How to plan your future on RM2,000 basic salary

LAST week, a friend who read my earlier piece on the importance of inculcating the savings habit called me over to his house.... The young lad started working as a sales executive six months ago and was earning what the lad described as a meagre basic pay of RM1,980.

His gross income, which included commissions, amounted to slightly over RM3,000. Despite the pay, which I considered to be quite good, he said that on some months, he found himself broke as early as a week before payday.

Curious, I asked him if he planned his spending. When he said he did not, I asked if he could give me a rough breakdown of his expenditure and he came up with an estimate of this:

food – 25% of take-home pay;

petrol and car instalment and related expenses – 40%;

entertainment –15%;

contribution to family – 15%, and,

remainder 5% for other incidentals.

- How to save -

I told him he was lucky as he did not have to pay for board and lodging since he was staying with his parents. On top of that, he also ate his dinner at home and during weekends.

His annual income had also put him out of the taxable bracket. While I agreed with him that it was not easy to save even with his income, especially if one is living in Kuala Lumpur city, I said I had known of some of those his age who were earning a third less than he did and got by quite comfortably.

I said that if he could trim 5% off his entertainment expenses and add it to his 5% of what he had allocated for incidentals, he could actually save 10% of his take home pay each month. I noted that he had also yet to purchase a life or health insurance, so I advised him to look into it if he could fit it into his budget.

He asked me what good it would do to save 10% of his meagre pay when in years to come purchasing power of the savings would have dropped as cost of living escalated. I said if he didn’t start saving, he would have nothing by that time, despite rising costs of living.

But with a healthy cash reserve, I said he could do plenty. What was more important was to inculcate a savings habit. If he had cash reserves, he could also put it in a fixed deposit account to earn interest or have it invested in a higher-return investment like trust funds.

If he wanted to buy a property one day, I said he could also put a higher downpayment and borrow less from the bank.

Indeed, saving 10% of one’s income was not much. But I told him that sum accumulated over three years would total an amount equivalent to three times his current pay, and should he for any reason lose his job, he would be able to sustain himself until he got a job again.

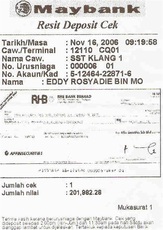

To help him understand better, I did a chart of his projected savings in 10 years, based on a regular monthly deposit of 10% of his pay. (You can see how much RM300 diligently deposited monthly over 10 years with a 3.5% compound interest will add up to in the chart given.)

I told my friend’s son that he was only 23 years old. By the time he was 33, he would have a healthy growing cash reserve of RM43,709 which he could use for other more profitable expenses like starting s family, putting a deposit on a house or even for education to improve his paper qualifications if he chose to.

And if he did not touch the savings, in another 15 years when he was 48, he would have a total of RM140,928, as shown in my calculation using with an online tool at

http://www.investor.gov/tools/calculators/compound-interest-calculator#.VMG1uf7Lez5

As you can see, the final amount was derived at with the assumption that there was no increase in the value of deposits or a rise in interest rate (from 3.5%).

In a real-life scenario, chances are that his pay will rise with time and the regular 10% deposit will also be increased accordingly.

If he strictly kept to the discipline of savings, his cash reserves would be a very healthy one by the time he reached retirement age because his own savings, plus the mandatory contribution to the Employees Provident Fund, would have grown by leaps and bounds.

I suggested to the chap that he make a simple financial forecast chart like the one I did and review it each time he got a pay rise. I told him to also make copies of his chart and place them at places where he would see them throughout the day.

The charts with his financial goal would ensure that he stayed on track as he strove towards financial freedom.

Read more:

http://www.therakyatpost.com/columnists/2015/01/28/plan-future-rm2000-salary/#ixzz3QBmrAsNX

LAST week, a friend who read my earlier piece on the importance of inculcating the savings habit called me over to his house.... The young lad started working as a sales executive six months ago and was earning what the lad described as a meagre basic pay of RM1,980.

His gross income, which included commissions, amounted to slightly over RM3,000. Despite the pay, which I considered to be quite good, he said that on some months, he found himself broke as early as a week before payday.

Curious, I asked him if he planned his spending. When he said he did not, I asked if he could give me a rough breakdown of his expenditure and he came up with an estimate of this:

food – 25% of take-home pay;

petrol and car instalment and related expenses – 40%;

entertainment –15%;

contribution to family – 15%, and,

remainder 5% for other incidentals.

- How to save -

I told him he was lucky as he did not have to pay for board and lodging since he was staying with his parents. On top of that, he also ate his dinner at home and during weekends.

His annual income had also put him out of the taxable bracket. While I agreed with him that it was not easy to save even with his income, especially if one is living in Kuala Lumpur city, I said I had known of some of those his age who were earning a third less than he did and got by quite comfortably.

I said that if he could trim 5% off his entertainment expenses and add it to his 5% of what he had allocated for incidentals, he could actually save 10% of his take home pay each month. I noted that he had also yet to purchase a life or health insurance, so I advised him to look into it if he could fit it into his budget.

He asked me what good it would do to save 10% of his meagre pay when in years to come purchasing power of the savings would have dropped as cost of living escalated. I said if he didn’t start saving, he would have nothing by that time, despite rising costs of living.

But with a healthy cash reserve, I said he could do plenty. What was more important was to inculcate a savings habit. If he had cash reserves, he could also put it in a fixed deposit account to earn interest or have it invested in a higher-return investment like trust funds.

If he wanted to buy a property one day, I said he could also put a higher downpayment and borrow less from the bank.

Indeed, saving 10% of one’s income was not much. But I told him that sum accumulated over three years would total an amount equivalent to three times his current pay, and should he for any reason lose his job, he would be able to sustain himself until he got a job again.

To help him understand better, I did a chart of his projected savings in 10 years, based on a regular monthly deposit of 10% of his pay. (You can see how much RM300 diligently deposited monthly over 10 years with a 3.5% compound interest will add up to in the chart given.)

I told my friend’s son that he was only 23 years old. By the time he was 33, he would have a healthy growing cash reserve of RM43,709 which he could use for other more profitable expenses like starting s family, putting a deposit on a house or even for education to improve his paper qualifications if he chose to.

And if he did not touch the savings, in another 15 years when he was 48, he would have a total of RM140,928, as shown in my calculation using with an online tool at

http://www.investor.gov/tools/calculators/compound-interest-calculator#.VMG1uf7Lez5

As you can see, the final amount was derived at with the assumption that there was no increase in the value of deposits or a rise in interest rate (from 3.5%).

In a real-life scenario, chances are that his pay will rise with time and the regular 10% deposit will also be increased accordingly.

If he strictly kept to the discipline of savings, his cash reserves would be a very healthy one by the time he reached retirement age because his own savings, plus the mandatory contribution to the Employees Provident Fund, would have grown by leaps and bounds.

I suggested to the chap that he make a simple financial forecast chart like the one I did and review it each time he got a pay rise. I told him to also make copies of his chart and place them at places where he would see them throughout the day.

The charts with his financial goal would ensure that he stayed on track as he strove towards financial freedom.

Read more:

http://www.therakyatpost.com/columnists/2015/01/28/plan-future-rm2000-salary/#ixzz3QBmrAsNX

Foto: jika anda masih ingat tentang latihan pola 38 sebelum ini... cikgu Ady conteng satu perkataan di rak buku dan minta anda gunakan energi dalaman "melihat" apa yang diconteng tu... logiknya sape yang tahu apa yang cikgu Ady tulis... tapi yang tak logiknya bagaimana ada beberapa individu yang dapat berikan jawapan dengan tepat! Tak dapat dijelaskan dengan sains... inilah metafizik energi 38!

My sis bgtau suaminya dah dpt kerja ok… then lampu kat hall umah dia selama ni bertahun x menyala… dah menyala… since tukar arah…hidup ini keajaiban… so touching doa sya utk prmudahkan segala galanya… finally jumpa cikgu

Sesi berdoa di Tasik Shah Alam bersama En Eddie beberapa thn lepas alhamdulillah, byk perubahan berlaku pd sy ttg simpanan wang dlm acc (sbb ada bawa buku acc bank masatu). Tq En Eddie.

Alhamdulillah lepas waktu doa 24/02/2014 saya dapat sewa rumah baru, network saya bertambah agak ramai pada tarikh yang sama dan hari ini jumpa pengerusi koperasi untuk masuk produk, jadual 3 bulan dah padat, hubungan saya suami isteri bertambah tenang, syukur pada Allah kerana jalan di hadapan ibarat highway... terima kasih Cikgu eddy

Alhamdulillah… elok je saya hbs berdoa.. kawan tel nak dtg rumah n beli produk jumlah 3K.

Sesi berdoa di Tasik Shah Alam bersama En Eddie beberapa thn lepas alhamdulillah, byk perubahan berlaku pd sy ttg simpanan wang dlm acc (sbb ada bawa buku acc bank masatu). Tq En Eddie.

Alhamdulillah lepas waktu doa 24/02/2014 saya dapat sewa rumah baru, network saya bertambah agak ramai pada tarikh yang sama dan hari ini jumpa pengerusi koperasi untuk masuk produk, jadual 3 bulan dah padat, hubungan saya suami isteri bertambah tenang, syukur pada Allah kerana jalan di hadapan ibarat highway... terima kasih Cikgu eddy

Alhamdulillah… elok je saya hbs berdoa.. kawan tel nak dtg rumah n beli produk jumlah 3K.

....so surprised sedang tengok blog Cikgu yg tahun2 dulu... pola 38&83.. duit siri no yg ada 38.. dalam hati.. bilalah nk dapat no ni???... tak sampai 1 minit housemate bg balance duit sewa.. hujungnya no 38..

Sesungguhnya pada kejadian langit dan bumi dan pada pertukaran malam dan siang, ada tanda-tanda (kekuasaan, kebijaksanaan dan keluasan rahmat Allah) bagi orang-orang yang berakal (190) (Iaitu) orang-orang yang menyebut dan mengingati Allah semasa mereka berdiri dan duduk dan semasa mereka berbaring mengiring dan mereka pula memikirkan tentang kejadian langit dan bumi (sambil berkata): Wahai Tuhan kami! Tidaklah Engkau menjadikan benda-benda ini dengan sia-sia, Maha Suci Engkau, maka peliharalah kami dari azab Neraka (191) [Surah Ali Imran: 190-191]

Dia lah Yang menjadikan matahari bersinar-sinar (terang-benderang) dan bulan bercahaya, dan Dia lah Yang menentukan perjalanan tiap-tiap satu itu (berpindah-randah) pada tempat-tempat peredarannya masing-masing) supaya kamu dapat mengetahui bilangan tahun dan kiraan masa. Allah tidak menjadikan semuanya itu melainkan Dengan adanya faedah dan gunanya Yang sebenar.Allah menjelaskan ayat-ayatNya (tanda-tanda kebesarannya) satu persatu bagi kaum Yang mahu mengetahui (hikmat sesuatu Yang dijadikanNya).” ( Surah Yunus: 5 )

“Daripada Abdillah ibn Abbas r.hm berkata, Nabi SAW telah bersabda : “Sesungguhnya matahari dan bulan merupakan 2 ayat dari ayat-ayat Allah. Tidak berlaku gerhana ( matahari atau bulan ) kerana kematian atau kelahiran seseorang. Maka jika engkau melihatnya segeralah mengingati Allah.”

Dia lah Yang menjadikan matahari bersinar-sinar (terang-benderang) dan bulan bercahaya, dan Dia lah Yang menentukan perjalanan tiap-tiap satu itu (berpindah-randah) pada tempat-tempat peredarannya masing-masing) supaya kamu dapat mengetahui bilangan tahun dan kiraan masa. Allah tidak menjadikan semuanya itu melainkan Dengan adanya faedah dan gunanya Yang sebenar.Allah menjelaskan ayat-ayatNya (tanda-tanda kebesarannya) satu persatu bagi kaum Yang mahu mengetahui (hikmat sesuatu Yang dijadikanNya).” ( Surah Yunus: 5 )

“Daripada Abdillah ibn Abbas r.hm berkata, Nabi SAW telah bersabda : “Sesungguhnya matahari dan bulan merupakan 2 ayat dari ayat-ayat Allah. Tidak berlaku gerhana ( matahari atau bulan ) kerana kematian atau kelahiran seseorang. Maka jika engkau melihatnya segeralah mengingati Allah.”

Cikgu Ady - Syracuse 1995.

Lulusan Syracuse University, New York, USA dalam bidang Biology. Kemudian mengambil pengajian praktikal dalam bidang Clinical Medical di Onondaga Medical School di Syracuse juga.

Pekerjaan terakhir sebagai Pengurus QA di sebuah organisasi pengeluar terbesar di dunia... kini full-time dalam bidang pernomboran tetapi masih buat part-time dalam bidang QA (audit dan latihan).

Isteri cikgu Ady juga penuntut Syracuse University dalam bidang Electrical Engineering. Kemudian menyambung pengajian EMBA di UiTM, Shah Alam. Kini sebagai Pengurus HR di sebuah organisasi.

Tahukah anda: Individu terkaya Saudi, Putera Al-Waleed b Talal, pemilik Kingdom Holding, merupakan penuntut di Syracuse University, New York.

Lulusan Syracuse University, New York, USA dalam bidang Biology. Kemudian mengambil pengajian praktikal dalam bidang Clinical Medical di Onondaga Medical School di Syracuse juga.

Pekerjaan terakhir sebagai Pengurus QA di sebuah organisasi pengeluar terbesar di dunia... kini full-time dalam bidang pernomboran tetapi masih buat part-time dalam bidang QA (audit dan latihan).

Isteri cikgu Ady juga penuntut Syracuse University dalam bidang Electrical Engineering. Kemudian menyambung pengajian EMBA di UiTM, Shah Alam. Kini sebagai Pengurus HR di sebuah organisasi.

Tahukah anda: Individu terkaya Saudi, Putera Al-Waleed b Talal, pemilik Kingdom Holding, merupakan penuntut di Syracuse University, New York.

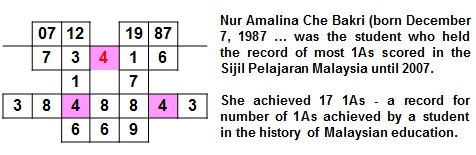

Salah satu bentuk profiling bagi membantu anak / pelajar adalah menggunakan kaedah pernomboran daripada tarikh lahir sebagai satu cara mengenalpasti masalah dan tentunya menjelaskan fenomena dan mencari/ membuat strategi pembetulan.

Angka 4 bagi kaum Cina adalah "mati" sampaikan tingkat 4 diganti 3A ... tetapi daripada kajian cikgu Ady mendapati angka 4 adalah tentang "ilmu"... apakah anak anda/ pelajar memiliki angka 4 yang banyak dan apakah angka 4 yang banyak menjamin kejayaan akademik? Bagaimana pula jika seseorang itu tiada angka 4 langsung? Penceramah untuk 31 Jan 2015 nanti tiada angka 4 dalam petak tarikh lahir tapi boleh pula cemerlang dalam akademik... bagaimana caranya tu? Jom, 31 Jan.

Apakah maksud no 4 di lokasi nombor bakat? Apakah maksud angka 4 di kiri petak dan di kanan petak.. bagaimana menggunakannya? Bagaimana jika tiada apakah strategi pembetulan?

Apakah maksud no 4 di lokasi nombor bakat? Apakah maksud angka 4 di kiri petak dan di kanan petak.. bagaimana menggunakannya? Bagaimana jika tiada apakah strategi pembetulan?

Program di Sabah pada 10 Jan 2015 lalu, sempat bergambar di depan Kinabalu Park....

Jumpa lagi pada 28 Feb 2015 nanti ye!

(1) Kelas Asas

(2) Program Taklimat Kerja di Australia

Hubungi En Nizam 012 769 3807 untuk maklumat lanjut.

Jumpa lagi pada 28 Feb 2015 nanti ye!

(1) Kelas Asas

(2) Program Taklimat Kerja di Australia

Hubungi En Nizam 012 769 3807 untuk maklumat lanjut.

Assalammualaikum cikgu..saja nk share masa rawatan aritu rasa sejuk tenang lapang ja mmg best cuma anak2 komen mak dia garang skrg...

Antara maklumbalas daripada ikhtiar energi seperti transfer/ rawtaan energi dan pemakaian minyak wangi pyrite adalah cepat marah. Ianya berlaku apabila energi yang terkumpul dalam badan menjadikan kita extra cergas dan extra sensitif, maka kawallah emosi dan gunakan energi tambahan itu untuk berkerja keras dan aktif... seumpama minum Red Bull, Livita atau 100 Plus sebagai ikhtiar tambah energi.

Antara maklumbalas daripada ikhtiar energi seperti transfer/ rawtaan energi dan pemakaian minyak wangi pyrite adalah cepat marah. Ianya berlaku apabila energi yang terkumpul dalam badan menjadikan kita extra cergas dan extra sensitif, maka kawallah emosi dan gunakan energi tambahan itu untuk berkerja keras dan aktif... seumpama minum Red Bull, Livita atau 100 Plus sebagai ikhtiar tambah energi.

RSS Feed

RSS Feed