Berkongsi ilmu di program Usahawan Tudung pada 27 Sept 2015 yang lalu. Kehadiran 290 peserta bertempat di Maju Junction, KL.

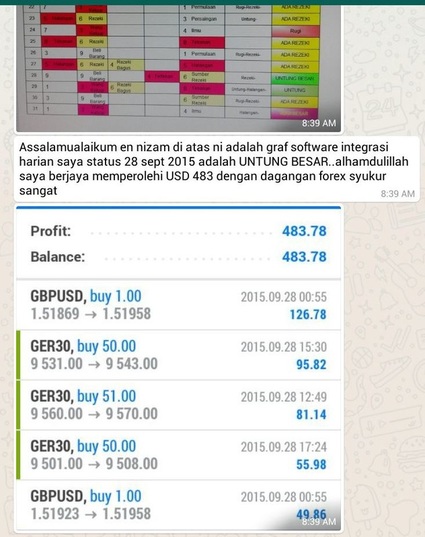

Testimoni penggunaan Software Integrasi - gabungan tarikh lahir dan waktu lahir - satu-satunya dan yang pertama di dunia gubahan team Dato Eddy di sini - digunakan dalam Forex... memang unik, di sini sahaja satu-satunya kaedah tarikh lahir untuk Forex trade... kan senang guna kaedah pernomboran sebagai satu IKHTIAR perancangan...

Bagi tempahan dan tawaran pakej, hubungi En Nizam: 012 769 3807

Bagi tempahan dan tawaran pakej, hubungi En Nizam: 012 769 3807

Program Bulanan... bulan seterusnya Oktober 2015.... terkandung dalamnya bulan Muharram yang mana Awal Muharram dijangka pada 14 Oktober 2015 adalah perubahan dari tahun Hijriyah 1436H (1+4+3+6=5 iaitu tahun yang banyak halangan 5) kepada tahun Hijriyah 1437H (1+4+3+7=6 iaitu 6 adalah REZEKI), jadi kita ikhtiarkan untuk berdoa secara berkumpulan dalam satu grup serta pakej yuran jimat, adalah satu ikhtiar tambahan disamping kita selalu berdoa kepada Nya setiap hari. .. ikhtiar menyiapkan diri kita untuk perubahan... dengan ikthiar energi yang lebih baik untuk tahun akan datang.

Daftar segera sebelum 3 Oktober... boleh daftar dahulu dan yuran boleh dibuat pada lain minggu... untuk elakkan terlepas program.

Daftar segera sebelum 3 Oktober... boleh daftar dahulu dan yuran boleh dibuat pada lain minggu... untuk elakkan terlepas program.

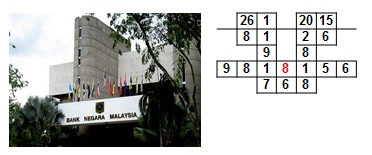

Bank Negara Malaysia berada dalam kitaran tahun 8 untuk tahun 2015 ini... memang tahun 2015 ini begitu sangat mencabar dari aspek kewangan... tahun 2015: negara Malaysia - Vacuum + Blocking + Terminating ditambah pula Bank Negara kitaran 8 dan dunia dalam kitaran 8... Jadi, 2016 menjadi ruang terbaik untuk bangkit semula!

Established on 26 January 1959 as the Bank Negara Malaya, its main purpose is to issue currency, act as banker and adviser to the Government of Malaysia and regulate the country's financial institutions, credit system and monetary policy. Its headquarters is located in Kuala Lumpur, the federal capital of Malaysia.

Established on 26 January 1959 as the Bank Negara Malaya, its main purpose is to issue currency, act as banker and adviser to the Government of Malaysia and regulate the country's financial institutions, credit system and monetary policy. Its headquarters is located in Kuala Lumpur, the federal capital of Malaysia.

KUALA LUMPUR, Sept 28, 2015:

Strengthening the nation’s economic resilience is important during this volatile global period, said Bank Negara Malaysia (BNM) governor Tan Sri Zeti Akhtar Aziz today.

“From time to time, we do see the ringgit recover and there are other development like in China, Middle East and US, all of it are affecting many countries including ours.

“This is likely to persist for some time. Thus we have to gain the resilience to ride out this period,” she said after launching the ‘Financial LATeracy’ exhibition today

She said that Malaysia’s interest rates are describe as accommodative and still supporting economic activity.

“We are still seeing steady growth of credit, meaning it has not hampered borrowing from financial system to support businesses especially SMEs. It is experiencing rapid double digit growth which is good.

“Of course the outlook is challenging, but we still say that growth will be in the region of 4-5%, that is the range.”

She said BNM is not concerned over the possible downgrade to “junk status” by Credit-Default-Swap (CDS) Traders as the downgrade was not by a ratings agency.

Zeti Akhtar Aziz said the “junk status” is only how the market tells their story and a similar thing occurred during the 1998 Asian financial crisis.

“However, a year after the financial crisis, we managed to prove to the world what can we do. We have to be firm so investors will look at how we assess the situation.”

Standard & Poor’s has an A stable rating for Malaysia while Fitch Ratings upgraded its ratings to A stable.

On the ringgit, she said it would not be possible to fix the exchange rate given the highly dynamic environment.

“We do not have any particular level because this is a dynamic environment, therefore, where other currencies are also adjusting, we cannot keep ours at one specific level because it will be misaligned.”

The central bank’s museum and art gallery is hosting the financial literacy exhibition, which is aimed at educating young Malaysian on basic savings and expenditure.

The exhibition featured Datuk Mohammad Nor Khalid’s “Buku Wang Saku” collection since 1999 – caricatures compilation about personal financial management, consumer responsibilities, moral values and cultures in Malaysia.

“The book is part of national savings campaign launched in 1996 – an effort to educate young Malaysians in schools be financial savvy,” said Zeti.

The collection features few themes such as plan your finance, save and invest, track and review spending, be a smart consumer and student’s financial club.

The exhibition runs till next year and public can visit the exhibition for free.

http://www.therakyatpost.com/business/2015/09/28/zeti-malaysia-needs-to-stay-strong-amid-turmoil/

Strengthening the nation’s economic resilience is important during this volatile global period, said Bank Negara Malaysia (BNM) governor Tan Sri Zeti Akhtar Aziz today.

“From time to time, we do see the ringgit recover and there are other development like in China, Middle East and US, all of it are affecting many countries including ours.

“This is likely to persist for some time. Thus we have to gain the resilience to ride out this period,” she said after launching the ‘Financial LATeracy’ exhibition today

She said that Malaysia’s interest rates are describe as accommodative and still supporting economic activity.

“We are still seeing steady growth of credit, meaning it has not hampered borrowing from financial system to support businesses especially SMEs. It is experiencing rapid double digit growth which is good.

“Of course the outlook is challenging, but we still say that growth will be in the region of 4-5%, that is the range.”

She said BNM is not concerned over the possible downgrade to “junk status” by Credit-Default-Swap (CDS) Traders as the downgrade was not by a ratings agency.

Zeti Akhtar Aziz said the “junk status” is only how the market tells their story and a similar thing occurred during the 1998 Asian financial crisis.

“However, a year after the financial crisis, we managed to prove to the world what can we do. We have to be firm so investors will look at how we assess the situation.”

Standard & Poor’s has an A stable rating for Malaysia while Fitch Ratings upgraded its ratings to A stable.

On the ringgit, she said it would not be possible to fix the exchange rate given the highly dynamic environment.

“We do not have any particular level because this is a dynamic environment, therefore, where other currencies are also adjusting, we cannot keep ours at one specific level because it will be misaligned.”

The central bank’s museum and art gallery is hosting the financial literacy exhibition, which is aimed at educating young Malaysian on basic savings and expenditure.

The exhibition featured Datuk Mohammad Nor Khalid’s “Buku Wang Saku” collection since 1999 – caricatures compilation about personal financial management, consumer responsibilities, moral values and cultures in Malaysia.

“The book is part of national savings campaign launched in 1996 – an effort to educate young Malaysians in schools be financial savvy,” said Zeti.

The collection features few themes such as plan your finance, save and invest, track and review spending, be a smart consumer and student’s financial club.

The exhibition runs till next year and public can visit the exhibition for free.

http://www.therakyatpost.com/business/2015/09/28/zeti-malaysia-needs-to-stay-strong-amid-turmoil/

Lihatlah tarikh kemerdekaan negara Malaysia tiada pola 769 iaitu kekayaan.... tetapi pada 2013 lalu berlakunya fenomena pola 769... dan lihatlah nanti pada tahun 2016 ada pola 769! Senyum lah sikit... ada potensi tu... ni tidak, negatif! Maka teruskanlah berpositif dan teruskan berdoa bersatu padu untuk kekayaan negara dan tempias kepada rakyat... tahun 2+0+1+5=8... 8 tekanan... sudah sudahlah ahli2 politik yang kerja asyik bergaduh pasal rezeki tahun ini mana nak berkat... nak negara kaya? Lantik Dato Eddy sebagai PM baru... he he he... tak payah...

Seperkara lagi, pada tahun 2016 nanti, satu lagi pola bagus ada 36... ingat tak pada tahun 2011 lalu harga emas adalah tertinggi dalam sejarah dunia? Sebab tahun 2011 ada pola 36... ini menunjukkan potensi pelaburan adalah baik pada tahun 2016 nanti samalah juga pada tahun 2013 ada pola 36, mudah-mudahan tahun 2016 tak lama lagi nanti setanding kekayaan negara Malaysia.. kebetulan negara Malaysia berada dalam Virtuous Star untuk tahun 2016 nanti, maka jom kita sama-sama bersiap dan ikhtiar untuk suasana kekayaan yang lebih baik untuk 2016 nanti!

Seperkara lagi, pada tahun 2016 nanti, satu lagi pola bagus ada 36... ingat tak pada tahun 2011 lalu harga emas adalah tertinggi dalam sejarah dunia? Sebab tahun 2011 ada pola 36... ini menunjukkan potensi pelaburan adalah baik pada tahun 2016 nanti samalah juga pada tahun 2013 ada pola 36, mudah-mudahan tahun 2016 tak lama lagi nanti setanding kekayaan negara Malaysia.. kebetulan negara Malaysia berada dalam Virtuous Star untuk tahun 2016 nanti, maka jom kita sama-sama bersiap dan ikhtiar untuk suasana kekayaan yang lebih baik untuk 2016 nanti!

KalaPada tahun 2006 lalu, semasa mula-mula Dato Eddy mulakan training tentang pernomboran ada menggunakan contoh tarikh lahir individu ini...

Beliau ada pola 944 tapi pada masa itu potensi itu tidak berlaku kepada individu ini, walaupun memang telah ada tafsiran pola 944 tetapi bila dirujuk kepada individu ini tiada pula sejarah potensi itu berlaku kepadanya... jadi kadang kala kami sekadar gunakan pola potensi lain seperti pola 426 sahaja dalam pengajian kami untuk slide ini. .. rasa segan juga bila present slide ini sebab walaupun individu ini ada pola 944 tapi ianya tidak berlaku kepadanya..

Tetiba pada tahun 2012, menyerlah sudah pola potensi 944 tersebut pada individu itu! Dan sememangnya tepat tafsirannya yang telah tersedia sebelum ini.. yang ditunggu-tunggu berlaku juga akhirnya, syukur.

Oleh itu, untuk menyerlahkan potensi kita kadang kala ianya berlaku pada masa yang agak lewat. Secara teorinya, ketepatan sesuatu kaedah tarikh lahir boleh dibuat apabila individu itu berada pada umur 90 tahun... itu sudah tua! Sebab itu, kaedah kami ini bukan mencari ketepatan... jika pada tahun 2006 orang boleh berkata kaedah kami tak tepat sebab individu ini ada pola 944 tapi tak berlaku pada beliau pun... tapi pada 2012 ianya berlaku... jadinya, yang dicari bukan ketepatan tapi apakah kita menggunakan atau memaksimakan potensi yang ada? Apakah kita mahu menunggu sahaja atau kita ikhtiarkan untuk menyerlahkan atau sekurangnya buat persiapan awal. Kalau nak tunggu ketepatan tarikh lahir maka tunggulah umur anda 90 tahun nanti.

Beliau ada pola 944 tapi pada masa itu potensi itu tidak berlaku kepada individu ini, walaupun memang telah ada tafsiran pola 944 tetapi bila dirujuk kepada individu ini tiada pula sejarah potensi itu berlaku kepadanya... jadi kadang kala kami sekadar gunakan pola potensi lain seperti pola 426 sahaja dalam pengajian kami untuk slide ini. .. rasa segan juga bila present slide ini sebab walaupun individu ini ada pola 944 tapi ianya tidak berlaku kepadanya..

Tetiba pada tahun 2012, menyerlah sudah pola potensi 944 tersebut pada individu itu! Dan sememangnya tepat tafsirannya yang telah tersedia sebelum ini.. yang ditunggu-tunggu berlaku juga akhirnya, syukur.

Oleh itu, untuk menyerlahkan potensi kita kadang kala ianya berlaku pada masa yang agak lewat. Secara teorinya, ketepatan sesuatu kaedah tarikh lahir boleh dibuat apabila individu itu berada pada umur 90 tahun... itu sudah tua! Sebab itu, kaedah kami ini bukan mencari ketepatan... jika pada tahun 2006 orang boleh berkata kaedah kami tak tepat sebab individu ini ada pola 944 tapi tak berlaku pada beliau pun... tapi pada 2012 ianya berlaku... jadinya, yang dicari bukan ketepatan tapi apakah kita menggunakan atau memaksimakan potensi yang ada? Apakah kita mahu menunggu sahaja atau kita ikhtiarkan untuk menyerlahkan atau sekurangnya buat persiapan awal. Kalau nak tunggu ketepatan tarikh lahir maka tunggulah umur anda 90 tahun nanti.

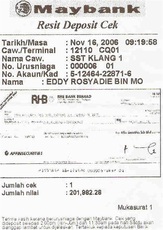

Pada 23 Sept 2015 lalu, sempat daftarkan satu syarikat baru... pada mulanya mahu tubukan kelab/ pertubuhan namun kerana kesuntukan masa maka daftar syarikat dahulu... bertujuan untuk kami bergerak atas satu nama pertubuhan kerana selama ini kami bergerak atas nama syarikat...jadi, bllaman ada event, orang lain guna nama pertubuhan yang kami pulak guna nama syarikat... yang nama ini macam nama pertubuhan... ada masa nanti kami upgrade kepada kelab/ pertubuhan.

Menariknya, no pendaftaran syarikat ini ada pola 38... memang kena dengan tujuan perjuangan... tentang warisan dan metafizik. Singkatan senang nak ingat dan tentunya sudah dikira secara metafizik... No pendaftaran juga berakhir angka 6 dan jumlah kiraan adalah 9! Memang sukar nak dapat nombor siri begini dah didaftar pada tarikh yang ada pola bagus... serta pada 9 Zulhijjah.

Makluman lanjut akan diberitahu nanti tentang aktiviti serta keahlian elit/ biasa.

Menariknya, no pendaftaran syarikat ini ada pola 38... memang kena dengan tujuan perjuangan... tentang warisan dan metafizik. Singkatan senang nak ingat dan tentunya sudah dikira secara metafizik... No pendaftaran juga berakhir angka 6 dan jumlah kiraan adalah 9! Memang sukar nak dapat nombor siri begini dah didaftar pada tarikh yang ada pola bagus... serta pada 9 Zulhijjah.

Makluman lanjut akan diberitahu nanti tentang aktiviti serta keahlian elit/ biasa.

Filem Hollywood yang ada angka 83

Your KPI for personal financial success: Net worth

By: YAP MING HUI

Regular review: Getting a snapshot of your overall financial health regularly will give you a measurement of progress over time, motivating you to reach your financial goals. As such, net worth should be meassured on a regular basis – at the very minimum once a year. — Reuters

HOW does one measure personal financial success?

Some think it is to do with the balance in your bank account while others use their salary as a guideline.

If you’re one to keep up with the Forbes list of top wealthiest, however, you’ll see that the measure of financial success is neither of these two values.

For example, topping the list is none other than Bill Gates with his net worth valued at a whopping US$79.2bil. Locally, sugar, palm oil and real estate tycoon Robert Kuok takes the spot with his net worth commendably valued at US$9.1bil.

In my previous article, I have outlined how investing with net worth in mind is far more efficient as compared to only managing your investments with return on investment (ROI) in mind. ROI is in fact merely a single factor of several which affects the end result – your net worth.

What is net worth and why is it important?

Net worth is essentially a monetary value from which is derived after totalling up your total assets – such as the value in all your bank accounts, shares investments, unit trust investment, the current value of your properties, EPF and so on – and then subtracting the total value of all your outstanding debts such bank loans and taxes.

While net worth is used to gauge your current financial standing, it also serves as an excellent key performance indicator for investing. It quantifies each good and bad financial decision you make thus rendering it one of the best measures of one’s personal wealth. How does this work?

Let’s say you decide to pay more than your monthly mortgage repayment to settle your loan sooner. While you think your wealth has shrunk due to the fact that you have less cash to your name, in the long run you benefit from lower interest charges, therefore increasing your net worth.

For medium to long-term investments, it makes better sense to take a little risk and invest in a few blue-chip stocks than to take the risk adverse path by keeping any surplus cash in a bank account. The quality and payoff of the decision to invest in blue-chip stocks would be reflected in the growth of your net worth some five to eight years from now.

Having a positive net worth also provides you with financial security.

Let’s say, for some reason tomorrow you lose your job. A person with large savings and zero debt (high net worth) would have a more worry-free time in between jobs, as compared to the next person who had a high paying salary but zero in savings and a large amount of debt (negative net worth).

Similarly, a person with a high net worth has the freedom to pursue his or her life’s dreams and ambition even at the expense of drawing a low starting salary. On reflection, a person with negative net worth will not have the luxury and freedom to do as such.

From this scenario, you can already see the different dynamics net worth provides as compared to the mere value of your take-home pay or the amount in your bank account.

How does one increases net worth?

The four drivers of net worth growth are savings, ROI, risks and costs. All these factors work in tandem to influence your net worth as a whole.

To increase your net worth, you’ll need to:

> Increase your savings

Savings is the raw material needed for your net worth growth.

To increase your net worth exponentially, you need to invest. And to invest, you’ll need to have capital. Thus the more you save, the more investment capital you have at your disposal.

The good news is that, among all the drivers for net worth, savings is within your control. The amount you end up saving annually is entirely dependent on your discipline and saving habits.

For example, you would have accumulated RM549,143.57 at the end of 20 years if you have saved RM12,000 annually with an 8% return. For an additional RM48,000 savings per year, i.e. RM60,000, you would have accumulated RM2,745,717.86 instead. The difference that you have accumulated in your savings could go a long way.

In fact, the more you save, the better it is because it makes you less dependent on the other three factors.

> Increase your ROI

The higher the ROI, the faster your net worth will grow.

Naturally, a unit trust giving you a return of 8% annually is preferred over fixed deposits with 4% return. The investment vehicle with the higher return would grow your net worth faster.

Beware of the risk-return trade-off. It is generally understood that the higher the ROI (more than 12%), the higher the risk. You could lose part, if not all, of your investment capital, an outcome which could be a terrible setback to your net worth.

Contrary to what some people might choose to think, ROI is a driver that is not within anyone’s control.

> Decrease your exposure to risk

Risks is also beyond anyone’s control.

While you’re taking active steps to grow your net worth, you’ll need to also take measures to protect yourself against any risks of losing your net worth.

The higher the risks, the higher the potential of your net worth being depleted.

Health-related risks, for example, could deplete the net worth you have spent years to achieve. Without medical insurance, you may have to fork out a lump sum of RM30,000 during a medical emergency. However, for a small monthly fee, you can transfer this risk to an insurance company, thus preserving your net worth value.

Investment risks should be taken into account as well. The Genevva gold scam and the infamous Madoff investment scandal are two perfect examples of investment fraud. Investors had lost millions, many losing 100% of their money because they were blindsided by the upside and failed to consider the risk of capital lost. Those who suffered the loss of their entire life savings also irrecoverably have their net worth affected.

Therefore, always take the time to do your research and due diligence and study your options before you part with your hard earned money.

> Decrease your costs

Most people may not realise this but cost can be a factor which will deplete your net worth. Therefore, one should strive to decrease all unnecessary costs that limits net worth growth.

For example, those who have purchased properties at a higher interest rate should strongly consider revising their interest rate now that the rates have dropped.

A difference between a 20-year housing loan for RM500,000 at an interest rate of 8.6% versus 4.6% is phenomenal – with the former, you’d end up paying RM548,995 in interest, where else with the latter, you’d only fork out RM265,672 in interest payment. A quick revision here could save you money otherwise spent unnecessarily.

Another cost to look out for is the cost of estate administration upon death.

Ironically, many of us spend the majority of our energy and waking hours working in one way or another to grow wealth, but fail to realise the one major cost that could cripple all that we have strived for when we pass on.

Estate administration cost can often reach the leagues of hundreds of thousands of ringgit. Drawing up a comprehensive estate plan for your net worth or inheritance could save you and your loved ones from unnecessary costs incurred (for example, legal fees, administration fees and fees for court proceedings).

Final thoughts

Getting a snapshot of your overall financial health regularly will give you a measurement of progress over time, motivating you to reach your financial goals. As such, net worth should be meassured on a regular basis – at the very minimum once a year.

Growing one’s net worth also involves a multi-dimensional approach.

ROI may play an important role in one’s pursuit of wealth, but it is a means to an end, not an end in itself. To assume such would be just like placing all bets on a singular number in a game of roulette.

Most investors make the rookie mistake of focusing solely on ROI as a means to grow wealth without realising that there are other elements at play.

To increase your overall wealth, it all boils down to the four drivers of net worth growth – savings, ROI, risks and cost, and how effectively you manage them.

Now that you know the four cornerstones of growing net worth, it’s time to put it into practice and steer your way to a financially promising future.

By: YAP MING HUI

Regular review: Getting a snapshot of your overall financial health regularly will give you a measurement of progress over time, motivating you to reach your financial goals. As such, net worth should be meassured on a regular basis – at the very minimum once a year. — Reuters

HOW does one measure personal financial success?

Some think it is to do with the balance in your bank account while others use their salary as a guideline.

If you’re one to keep up with the Forbes list of top wealthiest, however, you’ll see that the measure of financial success is neither of these two values.

For example, topping the list is none other than Bill Gates with his net worth valued at a whopping US$79.2bil. Locally, sugar, palm oil and real estate tycoon Robert Kuok takes the spot with his net worth commendably valued at US$9.1bil.

In my previous article, I have outlined how investing with net worth in mind is far more efficient as compared to only managing your investments with return on investment (ROI) in mind. ROI is in fact merely a single factor of several which affects the end result – your net worth.

What is net worth and why is it important?

Net worth is essentially a monetary value from which is derived after totalling up your total assets – such as the value in all your bank accounts, shares investments, unit trust investment, the current value of your properties, EPF and so on – and then subtracting the total value of all your outstanding debts such bank loans and taxes.

While net worth is used to gauge your current financial standing, it also serves as an excellent key performance indicator for investing. It quantifies each good and bad financial decision you make thus rendering it one of the best measures of one’s personal wealth. How does this work?

Let’s say you decide to pay more than your monthly mortgage repayment to settle your loan sooner. While you think your wealth has shrunk due to the fact that you have less cash to your name, in the long run you benefit from lower interest charges, therefore increasing your net worth.

For medium to long-term investments, it makes better sense to take a little risk and invest in a few blue-chip stocks than to take the risk adverse path by keeping any surplus cash in a bank account. The quality and payoff of the decision to invest in blue-chip stocks would be reflected in the growth of your net worth some five to eight years from now.

Having a positive net worth also provides you with financial security.

Let’s say, for some reason tomorrow you lose your job. A person with large savings and zero debt (high net worth) would have a more worry-free time in between jobs, as compared to the next person who had a high paying salary but zero in savings and a large amount of debt (negative net worth).

Similarly, a person with a high net worth has the freedom to pursue his or her life’s dreams and ambition even at the expense of drawing a low starting salary. On reflection, a person with negative net worth will not have the luxury and freedom to do as such.

From this scenario, you can already see the different dynamics net worth provides as compared to the mere value of your take-home pay or the amount in your bank account.

How does one increases net worth?

The four drivers of net worth growth are savings, ROI, risks and costs. All these factors work in tandem to influence your net worth as a whole.

To increase your net worth, you’ll need to:

> Increase your savings

Savings is the raw material needed for your net worth growth.

To increase your net worth exponentially, you need to invest. And to invest, you’ll need to have capital. Thus the more you save, the more investment capital you have at your disposal.

The good news is that, among all the drivers for net worth, savings is within your control. The amount you end up saving annually is entirely dependent on your discipline and saving habits.

For example, you would have accumulated RM549,143.57 at the end of 20 years if you have saved RM12,000 annually with an 8% return. For an additional RM48,000 savings per year, i.e. RM60,000, you would have accumulated RM2,745,717.86 instead. The difference that you have accumulated in your savings could go a long way.

In fact, the more you save, the better it is because it makes you less dependent on the other three factors.

> Increase your ROI

The higher the ROI, the faster your net worth will grow.

Naturally, a unit trust giving you a return of 8% annually is preferred over fixed deposits with 4% return. The investment vehicle with the higher return would grow your net worth faster.

Beware of the risk-return trade-off. It is generally understood that the higher the ROI (more than 12%), the higher the risk. You could lose part, if not all, of your investment capital, an outcome which could be a terrible setback to your net worth.

Contrary to what some people might choose to think, ROI is a driver that is not within anyone’s control.

> Decrease your exposure to risk

Risks is also beyond anyone’s control.

While you’re taking active steps to grow your net worth, you’ll need to also take measures to protect yourself against any risks of losing your net worth.

The higher the risks, the higher the potential of your net worth being depleted.

Health-related risks, for example, could deplete the net worth you have spent years to achieve. Without medical insurance, you may have to fork out a lump sum of RM30,000 during a medical emergency. However, for a small monthly fee, you can transfer this risk to an insurance company, thus preserving your net worth value.

Investment risks should be taken into account as well. The Genevva gold scam and the infamous Madoff investment scandal are two perfect examples of investment fraud. Investors had lost millions, many losing 100% of their money because they were blindsided by the upside and failed to consider the risk of capital lost. Those who suffered the loss of their entire life savings also irrecoverably have their net worth affected.

Therefore, always take the time to do your research and due diligence and study your options before you part with your hard earned money.

> Decrease your costs

Most people may not realise this but cost can be a factor which will deplete your net worth. Therefore, one should strive to decrease all unnecessary costs that limits net worth growth.

For example, those who have purchased properties at a higher interest rate should strongly consider revising their interest rate now that the rates have dropped.

A difference between a 20-year housing loan for RM500,000 at an interest rate of 8.6% versus 4.6% is phenomenal – with the former, you’d end up paying RM548,995 in interest, where else with the latter, you’d only fork out RM265,672 in interest payment. A quick revision here could save you money otherwise spent unnecessarily.

Another cost to look out for is the cost of estate administration upon death.

Ironically, many of us spend the majority of our energy and waking hours working in one way or another to grow wealth, but fail to realise the one major cost that could cripple all that we have strived for when we pass on.

Estate administration cost can often reach the leagues of hundreds of thousands of ringgit. Drawing up a comprehensive estate plan for your net worth or inheritance could save you and your loved ones from unnecessary costs incurred (for example, legal fees, administration fees and fees for court proceedings).

Final thoughts

Getting a snapshot of your overall financial health regularly will give you a measurement of progress over time, motivating you to reach your financial goals. As such, net worth should be meassured on a regular basis – at the very minimum once a year.

Growing one’s net worth also involves a multi-dimensional approach.

ROI may play an important role in one’s pursuit of wealth, but it is a means to an end, not an end in itself. To assume such would be just like placing all bets on a singular number in a game of roulette.

Most investors make the rookie mistake of focusing solely on ROI as a means to grow wealth without realising that there are other elements at play.

To increase your overall wealth, it all boils down to the four drivers of net worth growth – savings, ROI, risks and cost, and how effectively you manage them.

Now that you know the four cornerstones of growing net worth, it’s time to put it into practice and steer your way to a financially promising future.

Peserta Grup Energi Berdoa Bulan September 2015:

Dato.. Start masuk Sept, our incoming & upcoming job mcm air terjun.. Menderu-deru. Mmg tiapkali berdoa, sy mintak company akan hit beyond target by Q4 2015. Alhamdulillah. Ceo dah janji, nk bg huge increment akhir tahun ni... TQ dato.

Alhamdulillah..Saya juga dapat order dari clients Rose buds tea..dengan jumlah yang tak disangka2..Terima kasih Allah.

------------------

Berada di dalam Grup Bulan adalah ikthiar berdoa secara berjemaah.... kaedah sebegini satu-satunya dan pertama di dunia.... bergabung dan menumpang "energi" dalam satu grup adalah saatu ikhtiar tambahan selain daripada kita berdoa sendirian setiap hari, terutamanya bagi kaum wanita yang kurang kesempatan untuk berdoa berjemaah di masjid kerana tibanya keuzuran atau sukar ke masjid dsbnya, tak pe kami dan grup sama-sama buatkan doa, solat hajat dsbnya.... Nak buat grup berdoa dengan ustaz atau ustazah boleh juga beritahu mereka untuk buat grup sebegini... kan ini ikthiar namanya... bagi grup kami ini khusus untuk doa untuk rezeki, sesekali ada juga doa untuk akademik, kesihatan dsbnya... yang penting kan kata orang bijak pandai, jika nak positif kena berada di kelompok orang yang positif.

Dato.. Start masuk Sept, our incoming & upcoming job mcm air terjun.. Menderu-deru. Mmg tiapkali berdoa, sy mintak company akan hit beyond target by Q4 2015. Alhamdulillah. Ceo dah janji, nk bg huge increment akhir tahun ni... TQ dato.

Alhamdulillah..Saya juga dapat order dari clients Rose buds tea..dengan jumlah yang tak disangka2..Terima kasih Allah.

------------------

Berada di dalam Grup Bulan adalah ikthiar berdoa secara berjemaah.... kaedah sebegini satu-satunya dan pertama di dunia.... bergabung dan menumpang "energi" dalam satu grup adalah saatu ikhtiar tambahan selain daripada kita berdoa sendirian setiap hari, terutamanya bagi kaum wanita yang kurang kesempatan untuk berdoa berjemaah di masjid kerana tibanya keuzuran atau sukar ke masjid dsbnya, tak pe kami dan grup sama-sama buatkan doa, solat hajat dsbnya.... Nak buat grup berdoa dengan ustaz atau ustazah boleh juga beritahu mereka untuk buat grup sebegini... kan ini ikthiar namanya... bagi grup kami ini khusus untuk doa untuk rezeki, sesekali ada juga doa untuk akademik, kesihatan dsbnya... yang penting kan kata orang bijak pandai, jika nak positif kena berada di kelompok orang yang positif.

More than 717 pilgrims die in stampede in worst haj disaster in 25 years

September 24, 2015

MECCA: At least 717 pilgrims were killed on Thursday in a stampede outside the Muslim holy city of Mecca, Saudi authorities said, the worst disaster to strike the annual haj pilgrimage in 25 years. At least 805 others were injured in the crush at Mina, a few kilometers east of Mecca, caused by two large groups of pilgrims arriving together at a crossroads on their way to performing the “stoning the devil” ritual at Jamarat, Saudi civil defense said... In 2006, at least 346 pilgrims died in a stampede at Jamarat.

http://www.freemalaysiatoday.com/category/world/2015/09/24/hajj-stampede-kills-220-people-in-saudi-arabia/

----------------------------

Tahun 2+0+1+5=8.. tekanan... dirasai di pelusuk dunia ini.... kita hanya mampu berdoa kepada Nya... sudah lumrah fitrah alam di dalam perjalanan ketetapan Nya... kitaran tahun 8 adalah untuk menguji ketabahan kita semua... doalah macam mana pun musibah pasti datang kerana ini sudah ketetapan Nya, bukan salah Dia, salah kitalah yang banyak negatif dengan kehidupan ini... yang penting teruskan positif dan berdoa serta tentunya tambah ilmu dan ikhtiar.

September 24, 2015

MECCA: At least 717 pilgrims were killed on Thursday in a stampede outside the Muslim holy city of Mecca, Saudi authorities said, the worst disaster to strike the annual haj pilgrimage in 25 years. At least 805 others were injured in the crush at Mina, a few kilometers east of Mecca, caused by two large groups of pilgrims arriving together at a crossroads on their way to performing the “stoning the devil” ritual at Jamarat, Saudi civil defense said... In 2006, at least 346 pilgrims died in a stampede at Jamarat.

http://www.freemalaysiatoday.com/category/world/2015/09/24/hajj-stampede-kills-220-people-in-saudi-arabia/

----------------------------

Tahun 2+0+1+5=8.. tekanan... dirasai di pelusuk dunia ini.... kita hanya mampu berdoa kepada Nya... sudah lumrah fitrah alam di dalam perjalanan ketetapan Nya... kitaran tahun 8 adalah untuk menguji ketabahan kita semua... doalah macam mana pun musibah pasti datang kerana ini sudah ketetapan Nya, bukan salah Dia, salah kitalah yang banyak negatif dengan kehidupan ini... yang penting teruskan positif dan berdoa serta tentunya tambah ilmu dan ikhtiar.

Filem Hollywood yang menggunakan angka 38 dan 83.

Filem Hollywood yang menggunakan angka 83

Filem Hollywood yang menggunakan angka 38

Untuk berdoa pada hari Wukuf Arafah tahun-tahun akan datang, bolehlah juga dapatkan CD Zikir dan Doa Arafah oleh Ustaz Haji Mohammad Rozie terbitan Inteam.

Bukan selalu ada tarikh yang mana boleh berpanjangan 30 tahun "Rezeki Masuk"... nasiblah dapat lahir 23 September 2015... nak kita ni lahir semula memang tak akan boleh lahir semula, jadi yang boleh ikhtiar lah... seperti berdoa/ solat hajat seumpamanya... bukannya time ni je yang berdoa.. hari-hari pun berdoa cuma pada hari yang istimewa ini kita lebihkan sikit.. kebetulan Hari Wukuf Arafah 9 Zulhijjah... ambil berkat dan auranya.. dengan izin Nya.

Juga boleh buat aktiviti-aktiviti lain seperti membuka akaun bank, mendaftar syarikat dan sebagainya...kan ikhtiar namanya.

Juga boleh buat aktiviti-aktiviti lain seperti membuka akaun bank, mendaftar syarikat dan sebagainya...kan ikhtiar namanya.

Pertandingan Silat di Ulu Tiram, Johor Bahru pada 19-21 September 2015... Pertubuhan Seni Silat Panglima Bugis dapat 4 emas dan 2 perak.

RSS Feed

RSS Feed