| Maklumbalas peserta2 Grup Ikhtiar Energi Ogos 2020. Semasa menjana energi pada 18 Ogos 2020 lalu tarikh energi rezeki, kehadiran bayangan ombak laut dan warna biru. Rupanya peserta2 juga terkesan dengan kehadiran energi sedemikian. |  |

| Petak tarikh lahir statik ada pola 769 kekayaan. Dengan Status Kewangan 9 iaitu aset punyai 3 hotel miliknya. Tentang pola 769 kekayaan; ada baik dan buruk? Mari kita belajar tentang pola 769 dengan lebih detail dalam KDT 769 Bahagian 1 (kelas dalam aplikasi Telegram). |

| Sejak dulu lagi, Metafizik Energi menyatakan bahawa badan manusia punyai energi. Kini sains mendapati bahawa lemak pada badan manusia boleh simpan energi. Sains menjelaskan metafizik. Metafizik pencetus idea sains. Cuma sains belum lagi menemui jenis2 energi tersebut. |  |

Begitu banyak pola 6 termasuk tengah mata angin 6 Rezeki Masuk. Tahun 2020 juga tengah mata angin 6 Rezeki Masuk.

| Kaedah perubatan alternatif adalah juga di bawah Metafizik kerana ianya kaedah yang tidak boleh ditafsirkan secara fizikal atau di luar logik. Jadi, selama ini penggunaan madu (honey) untuk kesihatan cuma kaedah perubatan alternatif. Tetapi kini sains menyatakan madu (honey) lebih berkesan daripada ubat2an sains yang fizikal. Metafizik pencetus idea sains. |  |

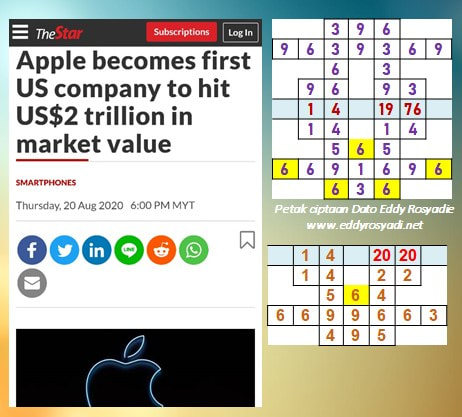

| Apakah anda ada pola potensi pemborong dan peruncit? Ini peluang kerjaya/ bisnes untuk anda. Nilai RM1 Trilion sangat besar dan sebaiknya diambil peluang oleh individu yang ada pola potensi pemborong dan peruncit. |  |

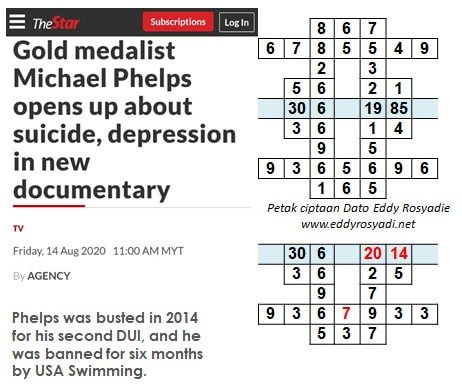

Petak statik tarikh lahir mengandungi pola potensi untuk kemurungan/ depression. Pada tahun 2014 kitaran tahun 7 tahun ujian, kehilangan dan kerugian.

| Bulan Ogos. Bulan ke 8 dalam tahun fenomena dunia 8. Angka 8 ditafsirkan sebagai elemen API. Suasana panas dan tekanan. |  |

| Peserta Grup Ikhtiar Energi Ogos 2020. Pada 17 Ogos 2020 lalu, Dato Eddy Rosyadie menjana energi untuk peserta2 grup pada waktu energi hari tersebut iaitu jam 7.30 malam. Tidak dapat dipastikan bagaimana ini terjadi dan tujuannya. Besar kemungkinan ia seolah "mandian bunga" secara energi/ kebatinan tanpa menggunakan bahan seperti air atau bunga2an. |  |

| Sejak berkurun lagi Metafizik Energi menyatakan batu kristal mengandungi energi tertentu. Kini sains mendapati batu kristal mengandungi energi malah digunakan sebagai penentu masa dengan konsep frekuensi dari batu kristal. Metafizik pencetus idea sains. |

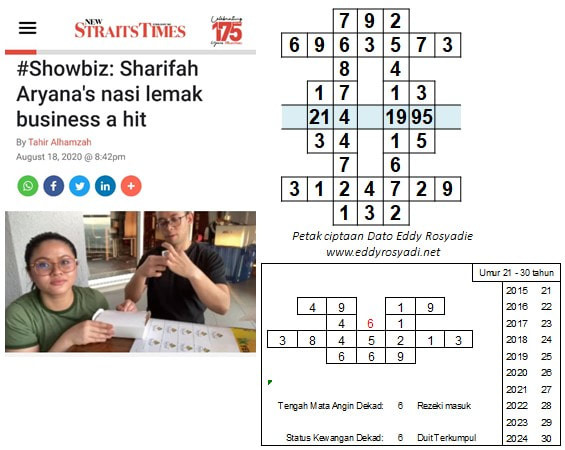

Dalam petak tarikh lahir statik tiada pola makanan tetapi dalam dekad usia antara 2015-2024 ada pola makanan. Jadi potensi kita boleh jadi berbeza pada dekad tertentu. Iaitu tidak terhad pada petak tarikh lahir statik semata-mata. Potensi pada petak tarikh lahir statik memang dijadikan panduan utama untuk menentukan kerjaya/ bisnes manakala potensi dekad usia boleh menjadi potensi kerjaya/ bisnes sementara.

| Senarai pekerjaan/ perniagaan yang diperlukan pada tahun 2020 ini. Tahun 2020=4 elemen KAYU antaranya kesihatan dan farmaseutikal, pendidikan. Tahun 2021=5 elemen TANAH antaranya pembinaan. |  |

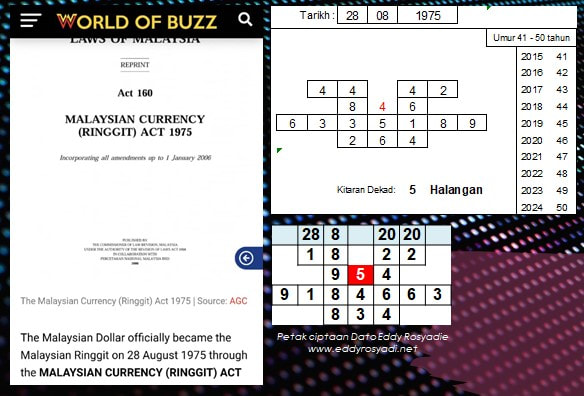

Malaysia Ringgit (MYR) dalam tempoh dekad halangan bermula dari 2015 (kes harga minyak jatuh dan Ringgit Malaysia juga jatuh) hingga tahun 2024. Matawang bermasalah dan ekonomi pun terjejas dan kekayaan rakyat Malaysia terkesan. Pada tahun 2020 ini pula halangan (pandemik Covid19 menjejaskan MYR).

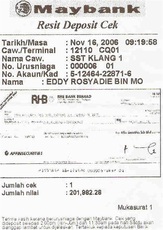

| Kasultanan Pajang yang terletak di Solo, Indonesia lenyap pada tahun 1586 setelah 30 tahun didirikan oleh seorang pendekar terkenal bernama Jaka Tingkir. Pada 26 Mei 2011, Sultan Demak melantik seorang Sultan Pajang untuk mewujudkan kembali sejarah dan warisan budaya. Tarikh tersebut ada pola 83 kesultanan. Tahun 2018-2019, Dato Eddy Rosyadie telah 3 kali menziarahi Karaton Kasultanan Pajang dan menjadi ahli VIP Karaton. |  |

|  |

|

How to recession-proof your finances

The UK economy is officially in recession for the first time since the financial crisis ten years ago.

The economy plunged by 20 per cent between April and June as the pandemic shuttered businesses and kept people locked up at home.

More jobs are likely to be lost and personal finances will take a hit.

Lynn Beattie, Personal Finance Expert at mrsmummypenny.co.uk and author of The Money Guide to Transform Your Life, which will be released on September 1, says: "We are starting to see the impact of covid-19 with many retailers closing branches, including giants like Boots and John Lewis. There will be many more casualties over the remainder of 2020 and well into 2021.”

Audit your finances and live within your means

“Firstly, it is vital to be completely honest with yourself about your financial situation,” John Ellmore, Director of KnowYourMoney.co.uk advises. “Conduct a thorough audit of your finances and gain a comprehensive understanding of all your incomes and outgoings. This will show you exactly where your cash is going and, most importantly, help you identify problematic spending behaviour.”

Ellmore adds that when you’ve figured out how you’re spending money, it’s time to be strict with yourself and don’t make any unnecessary spending. “Living within your means is vital to help avoid any major shocks to your bank balance. Further, any money you can save should be put away in an emergency fund for a rainy day. Hopefully, you won’t need to use it, but it is reassuring to have a financial cushion to fall back on should the worst happen.”

Set up an emergency fund

If you have any money to spare, now would be a good time to think about starting an emergency fund.

“Having an easily accessible emergency fund is essential for surviving a recession. Prepare this as early as possible, particularly if you are still working and you have excess money from savings made during covid-19,” Beattie advises.

“This emergency fund should be able to keep you going for between three to six months, six months is my guidance. Keep it in a separate account that has instant access. This money should remain untouched unless it is a real emergency, for example, money needed to pay the mortgage, or to buy food. Not to be used for holidays or things that you want rather than need.”

Ellmore agrees, and says that if you’re working from home, now is the ideal time to set up an emergency fund. “Take advantage of having regular income and save any extra cash that you can. Be strict with yourself. Refrain from online shopping and stash money away in a savings account. It will definitely ease your worries, knowing that you have money set aside for if the worst happens.

“Firstly, decide the total you want to save. Having an end goal will narrow your focus and give you something concrete to work towards. Regularly assess and re-evaluate your savings strategy. Life is unpredictable and, at times, you won’t be able to save as much as you would like to. So, make sure your savings efforts reflect this and adjust your goals to make them achievable and keep you motivated. Starting an emergency fund might take discipline, but it will definitely help you sleep at night.”

Furloughed workers should be planning for the future

Beattie says that everyone should be looking towards and planning for the future. “What are the chances of the business you work for going into financial difficulties, is there a chance that you might lose your job? Talk to your employer to understand what is happening. The emergency fund is an essential for furloughed workers with a risk of losing their job.”

Ellmore adds that while income will be slightly less while furloughed, you still need to be saving where you can.

He continues: “While the government is putting schemes in place to protect as many jobs as possible, it’s important to give yourself solid financial backing, in case your company is unable to bring you back.

“Make sure you are up to date with debt repayments and having a clear line of communication with your creditor will also help. Keeping your creditor in the loop could mean that, if you find yourself struggling with repayments, your payment schedule could be adjusted, without damaging your credit score.”

Redundant workers need to understand what they are owed

Ellmore says redundant workers need to understand what they are owed - the rule of thumb for statutory redundancy pay depends on the number of years an employee has worked at the company and the amount they have earned. “If in doubt, review your contract. Understanding how much you are due to receive will help you organise your finances in the long term. “

Redundant workers also need to look at ways of making extra money. Beattie says: “Have a big declutter and sell clothes, bags, electronics, old mobile phones. Use sites like Facebook Marketplace, eBay, Gumtree to make some quick cash.

“Is there a side hustle that you can start? What are your skills and how can these be used to make some extra money. Maybe you love walking dogs, maybe you can knit, maybe you are a brilliant photographer, whatever it is, use your skills to make some extra money.”

A budget is imperative

The first step for anyone who has recently been made redundant or is looking to save money, Beattie says, is to do a ‘deep dive’ into your budget.

“Have a clear idea of what essential bills you must pay. Get rid of any unnecessary direct debits and call every company that falls under essential bills to ensure you are on the best deal,” Beattie says. “Use comparison sites to compare deals and switch to a cheaper energy company, broadband, mobile phone, insurance company. When you have worked through your budget you will know how much each month costs you, and how long any redundancy money will last.”

Eesha Mohindra, senior money analyst at MoneySavingExpert.com, says a common mistake when budgeting is to only look at your spending from one to three months.

“Rarely do people look at the whole year – which includes big one-off payments like car insurance, holidays, birthdays and Christmas. So, look at least a years’ worth of statements and write down every category you spend in. There are free budget planner tools available online at moneysavingexpert.com/budgetplanner which makes things very easy for you,” Mohindra adds.

“Within your budget make sure you include how much you want to save each month. Many people just think of saving whatever they have left over each month, rather than factoring it in as a part of their monthly budget.”

Mohindra says the easiest way to factor in saving to your budget is to set up ‘piggybacking’ accounts - several accounts where you can automatically syphon money to save.

“For example, set up individual accounts for household bills, birthdays, holidays, Christmas and emergency fund. That way you have a set amount of money in each account and can’t spend more. If you have only £300 in your holiday fund it means you can’t pay for a £500 holiday.”

Remove any unnecessary payments

Mohindra says one of the easiest places to start saving is by looking at your bank account and removing any pain-free direct debits.

“Are you paying for anything you no longer use like insurance for an old mobile phone, or council tax for a home you no longer live in? If you spot these, call up the company and cancel them. Then look for things you’re currently paying for but could be getting cheaper,” Mohindra adds.

“When was the last time you switched energy tariffs, home insurance, car insurance, broadband, TV package, mobile tariff – don’t let these auto-renew onto expensive out of contract rates. Do a comparison online to see if you can get it cheaper elsewhere or if you want to stick to the same provider then at least consider haggling. For the things you don’t need but do want, ask yourself, is it worth it? Is the gain you get worth the money? Think in annual cost, £8 a month is £100 a year – so if it's a TV subscription you only use a few times or a gym membership you rarely go to, is it worth it? If not, cancel or try and find something cheaper.”

Don’t make impulse purchases

Beattie recommends thinking about a purchase for at least 24 hours before you buy it. “Think about what you are buying, do you really need it, or is it a want. I recently counted my blouses, and have 22, I do not need any more blouses.

“Pop the item into an online basket and come back the next day, you might have changed your mind, and also the company might send you a discount voucher to encourage a purchase.”

Start a spending diary

Beattie also recommends starting a spending diary to keep track of your daily purchases and bills to understand what you buy and why. She adds: “If writing a diary fills you with dread, download an app like Money Dashboard that will consolidate all your accounts to help you to understand what you are spending on over time.

“Create that budget and stick to it, don’t forget to allow for some treats and fun money. If you are good most of the time, the occasional treat is fine.”

Sort out your debts

Mohindra advises using any spare savings you have to clear debts. “If you’ve got multiple debts, for example a couple of expensive credit cards, overdraft, personal loan, prioritise repaying the highest interest debt first, as it grows fastest. Use all spare cash to clear that and just pay the minimums on everything else. Once it's clear, focus on the next costliest.”

Ellmore agrees, saying focussing on paying off debts now will mean you’re not left with a ‘nasty shock’ later down the line. “Additionally, sticking to regular repayments will help you to protect that all important credit score. Don’t if you can’t afford to, but it will certainly help your finances remain stable,” he adds.

“Next, consider how to reduce the cost of future debt. Interest rates have fallen, which means the cost of debt has also reduced slightly. So, if your credit score is strong, consider moving debt to a 0 per cent credit card, or a personal loan with a cheaper interest rate. This will mean that you’re able to use more money to pay down on the actual debt, rather than just paying off the interest.”

Consider your credit score

While your credit score may be the last thing on your mind, Ellmore says it helps to keep it as high as possible.

He says: "Recessions cause credit markets to tighten, which will make it harder for people with less than adequate credit scores to take on a mortgage, credit card or loan. However, credit scores can be improved by simple actions, such as paying bills on time and keeping your oldest credit cards open.

“Most importantly, if your finances become excruciatingly tight, maintain open communication with your creditors. This will help to keep them on good terms, so they potentially make arrangements to make repayments more manageable, without your credit score suffering.”

Be smart with your money

It’s a no-brainer, but with an impending recession, now is the time to be smart with your money. Compare options, shop at cheaper supermarkets, switch energy and gas providers to get better plans. Do the hard work now so that it will pay off in the months to come.

Ellmore adds: “Always compare your options. So many people remain loyal to certain brands their entire lives, without realising how much they could be saving by shopping around. This goes for almost everything, from your weekly grocery shop to car or home insurance. You could be amazed by how much you save, and your bank balance will certainly thank you.”

https://www.standard.co.uk/lifestyle/financial-advice-furlough-redundant-workers-a4501521.html

The UK economy is officially in recession for the first time since the financial crisis ten years ago.

The economy plunged by 20 per cent between April and June as the pandemic shuttered businesses and kept people locked up at home.

More jobs are likely to be lost and personal finances will take a hit.

Lynn Beattie, Personal Finance Expert at mrsmummypenny.co.uk and author of The Money Guide to Transform Your Life, which will be released on September 1, says: "We are starting to see the impact of covid-19 with many retailers closing branches, including giants like Boots and John Lewis. There will be many more casualties over the remainder of 2020 and well into 2021.”

Audit your finances and live within your means

“Firstly, it is vital to be completely honest with yourself about your financial situation,” John Ellmore, Director of KnowYourMoney.co.uk advises. “Conduct a thorough audit of your finances and gain a comprehensive understanding of all your incomes and outgoings. This will show you exactly where your cash is going and, most importantly, help you identify problematic spending behaviour.”

Ellmore adds that when you’ve figured out how you’re spending money, it’s time to be strict with yourself and don’t make any unnecessary spending. “Living within your means is vital to help avoid any major shocks to your bank balance. Further, any money you can save should be put away in an emergency fund for a rainy day. Hopefully, you won’t need to use it, but it is reassuring to have a financial cushion to fall back on should the worst happen.”

Set up an emergency fund

If you have any money to spare, now would be a good time to think about starting an emergency fund.

“Having an easily accessible emergency fund is essential for surviving a recession. Prepare this as early as possible, particularly if you are still working and you have excess money from savings made during covid-19,” Beattie advises.

“This emergency fund should be able to keep you going for between three to six months, six months is my guidance. Keep it in a separate account that has instant access. This money should remain untouched unless it is a real emergency, for example, money needed to pay the mortgage, or to buy food. Not to be used for holidays or things that you want rather than need.”

Ellmore agrees, and says that if you’re working from home, now is the ideal time to set up an emergency fund. “Take advantage of having regular income and save any extra cash that you can. Be strict with yourself. Refrain from online shopping and stash money away in a savings account. It will definitely ease your worries, knowing that you have money set aside for if the worst happens.

“Firstly, decide the total you want to save. Having an end goal will narrow your focus and give you something concrete to work towards. Regularly assess and re-evaluate your savings strategy. Life is unpredictable and, at times, you won’t be able to save as much as you would like to. So, make sure your savings efforts reflect this and adjust your goals to make them achievable and keep you motivated. Starting an emergency fund might take discipline, but it will definitely help you sleep at night.”

Furloughed workers should be planning for the future

Beattie says that everyone should be looking towards and planning for the future. “What are the chances of the business you work for going into financial difficulties, is there a chance that you might lose your job? Talk to your employer to understand what is happening. The emergency fund is an essential for furloughed workers with a risk of losing their job.”

Ellmore adds that while income will be slightly less while furloughed, you still need to be saving where you can.

He continues: “While the government is putting schemes in place to protect as many jobs as possible, it’s important to give yourself solid financial backing, in case your company is unable to bring you back.

“Make sure you are up to date with debt repayments and having a clear line of communication with your creditor will also help. Keeping your creditor in the loop could mean that, if you find yourself struggling with repayments, your payment schedule could be adjusted, without damaging your credit score.”

Redundant workers need to understand what they are owed

Ellmore says redundant workers need to understand what they are owed - the rule of thumb for statutory redundancy pay depends on the number of years an employee has worked at the company and the amount they have earned. “If in doubt, review your contract. Understanding how much you are due to receive will help you organise your finances in the long term. “

Redundant workers also need to look at ways of making extra money. Beattie says: “Have a big declutter and sell clothes, bags, electronics, old mobile phones. Use sites like Facebook Marketplace, eBay, Gumtree to make some quick cash.

“Is there a side hustle that you can start? What are your skills and how can these be used to make some extra money. Maybe you love walking dogs, maybe you can knit, maybe you are a brilliant photographer, whatever it is, use your skills to make some extra money.”

A budget is imperative

The first step for anyone who has recently been made redundant or is looking to save money, Beattie says, is to do a ‘deep dive’ into your budget.

“Have a clear idea of what essential bills you must pay. Get rid of any unnecessary direct debits and call every company that falls under essential bills to ensure you are on the best deal,” Beattie says. “Use comparison sites to compare deals and switch to a cheaper energy company, broadband, mobile phone, insurance company. When you have worked through your budget you will know how much each month costs you, and how long any redundancy money will last.”

Eesha Mohindra, senior money analyst at MoneySavingExpert.com, says a common mistake when budgeting is to only look at your spending from one to three months.

“Rarely do people look at the whole year – which includes big one-off payments like car insurance, holidays, birthdays and Christmas. So, look at least a years’ worth of statements and write down every category you spend in. There are free budget planner tools available online at moneysavingexpert.com/budgetplanner which makes things very easy for you,” Mohindra adds.

“Within your budget make sure you include how much you want to save each month. Many people just think of saving whatever they have left over each month, rather than factoring it in as a part of their monthly budget.”

Mohindra says the easiest way to factor in saving to your budget is to set up ‘piggybacking’ accounts - several accounts where you can automatically syphon money to save.

“For example, set up individual accounts for household bills, birthdays, holidays, Christmas and emergency fund. That way you have a set amount of money in each account and can’t spend more. If you have only £300 in your holiday fund it means you can’t pay for a £500 holiday.”

Remove any unnecessary payments

Mohindra says one of the easiest places to start saving is by looking at your bank account and removing any pain-free direct debits.

“Are you paying for anything you no longer use like insurance for an old mobile phone, or council tax for a home you no longer live in? If you spot these, call up the company and cancel them. Then look for things you’re currently paying for but could be getting cheaper,” Mohindra adds.

“When was the last time you switched energy tariffs, home insurance, car insurance, broadband, TV package, mobile tariff – don’t let these auto-renew onto expensive out of contract rates. Do a comparison online to see if you can get it cheaper elsewhere or if you want to stick to the same provider then at least consider haggling. For the things you don’t need but do want, ask yourself, is it worth it? Is the gain you get worth the money? Think in annual cost, £8 a month is £100 a year – so if it's a TV subscription you only use a few times or a gym membership you rarely go to, is it worth it? If not, cancel or try and find something cheaper.”

Don’t make impulse purchases

Beattie recommends thinking about a purchase for at least 24 hours before you buy it. “Think about what you are buying, do you really need it, or is it a want. I recently counted my blouses, and have 22, I do not need any more blouses.

“Pop the item into an online basket and come back the next day, you might have changed your mind, and also the company might send you a discount voucher to encourage a purchase.”

Start a spending diary

Beattie also recommends starting a spending diary to keep track of your daily purchases and bills to understand what you buy and why. She adds: “If writing a diary fills you with dread, download an app like Money Dashboard that will consolidate all your accounts to help you to understand what you are spending on over time.

“Create that budget and stick to it, don’t forget to allow for some treats and fun money. If you are good most of the time, the occasional treat is fine.”

Sort out your debts

Mohindra advises using any spare savings you have to clear debts. “If you’ve got multiple debts, for example a couple of expensive credit cards, overdraft, personal loan, prioritise repaying the highest interest debt first, as it grows fastest. Use all spare cash to clear that and just pay the minimums on everything else. Once it's clear, focus on the next costliest.”

Ellmore agrees, saying focussing on paying off debts now will mean you’re not left with a ‘nasty shock’ later down the line. “Additionally, sticking to regular repayments will help you to protect that all important credit score. Don’t if you can’t afford to, but it will certainly help your finances remain stable,” he adds.

“Next, consider how to reduce the cost of future debt. Interest rates have fallen, which means the cost of debt has also reduced slightly. So, if your credit score is strong, consider moving debt to a 0 per cent credit card, or a personal loan with a cheaper interest rate. This will mean that you’re able to use more money to pay down on the actual debt, rather than just paying off the interest.”

Consider your credit score

While your credit score may be the last thing on your mind, Ellmore says it helps to keep it as high as possible.

He says: "Recessions cause credit markets to tighten, which will make it harder for people with less than adequate credit scores to take on a mortgage, credit card or loan. However, credit scores can be improved by simple actions, such as paying bills on time and keeping your oldest credit cards open.

“Most importantly, if your finances become excruciatingly tight, maintain open communication with your creditors. This will help to keep them on good terms, so they potentially make arrangements to make repayments more manageable, without your credit score suffering.”

Be smart with your money

It’s a no-brainer, but with an impending recession, now is the time to be smart with your money. Compare options, shop at cheaper supermarkets, switch energy and gas providers to get better plans. Do the hard work now so that it will pay off in the months to come.

Ellmore adds: “Always compare your options. So many people remain loyal to certain brands their entire lives, without realising how much they could be saving by shopping around. This goes for almost everything, from your weekly grocery shop to car or home insurance. You could be amazed by how much you save, and your bank balance will certainly thank you.”

https://www.standard.co.uk/lifestyle/financial-advice-furlough-redundant-workers-a4501521.html

RSS Feed

RSS Feed