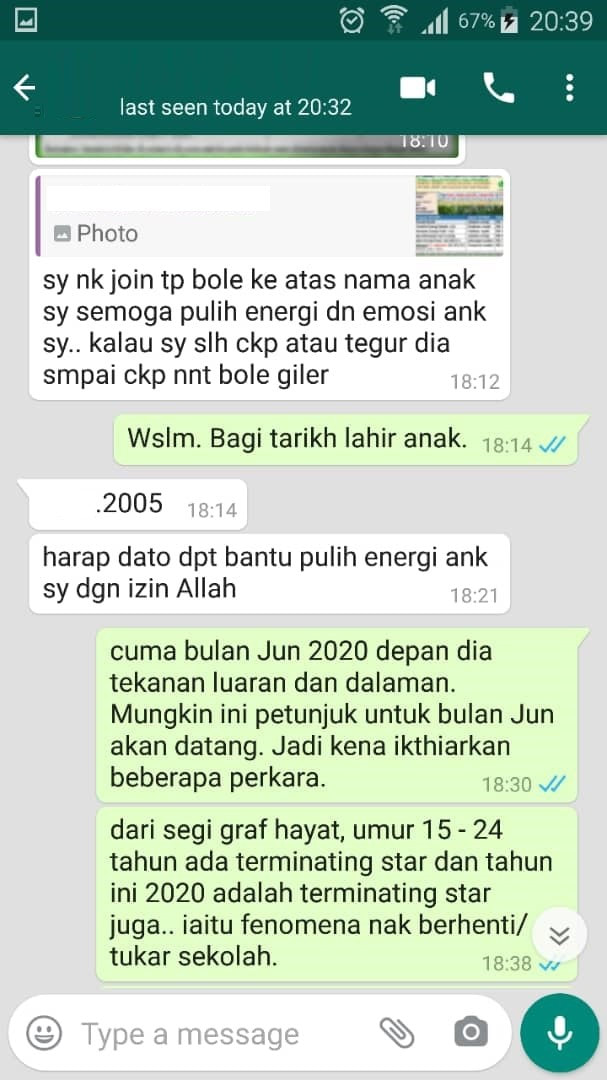

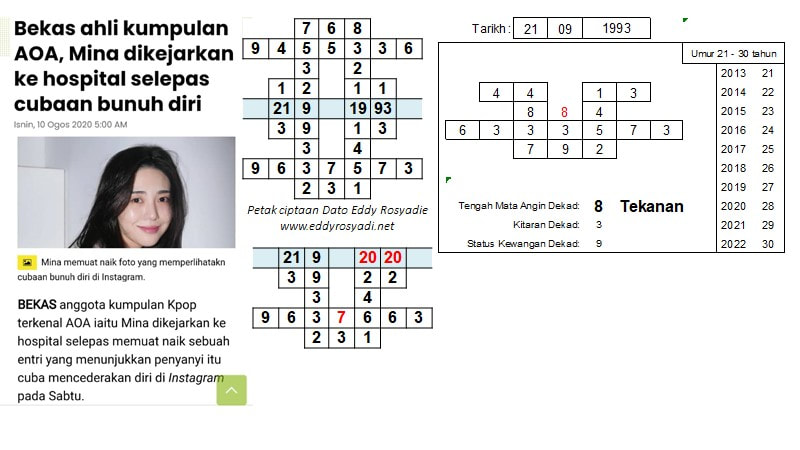

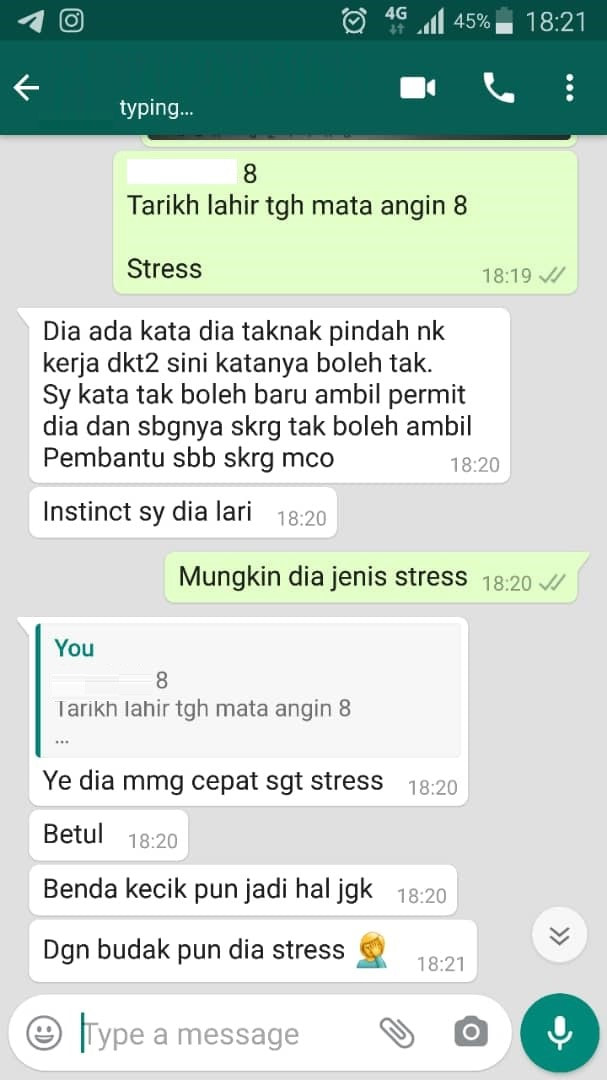

Tahun 2020 mengalami tekanan dalaman. Walaupun tahun 2020 ini ada pola 769 kekayaan yang mana pandemik Covid19 tahun 2020 ini meningkatkan keuntungan tetapi ada juga fenomena tekanan yang dialami.

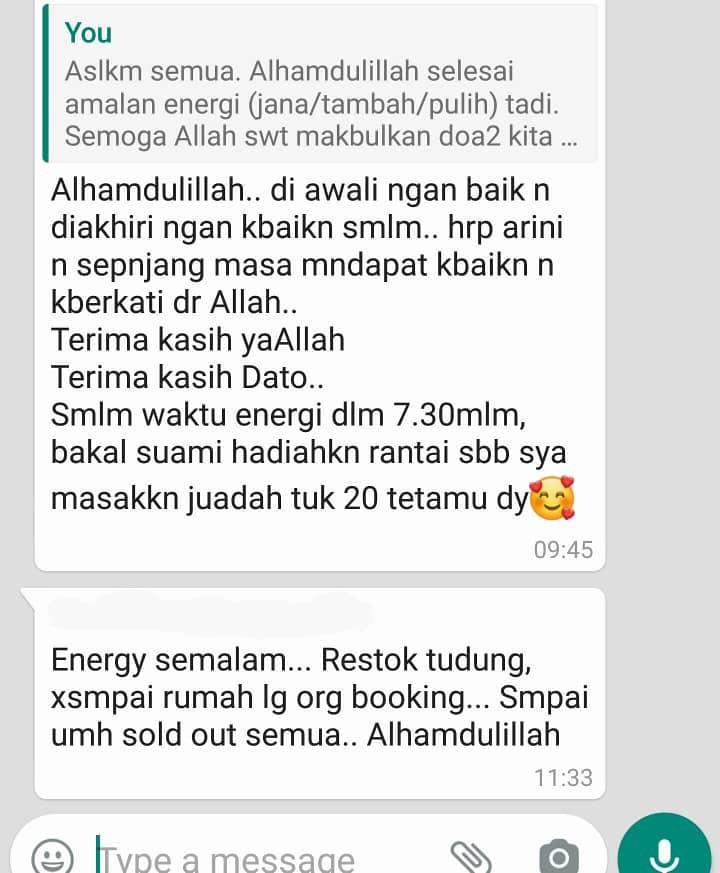

| Maklumbalas peserta Ikhtiar Energi Rezeki baru-baru ini. Kita berusaha di samping kita ikhtiarkan jana energi rezeki supaya usaha kita itu lebih berkesan. |  |

Tahun 2020 ini melalui tempoh tahun halangan dalaman (petak diwarnakan merah).

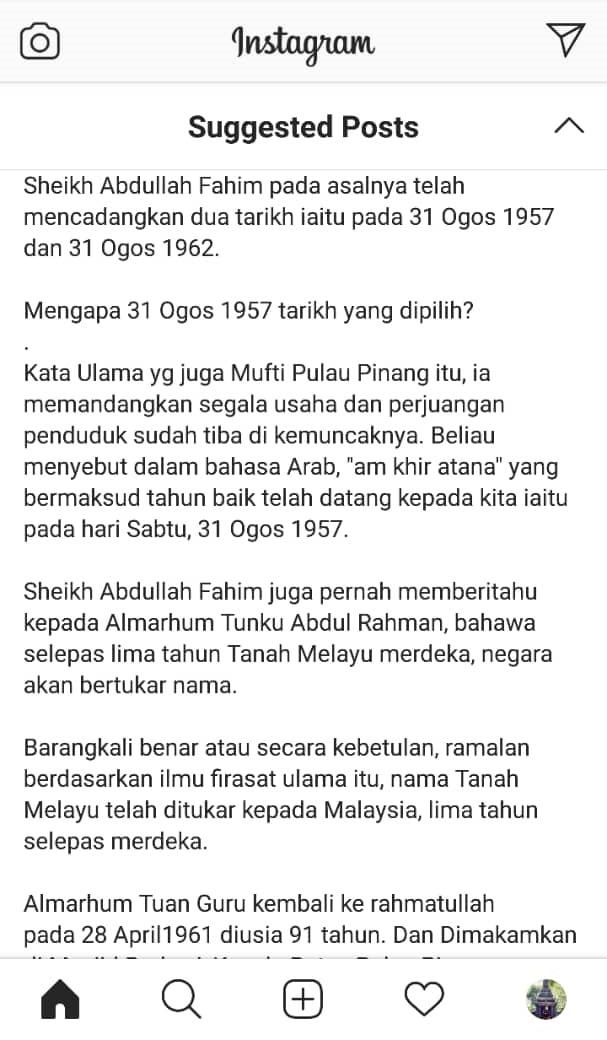

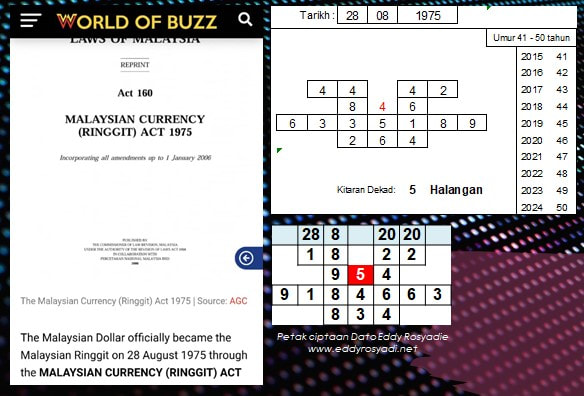

| Tarikh 31 Ogos 1957 telah dikira oleh Mufti Pulau Pinang. Ia adalah perjalanan negara Malaysia ini. Pengiraan tarikh daftar syarikat dan tarikh nikah memainkan peranan penting untuk perjalanan kehidupan kita. |  |

| Aliran metafizik terlalu banyak dan anda perlu memilih yang sebaiknya. Tentang nombor telefon adalah platform untuk komunikasi. Jika ada nombor telefon yang lebih baik dari perspektif metafizik ianya berpotensi dalam penerimaan komunikasi yang baik. Kiraan nombor telefon telah dipelopori oleh Dato Eddy Rosyadie pada tahun 2009 lalu. Ianya mula berkembang dalam seminar2 yang dianjurkan oleh Dato Eddy Rosyadie. Namun begitu, beberapa aliran metafizik yang bukan bernaung dengan Dato Eddy Rosyadie telah mengubah maksud kiraan yang dipelopori oleh Dato Eddy Rosyadie menjadikan ianya lebih merumitkan. |

Tahun 2020 dugaan yang tidak disangka2. Walaupun kami tahu Malaysia masuk kitaran 7 tahun 2020 (tahun kerugian) tapi tak adalah serugi seteruk dek akibat covid19. Jadi, kali ini kita lebih bersedia untuk hadapi 2021 yang mana Malaysia adalah kitaran 8 (31+8+2021=8) biasanya tahun 8 tahun yang STRESS. Bagaimana nak hadapi tahun stress? Apa cara2nya? Apa peluang kerjaya/ bisnes untuk tahun 2021=5 yakni tahun halangan? Kita bakala masuki tahun 2021 Halangan dan Stress. Usah pandang ringan tentang menghadapi tahun 2021 lagi. Jom, kita pelajari strategi2 dan juga persiapan untuk ke tahun 2022=6 tahun rezeki. Bagaimana untuk melalui tahun halangan 2021=5 dan kemudiannya tahun rezeki 2022=6?

|   Beberapa program Riadah Outdoor Jana Energi yang pernah Dato Eddy Rosyadie anjurkan sebelum2 ini. - Pantai Kota Kinabalu. - Resort di Pagoh - Kawasan Rekreasi Ulu Bendul - Pantai Balok Tujuan utama adalah untuk menikmat alam dengan suasana outdoor dan disamping itu menjana energi dengan alam. Kelas 20 September 2020 di Seremban adalah kelas teori dan praktikal untuk Jana Energi Positif. Sebaiknya hadir ke kelas yang ini sebelum kita beriadah Outdoor untuk memahami perihal energi dengan lebih mendalam. |

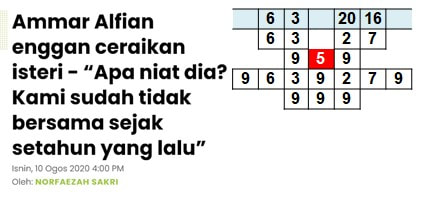

Usia dekad dalam tekanan dan tiada pola jodoh. Punyai pola berkawan dengan suami orang.

Fenomena kehidupan diperjelaskan dengan kaedah pernomboran.

Fenomena kehidupan diperjelaskan dengan kaedah pernomboran.

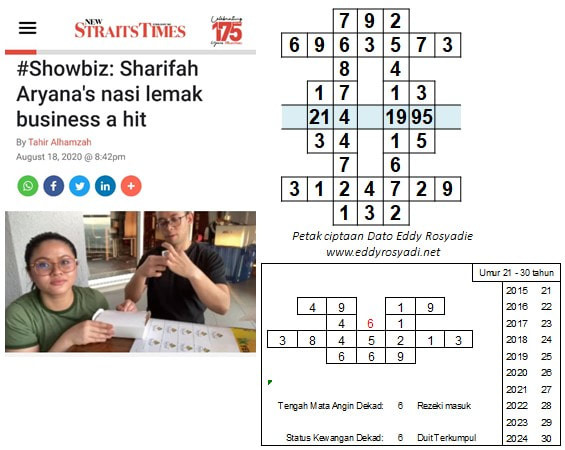

| Dunia makanan merupakan satu bidang yang tinggi permintaannya sepanjang masa. Malah, dalam Graf Hayat kita ada satu star (fenomena) digelar Cooking Star. SEMUA ORANG ada fenomena Cooking Star ini cuma berbeza usia kerana perbezaan tarikh lahir dan masa lahir. Kerana itu jika anda ada beberapa potensi diri termasuk dunia makanan, maka dunia makanan itu yang diberi keutamaan. Sama ada suka atau tidak itu perkara no 2. Yang penting potensi itu dah ada. |  |

Berada dalam tahun 2020 yang ada tekanan dan halangan.

| Dapat rezeki masuk. Menjelang kemerdekaan yang ke 63 = 9 sukses. Lagipun Malaysia tahun 2020 ini melalui tempoh Great Financier yakni berkaitan dunia kewangan. |  |

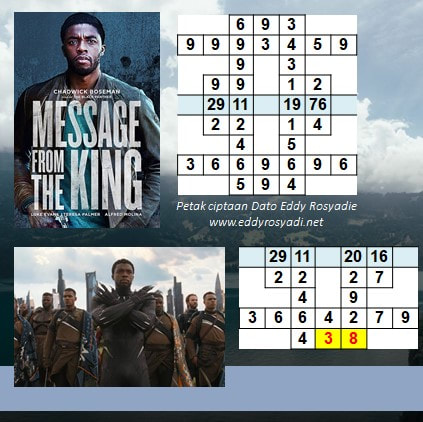

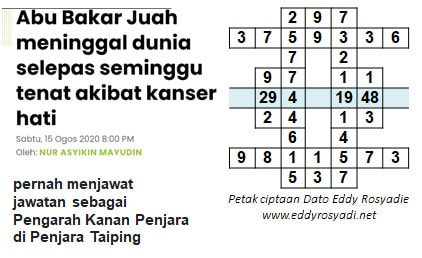

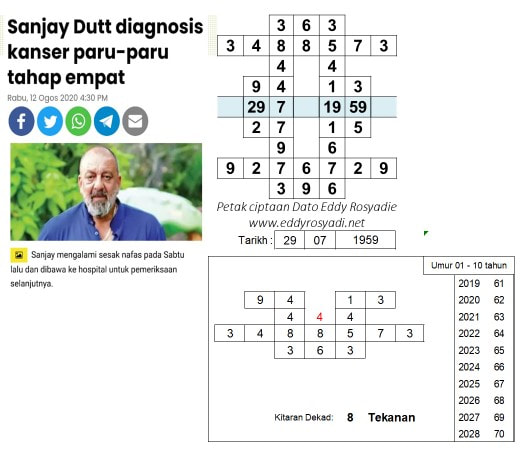

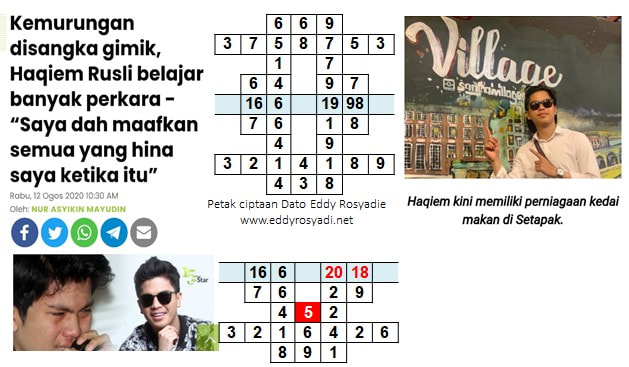

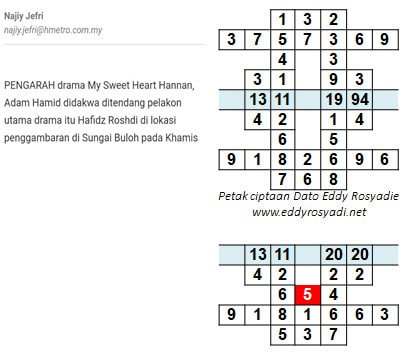

Yang hidup pasti mati itulah realiti kehidupan. Walaupun sebagai pelakon, beliau pernah menganggotai pasukan beruniform. Dalam petak tarikh lahir beliau ada potensi dunia penguatkuasaan. Malah elemen dan pola beliau juga adalah sebagai seorang Pengarah Kanan.

| Maklumbalas peserta Ikhtiar Energi Pakej Bulan Ogos 2020. Apapun ini pengalaman dirinya itu yang unik. Merasai ketenangan dari energi yang dijana pada hari dan waktu energi yang dimaklumkan. Waktu energi ada saja setiap hari tetapi berbeza2 waktunya mengikut kiraan Dato Eddy Rosyadie. Manakala waktu energi pada hari yang berpola baik dilihat lebih berkesan berbanding daripada hari-hari yang berpola biasa2. |

| Maklumbalas peserta Ikhtiar Energi Rezeki 27 Ogos 2020 lalu. Dipermudahkan rezeki pada hari energi rezeki. |  |

| Semoga mimpi yang indah menjadi kenyataan. Amin. |

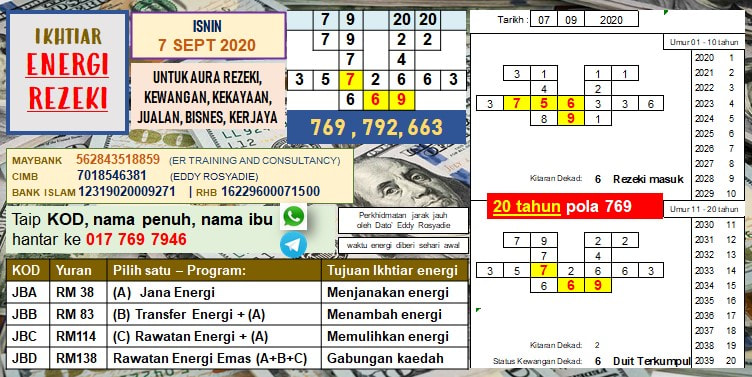

| Petak tarikh lahir statik punyai pola 769 kekayaan. Apa itu pola 769? Tentang kekayaan? Ada baik dan ada buruk pola ini? Bagaimana untuk kenali potensi pola 769 dalam petak tarikh lahir? Jom, kelas KDT (dalam aplikasi Telegram) |

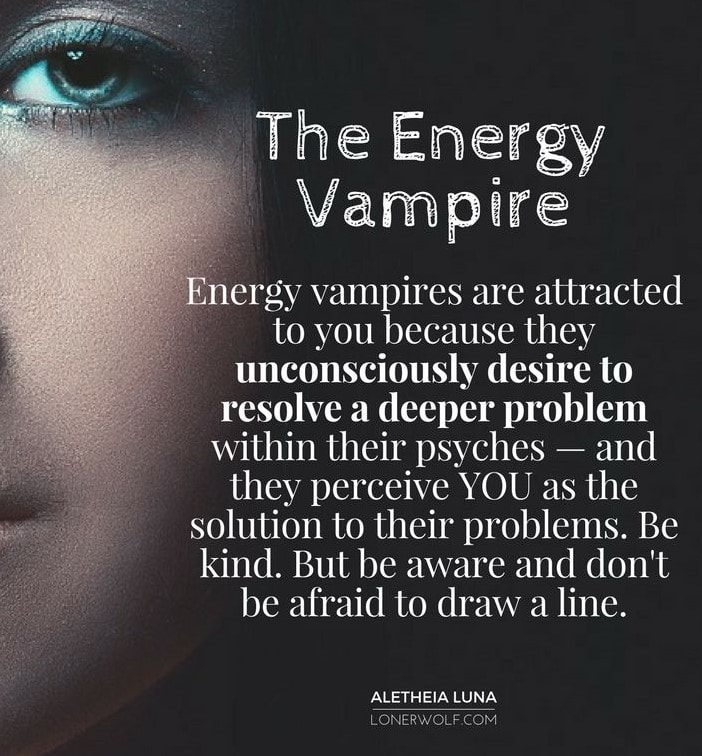

|  Bukanlah betul2 pontianak yang menghisap darah anda terang2 di siang hari, tetapi ini adalah satu contoh tentang bagaimana seseorang itu "menyedut" (vampire) energi anda menjadikan anda sentiasa letih sahaja. Ada disekeliling anda mungkin rakan pejabat, mungkin pasangan atau ahli keluarga anda sendiri. Yang penting kita teruskan menjana energi yang positif dan berkala. Majoriti "penyedut" energi tak tahu pun dirinya itu vampire (penyedut energi anda). Ketahui tentang energi dan bagaimana cara2nya untuk menjana energi positif. |

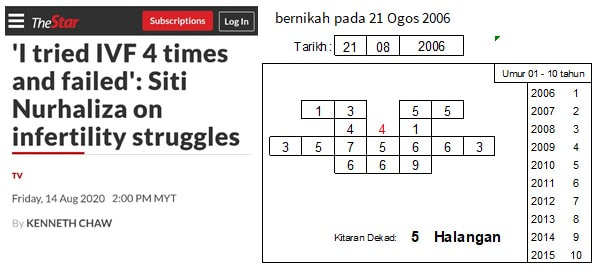

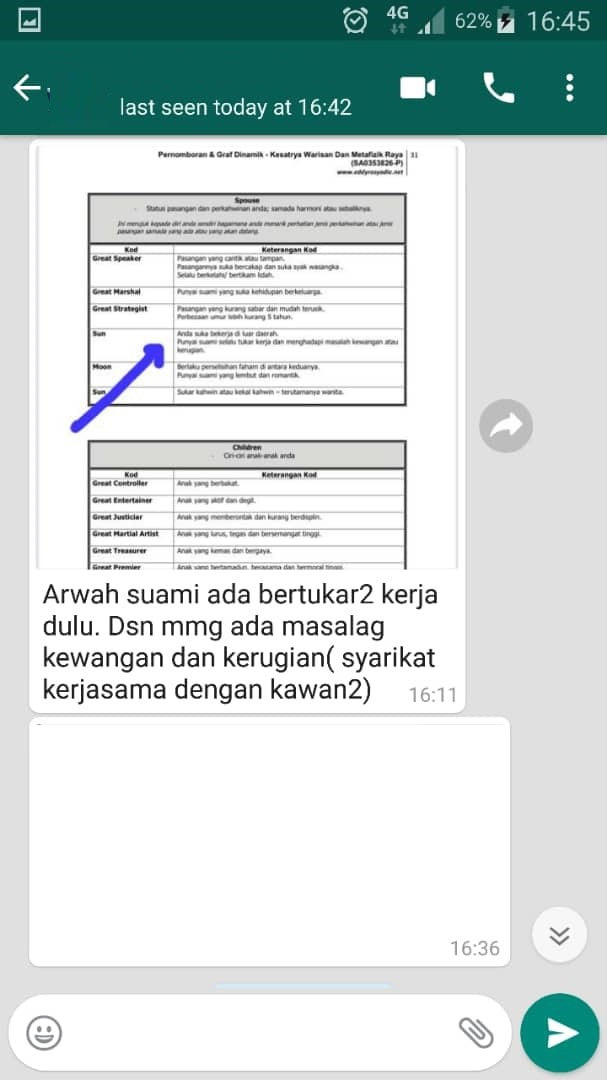

Tarikh nikah ada potensi2 konflik dan 10 tahun pertama perkahwinan mengandungi konflik halangan.

Bagaimana pula dengan tarikh nikah anda? Ada strategi yang boleh diusahakan untuk mengatasi masalah tersebut. Bagi bakal pengantin pula bagaimana pula dengan tarikh nikah yang bakal anda langsungkan? Sudah memilih tarikh nikah yang sesuai?

Bagaimana pula dengan tarikh nikah anda? Ada strategi yang boleh diusahakan untuk mengatasi masalah tersebut. Bagi bakal pengantin pula bagaimana pula dengan tarikh nikah yang bakal anda langsungkan? Sudah memilih tarikh nikah yang sesuai?

DIENERGIKAN PADA 7 SEPT 2020 (FOC):

Kuantiti Terhad (dalam gambar sahaja):

Sebiji RM10

Dua biji RM15

+ Kos Poslaju Semenanjung RM10/ Sabah Sarawak RM15

Kuantiti Terhad (dalam gambar sahaja):

Sebiji RM10

Dua biji RM15

+ Kos Poslaju Semenanjung RM10/ Sabah Sarawak RM15

DIENERGIKAN PADA 7 SEPTEMBER 2020 (FOC):

Kuantiti Terhad (dalam gambar sahaja):

Sebiji RM10

Dua biji RM15

+ Kos Poslaju Semenanjung RM10/ Sabah Sarawak RM15

Kuantiti Terhad (dalam gambar sahaja):

Sebiji RM10

Dua biji RM15

+ Kos Poslaju Semenanjung RM10/ Sabah Sarawak RM15

DIENERGIKAN PADA 7 SEPTEMBER 2020 (FOC):

Kuantiti Terhad (dalam gambar sahaja):

Kiri sekali - RM30 sebiji

Tengah - RM50 sebiji

Kanan - RM100 sebiji

Paling Kanan - RM150 sebiji (ada refleksi kilauan umpama emas)

+ Kos Poslaju Semenanjung RM10/ Sabah Sarawak RM15

Hubungi Dato Eddy Rosyadie

017 769 7946

016 624 9666

Kuantiti Terhad (dalam gambar sahaja):

Kiri sekali - RM30 sebiji

Tengah - RM50 sebiji

Kanan - RM100 sebiji

Paling Kanan - RM150 sebiji (ada refleksi kilauan umpama emas)

+ Kos Poslaju Semenanjung RM10/ Sabah Sarawak RM15

Hubungi Dato Eddy Rosyadie

017 769 7946

016 624 9666

Semua bencana alam ini berlaku dalam bulan Ogos bulan yang ke 8 di dalam tahun kiraan fenomena dunia 8 tahun 2020. Biasanya 8 itu adalah tekanan. Energi alam mengalami tekanan jadi janalah energi diri dalaman yang tenang. Berterusanlah menjana energi diri secara berkala. |   |

** Seminar hadapi Tahun 2021 dan 2022. Batch pertama di Hotel Seri Malaysia, Larkin, Johor Bahru pada Sabtu 10 Oktober 2020. Tempat terhad 40 orang.

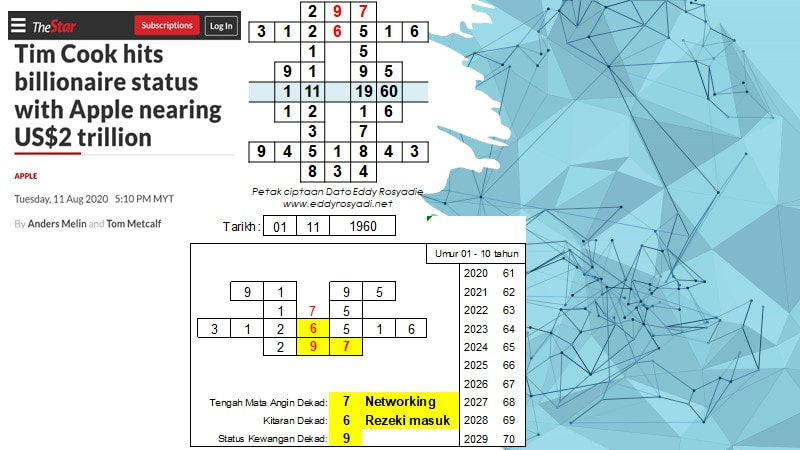

| Antara bilionair seperti Bill Gates, Mark Zuckerberg dan Jeff Bezos mendapat sokongan daripada ibu bapa yang mendapatkan "contact" dan membiayai mereka pada permulaan hidup mereka dan seterusnya mereka berusaha dari situ dan menjadi bilionair. Jutawan selebriti seperti Justin Bieber mendapat dorongan daripada ibunya yang sering upload video You Tube aksi anaknya itu sehinggalah mendapat perhatian penerbit album dan seterusnya menjadi berjaya kaya. Jadi, ibu bapa memainkan peranan dalam mencipta kekayaan anda itu. Di dalam graf hayat, ada satu tafsiran yang menyebut "dibantu oleh ibubapa" menunjukkan kejayaan seseorang itu adalah kerana ibubapa bukannya diri sendiri. Apakah laporan graf hayat anda ada tafsiran sebegitu? |  |

Antara sebab DS Siti lambat mendapat zuriat adalah kerana tempoh 10 tahun perkahwinannya ada halangan. Selepas tamat tempoh halangan barulah dapat zuriat.

| Metafizik energi sejak dulu menyatakan bahawa pokok2 mempunyai energi tersendiri dan boleh membantu manusia. Kini sains mengesahkan terdapatnya energi dalam pokok malah sains mencipta alat photosintesis tiruan. Metafizik pencetus idea sains. |

Dalam petak statik tarikh lahir anda pola mengenai sakit paru-paru dan apabila masuk ke usia dekad tekanan, ianya terjadi. Bagi individu ini, nasib baik usia dekadnya pada usia warga emas. Jikalau usia dekad remaja atau muda adalah tekanan menimbulkan masalah pula.

Bagaimana dengan anda?

- Penyakit apa yang berpotensi anda hidapi?

- bilakah usia dekad tekanan anda?

Untuk kenali potensi dan konflik kehidupan, Whatsapp/ Telegram Dato Eddy Rosyadie

0177697946

0166249666

Bagaimana dengan anda?

- Penyakit apa yang berpotensi anda hidapi?

- bilakah usia dekad tekanan anda?

Untuk kenali potensi dan konflik kehidupan, Whatsapp/ Telegram Dato Eddy Rosyadie

0177697946

0166249666

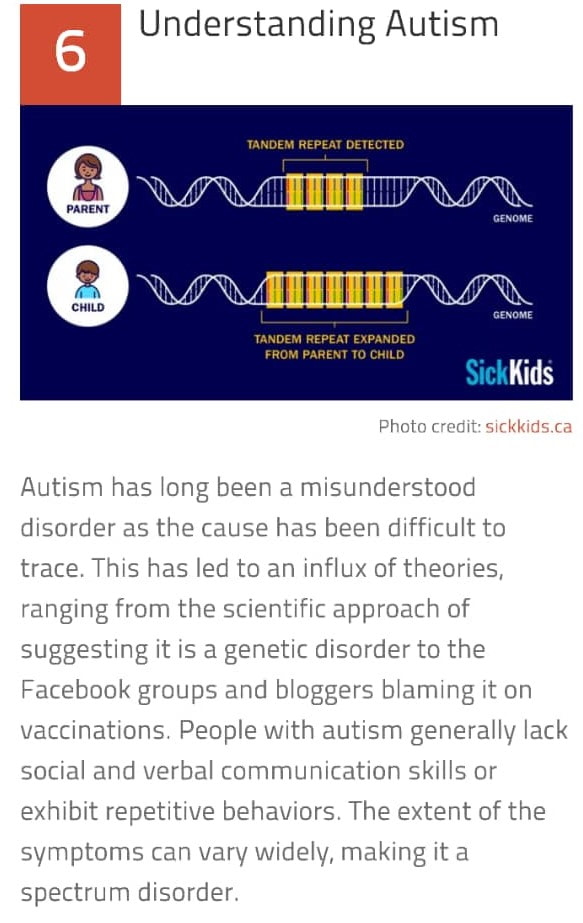

| Majoriti penyakit manusia adalah kerana perihal genetik. Seperti autisma dalam Genome ibu/bapa ada "tandem repeat" dan anak yang mengalami autisma mempunyai "tandem repeat" yang panjang. Di dalam perihal sebegini, tiadalah rawatan yang benar2 berkesan melainkan membetulkan genome DNA tersebut. Tetapi teknologi sains untuk hal tersebut masih jauh. Jadi kita berusaha dengan strategi, ikhtiar dan usaha berterusan. |  |

Petak tarikh lahir statik ada pola penyakit di bahagian kulit. Ada strategi2 pencegahan yang boleh diusahakan. Terlebih dahulu ketahui potensi dan konflik penyakit.

|  |

|

Shock proof your finances: A jobs bloodbath, pensions and savings rates slashed... but don't despair, here's how to fight back against recession

Now we are officially in the deepest recession the UK has ever known

More than 9m people have been furloughed and job losses have hit 730,000

By BEN WILKINSON FOR THE DAILY MAIL

PUBLISHED: 22:01 BST, 18 August 2020 | UPDATED: 07:55 BST, 19 August 2020

The coronavirus has had a shattering effect on the country, and we are now in the deepest recession the UK has ever known.

More than nine million people have been furloughed and 730,000 jobs have been lost.

But this Money Mail and This is Money special is here to help you revive your finances and make sure you and your family are in the best possible position as the nation fights its way out of the economic crisis.

It comes after our redundancy survival guide earlier this month. And last week we explained how you can set up your own business and take the first steps on a new career path.

The virus has cost some households dearly, with many suffering huge income losses.

Meanwhile, others have been able to save for the first time in years, as commuting costs vanished, along with the temptation to spend on dining out and holidays.

Whatever your situation, we will help you put every penny to good use as we emerge from lockdown and battle the recession.

We have spoken to Britain's top money experts, and explain how you can rebuild your finances, fill your war chest and plan for the future, whatever it may hold.

John Ellmore, director of the finance comparison site KnowYourMoney.co.uk, says: 'It is important not to panic. Rather, people must take stock.'

You will need to review your budget at regular intervals to keep on top of your spending. And don't forget to look at statements so you can prepare for big annual spends, such as Christmas and holidays.

Becky O'Connor, personal finance specialist at insurer Royal London, recommends checking your bank balance daily to keep a close eye on outgoings.

She also suggests arranging for major transactions and loan repayments to come out immediately after payday — so you know what you will have left for the rest of the month.

You could go further and work out a daily budget, too. But Ms O'Connor warns that no month is typical and you should always be prepared for unexpected expenditure.

Sarah Coles, personal finance expert at investment firm Hargreaves Lansdown, says it's worth having a 'plan B', adding: 'If your circumstances change for the worse, you need to be able to slash your costs quickly, so plan this in advance.

'This doesn't have to be a budget that you can live with for ever: it is designed to get you through the worst of circumstances.'

Seek out any chance to save

Once you have a comprehensive list of all your outgoings, you may well be shocked at how much you are spending each month.

Go through your list with a fine-tooth comb to find any unnecessary spending. When you have a total for this, you may again be surprised at how quickly it all adds up. Perhaps you pay regularly for a service you find you don't use very often, such as Amazon Prime or Netflix?

Laura Suter, personal finance analyst at investment broker AJ Bell, says: 'Work out whether you're getting value for money and still using the service — if you are not, cancel it.' But Ms Coles warns not to sacrifice all the things that make you happy — because if you are miserable, you may be more likely to bust your budget.

The internet can also help you save. Sell unwanted clutter or buy cheaply on sites such as eBay, Shpock and Facebook, or use local groups on the social media site to borrow expensive items such as lawn mowers and power tools.

Try planning meals in advance to avoid spending on takeaways, and use a food-sharing app such as Olio, where neighbours exchange food they no longer need for free.

How I lopped £1,000 off my bills

Stay-at-home dad Richard Jackson saves his family close to £1,000 every year with his switching strategy.

Richard, 39, sets reminders on his mobile phone when his energy, mobile, television and broadband deals are due to expire.

He then uses price comparison websites to seek out the cheapest offers.

Richard, who lives in Devon with his wife and two boys, says the family has managed to save more than £500 a month in lockdown after spending on meals out, petrol and outgoings plummeted.

And he has managed to bolster the family finances even further by switching energy deals from EDF to Shell Energy - saving £13 a month.

He has also pocketed £100 offered to banking customers who switch their current account to Halifax.

Richard says that anyone looking to save like him should make notes of when their household bill deals are due to expire.

He says: 'If you don't save yourself the money, the companies will just take it off you. You need to be organised. It doesn't take ten minutes to do it.

'They entice you with an introductory deal and hope you don't leave, but I will leave if the deal isn't good enough.'

The Jacksons, who also received a refund for their cancelled cruise holiday, are saving the money to help them through a major building project at the family home.

Keep up good money habits

Ask yourself what you can truly afford to save every month and commit to doing so. Set up a direct debit so the money is moved automatically on payday, then you cannot spend it.

But do not save more than you can afford — if the sum is too high, you may panic and cancel the deposits.

Ms O'Connor also recommends setting a savings target - for example, £2,000 by the end of the year.

Lockdown forced many of us into a savings habit, as we were simply unable to spend. It made us realise just how much was being lashed out on luxuries. But how can you make these good habits stick?

A Hargreaves Lansdown survey during lockdown found that about one person in three would go out less, buy fewer clothes and avoid impulse purchases in future to save money.

Meanwhile, one in five said they were likely to save on commuting costs, with employers now happier to have staff working from home.

Ms Coles suggests simply thinking twice about 'habitual' spending - so consider whether you really need something before plucking it off the shelf in a shop. You might also try giving yourself 24 hours before buying anything new, to avoid impulse purchases.

If you think it would help, you could make it harder for yourself to spend rashly by removing any card details saved online and by unsubscribing from emails sent by stores which tempt you to spend.

Go hunting for better deals

The largest monthly outgoing for most households is the mortgage - and this is perhaps where the biggest saving can be found.

If you are on your lender's standard variable rate, it is likely you can get a better deal.

Rates hit record lows in June, before the average rates for both two and five-year fixed-rate deals fell even further to 1.99 per cent and 2.25 per cent respectively last month. So now is the ideal time to lock in to a cheap deal.

Ms Suter says: 'Once you've tackled that big outgoing, look at bills that have crept up. Whether it's switching to a cheaper energy deal, realising your Sky package has shot up in price, or cutting the cost of your car insurance, there's lots you can do just by going on a comparison website and hunting for a new deal.'

You can sign up to an energy supplier auto-switching service such as Switchd or Flipper. They will move you to the cheapest deal automatically, taking the hassle out of switching and removing the need to worry that you are not on a good rate.

Ms O'Connor adds: 'Deals and rates change all the time, but no one is going to tell you. It's up to you to be aware of what is available.'

The comparison site Uswitch estimates that fixed energy plans used by 1.5 million households will end this summer — and that those homeowners could save an average £149 a year if they sought out a better one.

Energy prices are now relatively low, making this the perfect time to switch tariffs.

Sarah Broomfield, energy expert at Uswitch, says: 'Now is a crucial time to bag yourself a new deal, before you get dumped on your supplier's standard variable tariff.'

About a third of broadband customers are thought to be paying more than they should because their contracts have run out. And finding a decent internet deal is more important now than ever, as so many people are working from home.

The soaring cost of new mobile phones also presents an opportunity to save: instead of upgrading to the latest model, keep your current phone and move to a Sim-only deal when your contract ends.

Uswitch says someone who bought an iPhone two years ago on an average 24-month contract could save £600 by switching to a Sim-only deal with the same amount of data and minute allowances.

Go through your outgoings list with a fine-tooth comb to find any unnecessary spending. When you have a total, you may again be surprised at how much this adds up to every month +5

Go through your outgoings list with a fine-tooth comb to find any unnecessary spending. When you have a total, you may again be surprised at how much this adds up to every month

Get organised to deal with debt

Charity StepChange predicted that 4.6 million people would together rack up £6 billion in debts during the crisis, while millions will have taken payment holidays from mortgages and loan repayments.

Ms Coles says: 'For some people, cuts in income or losing work has meant a horrible battle to make ends meet, forcing them to max-out on debt. If you're in this position, it's time to take stock and assess how to stop things getting worse.'

Debts with the highest interest-rate charges should be cleared first. If you cannot pay off your debt any time soon, you could at least shift it to a cheaper rate - for instance, with a 0 per cent credit card or a personal loan with a low rate.

Ms Suter says: 'This means you can use more of your capital to pay down the actual debt each month, rather than just paying off the interest.'

If you were forced to ask your bank or building society for a three-month mortgage payment holiday, it is worth remembering that you will now owe more interest. Taking such a break will increase debt by more than £1,000 on a typical mortgage.

Also, bear in mind that overdrafts are no longer a cheap and convenient way to borrow. After orders from the regulator to make fees fairer and simpler, most major banks have brought in charges of up to 50 per cent.

For vulnerable borrowers who use their overdrafts without permission, the charges will probably mean they pay less. But those who dip in and out of an agreed overdraft could find it is a very expensive way to borrow.

If you need to take out a loan, local credit unions may offer the fairest rates around. These mutual organisations act in the best interests of their members. Find your nearest at abcul.coop/home.

Mr Ellmore, from KnowYourMoney.co.uk, says it is also important to maintain a strong credit score, so bills should be paid on time if possible. This will put you in the best position if you need to apply for a loan.

Yet Ms Coles says it is now worth drawing a line under taking on more debt. 'There is no point in working hard to pay it all back if you are still prepared to run up debts,' she says. 'If this is going to be a life-long change, you need to commit to steering clear of needless debt for good.'

Fresh figures, from the banking body UK Finance, yesterday showed credit card debt had fallen by 12.6 per cent so far this year.

Start building a safety net

Once you have cleared any debts and boosted your savings, you can focus on building a safety net in case you lose your job or face unexpected costs.

One adult in eight in Britain has no savings at all, and 45 per cent of the country has less than £2,000 put away.

Experts say it is a good idea to build up an emergency fund to last between three and six months, to cover essential outgoings such as mortgage or rent payments, household bills and food.

This pot of money should be left in an easy-access savings account, even though these might not offer the most generous interest rates.

After the Bank of England slashed the base rate to a record low of 0.1 per cent, all High Street banks cut their savings rates to a pittance at 0.01 per cent. But you can still earn at least 1 per cent more by finding a top-paying account.

Ms Suter says: 'The Bank of England cutting rates and the high demand for savings accounts means you're not going to get loads of interest. But far too much money is sitting in current accounts earning nothing, or old savings accounts that pay a pittance.'

If you have lost your job, you may also have lost important benefits, such as pension payments and insurance.

Unemployment and redundancy policies have been pulled from the market because of the pandemic, but you can still buy income protection and critical illness cover.

Free investing guides

Income protection will pay a tax-free wage if you cannot work due to health problems.

Critical illness cover, meanwhile, will pay out a lump sum to cover mortgage payments and financial security if you have a serious health condition diagnosed.

The price of the policy will depend on individual circumstances, including your age, health, occupation and smoking history, but the average premium is about £25 to £30 a month.

Protection insurance specialist Kevin Carr says: 'If you, or anybody else, relies on your salary to pay the bills, [these policies are] worth thinking about.'

Don't hesitate to ask for help

There is no shame in asking for help or claiming benefits if you find yourself struggling.

Ms O'Connor says: 'Managing finances is hard at the best of times - but at the worst of times, it can feel impossible without falling into debt.

'No one wants anyone to go hungry or have their home repossessed. There is always help if you know where to look.'

She adds: 'As a rule, if you lose your job or a big chunk of income, there is probably some form of help out there for you, so don't suffer alone. When it comes to money problems, prevention is always better than cure.'

https://www.thisismoney.co.uk/money/news/article-8639115/How-shock-proof-finances-Protect-family-recession.html

Now we are officially in the deepest recession the UK has ever known

More than 9m people have been furloughed and job losses have hit 730,000

By BEN WILKINSON FOR THE DAILY MAIL

PUBLISHED: 22:01 BST, 18 August 2020 | UPDATED: 07:55 BST, 19 August 2020

The coronavirus has had a shattering effect on the country, and we are now in the deepest recession the UK has ever known.

More than nine million people have been furloughed and 730,000 jobs have been lost.

But this Money Mail and This is Money special is here to help you revive your finances and make sure you and your family are in the best possible position as the nation fights its way out of the economic crisis.

It comes after our redundancy survival guide earlier this month. And last week we explained how you can set up your own business and take the first steps on a new career path.

The virus has cost some households dearly, with many suffering huge income losses.

Meanwhile, others have been able to save for the first time in years, as commuting costs vanished, along with the temptation to spend on dining out and holidays.

Whatever your situation, we will help you put every penny to good use as we emerge from lockdown and battle the recession.

We have spoken to Britain's top money experts, and explain how you can rebuild your finances, fill your war chest and plan for the future, whatever it may hold.

John Ellmore, director of the finance comparison site KnowYourMoney.co.uk, says: 'It is important not to panic. Rather, people must take stock.'

You will need to review your budget at regular intervals to keep on top of your spending. And don't forget to look at statements so you can prepare for big annual spends, such as Christmas and holidays.

Becky O'Connor, personal finance specialist at insurer Royal London, recommends checking your bank balance daily to keep a close eye on outgoings.

She also suggests arranging for major transactions and loan repayments to come out immediately after payday — so you know what you will have left for the rest of the month.

You could go further and work out a daily budget, too. But Ms O'Connor warns that no month is typical and you should always be prepared for unexpected expenditure.

Sarah Coles, personal finance expert at investment firm Hargreaves Lansdown, says it's worth having a 'plan B', adding: 'If your circumstances change for the worse, you need to be able to slash your costs quickly, so plan this in advance.

'This doesn't have to be a budget that you can live with for ever: it is designed to get you through the worst of circumstances.'

Seek out any chance to save

Once you have a comprehensive list of all your outgoings, you may well be shocked at how much you are spending each month.

Go through your list with a fine-tooth comb to find any unnecessary spending. When you have a total for this, you may again be surprised at how quickly it all adds up. Perhaps you pay regularly for a service you find you don't use very often, such as Amazon Prime or Netflix?

Laura Suter, personal finance analyst at investment broker AJ Bell, says: 'Work out whether you're getting value for money and still using the service — if you are not, cancel it.' But Ms Coles warns not to sacrifice all the things that make you happy — because if you are miserable, you may be more likely to bust your budget.

The internet can also help you save. Sell unwanted clutter or buy cheaply on sites such as eBay, Shpock and Facebook, or use local groups on the social media site to borrow expensive items such as lawn mowers and power tools.

Try planning meals in advance to avoid spending on takeaways, and use a food-sharing app such as Olio, where neighbours exchange food they no longer need for free.

How I lopped £1,000 off my bills

Stay-at-home dad Richard Jackson saves his family close to £1,000 every year with his switching strategy.

Richard, 39, sets reminders on his mobile phone when his energy, mobile, television and broadband deals are due to expire.

He then uses price comparison websites to seek out the cheapest offers.

Richard, who lives in Devon with his wife and two boys, says the family has managed to save more than £500 a month in lockdown after spending on meals out, petrol and outgoings plummeted.

And he has managed to bolster the family finances even further by switching energy deals from EDF to Shell Energy - saving £13 a month.

He has also pocketed £100 offered to banking customers who switch their current account to Halifax.

Richard says that anyone looking to save like him should make notes of when their household bill deals are due to expire.

He says: 'If you don't save yourself the money, the companies will just take it off you. You need to be organised. It doesn't take ten minutes to do it.

'They entice you with an introductory deal and hope you don't leave, but I will leave if the deal isn't good enough.'

The Jacksons, who also received a refund for their cancelled cruise holiday, are saving the money to help them through a major building project at the family home.

Keep up good money habits

Ask yourself what you can truly afford to save every month and commit to doing so. Set up a direct debit so the money is moved automatically on payday, then you cannot spend it.

But do not save more than you can afford — if the sum is too high, you may panic and cancel the deposits.

Ms O'Connor also recommends setting a savings target - for example, £2,000 by the end of the year.

Lockdown forced many of us into a savings habit, as we were simply unable to spend. It made us realise just how much was being lashed out on luxuries. But how can you make these good habits stick?

A Hargreaves Lansdown survey during lockdown found that about one person in three would go out less, buy fewer clothes and avoid impulse purchases in future to save money.

Meanwhile, one in five said they were likely to save on commuting costs, with employers now happier to have staff working from home.

Ms Coles suggests simply thinking twice about 'habitual' spending - so consider whether you really need something before plucking it off the shelf in a shop. You might also try giving yourself 24 hours before buying anything new, to avoid impulse purchases.

If you think it would help, you could make it harder for yourself to spend rashly by removing any card details saved online and by unsubscribing from emails sent by stores which tempt you to spend.

Go hunting for better deals

The largest monthly outgoing for most households is the mortgage - and this is perhaps where the biggest saving can be found.

If you are on your lender's standard variable rate, it is likely you can get a better deal.

Rates hit record lows in June, before the average rates for both two and five-year fixed-rate deals fell even further to 1.99 per cent and 2.25 per cent respectively last month. So now is the ideal time to lock in to a cheap deal.

Ms Suter says: 'Once you've tackled that big outgoing, look at bills that have crept up. Whether it's switching to a cheaper energy deal, realising your Sky package has shot up in price, or cutting the cost of your car insurance, there's lots you can do just by going on a comparison website and hunting for a new deal.'

You can sign up to an energy supplier auto-switching service such as Switchd or Flipper. They will move you to the cheapest deal automatically, taking the hassle out of switching and removing the need to worry that you are not on a good rate.

Ms O'Connor adds: 'Deals and rates change all the time, but no one is going to tell you. It's up to you to be aware of what is available.'

The comparison site Uswitch estimates that fixed energy plans used by 1.5 million households will end this summer — and that those homeowners could save an average £149 a year if they sought out a better one.

Energy prices are now relatively low, making this the perfect time to switch tariffs.

Sarah Broomfield, energy expert at Uswitch, says: 'Now is a crucial time to bag yourself a new deal, before you get dumped on your supplier's standard variable tariff.'

About a third of broadband customers are thought to be paying more than they should because their contracts have run out. And finding a decent internet deal is more important now than ever, as so many people are working from home.

The soaring cost of new mobile phones also presents an opportunity to save: instead of upgrading to the latest model, keep your current phone and move to a Sim-only deal when your contract ends.

Uswitch says someone who bought an iPhone two years ago on an average 24-month contract could save £600 by switching to a Sim-only deal with the same amount of data and minute allowances.

Go through your outgoings list with a fine-tooth comb to find any unnecessary spending. When you have a total, you may again be surprised at how much this adds up to every month +5

Go through your outgoings list with a fine-tooth comb to find any unnecessary spending. When you have a total, you may again be surprised at how much this adds up to every month

Get organised to deal with debt

Charity StepChange predicted that 4.6 million people would together rack up £6 billion in debts during the crisis, while millions will have taken payment holidays from mortgages and loan repayments.

Ms Coles says: 'For some people, cuts in income or losing work has meant a horrible battle to make ends meet, forcing them to max-out on debt. If you're in this position, it's time to take stock and assess how to stop things getting worse.'

Debts with the highest interest-rate charges should be cleared first. If you cannot pay off your debt any time soon, you could at least shift it to a cheaper rate - for instance, with a 0 per cent credit card or a personal loan with a low rate.

Ms Suter says: 'This means you can use more of your capital to pay down the actual debt each month, rather than just paying off the interest.'

If you were forced to ask your bank or building society for a three-month mortgage payment holiday, it is worth remembering that you will now owe more interest. Taking such a break will increase debt by more than £1,000 on a typical mortgage.

Also, bear in mind that overdrafts are no longer a cheap and convenient way to borrow. After orders from the regulator to make fees fairer and simpler, most major banks have brought in charges of up to 50 per cent.

For vulnerable borrowers who use their overdrafts without permission, the charges will probably mean they pay less. But those who dip in and out of an agreed overdraft could find it is a very expensive way to borrow.

If you need to take out a loan, local credit unions may offer the fairest rates around. These mutual organisations act in the best interests of their members. Find your nearest at abcul.coop/home.

Mr Ellmore, from KnowYourMoney.co.uk, says it is also important to maintain a strong credit score, so bills should be paid on time if possible. This will put you in the best position if you need to apply for a loan.

Yet Ms Coles says it is now worth drawing a line under taking on more debt. 'There is no point in working hard to pay it all back if you are still prepared to run up debts,' she says. 'If this is going to be a life-long change, you need to commit to steering clear of needless debt for good.'

Fresh figures, from the banking body UK Finance, yesterday showed credit card debt had fallen by 12.6 per cent so far this year.

Start building a safety net

Once you have cleared any debts and boosted your savings, you can focus on building a safety net in case you lose your job or face unexpected costs.

One adult in eight in Britain has no savings at all, and 45 per cent of the country has less than £2,000 put away.

Experts say it is a good idea to build up an emergency fund to last between three and six months, to cover essential outgoings such as mortgage or rent payments, household bills and food.

This pot of money should be left in an easy-access savings account, even though these might not offer the most generous interest rates.

After the Bank of England slashed the base rate to a record low of 0.1 per cent, all High Street banks cut their savings rates to a pittance at 0.01 per cent. But you can still earn at least 1 per cent more by finding a top-paying account.

Ms Suter says: 'The Bank of England cutting rates and the high demand for savings accounts means you're not going to get loads of interest. But far too much money is sitting in current accounts earning nothing, or old savings accounts that pay a pittance.'

If you have lost your job, you may also have lost important benefits, such as pension payments and insurance.

Unemployment and redundancy policies have been pulled from the market because of the pandemic, but you can still buy income protection and critical illness cover.

Free investing guides

Income protection will pay a tax-free wage if you cannot work due to health problems.

Critical illness cover, meanwhile, will pay out a lump sum to cover mortgage payments and financial security if you have a serious health condition diagnosed.

The price of the policy will depend on individual circumstances, including your age, health, occupation and smoking history, but the average premium is about £25 to £30 a month.

Protection insurance specialist Kevin Carr says: 'If you, or anybody else, relies on your salary to pay the bills, [these policies are] worth thinking about.'

Don't hesitate to ask for help

There is no shame in asking for help or claiming benefits if you find yourself struggling.

Ms O'Connor says: 'Managing finances is hard at the best of times - but at the worst of times, it can feel impossible without falling into debt.

'No one wants anyone to go hungry or have their home repossessed. There is always help if you know where to look.'

She adds: 'As a rule, if you lose your job or a big chunk of income, there is probably some form of help out there for you, so don't suffer alone. When it comes to money problems, prevention is always better than cure.'

https://www.thisismoney.co.uk/money/news/article-8639115/How-shock-proof-finances-Protect-family-recession.html

RSS Feed

RSS Feed